Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

August 29, 2022

Coming off the worst first half in over fifty years, both the stock and bond market seemed primed for at least a rebound. Rising interest rates, high inflation and worries about a possible recession had combined to bring the ‘pandemic-induced’ bull market in stocks to a screeching halt in the first half. However, one of the biggest signs that maybe the selling in the first half had gone too far was the Bank of America June investor survey, wherein they described investor sentiment as ‘apocalyptic’, with global growth and profit expectations at an all-time low, recession expectations at their highest since the pandemic-fueled slowdown in May 2020, investor allocation to stocks at lowest level since October 2008, and cash at the highest since 2001. That extreme level of bearish positioning in stocks set the stage for a counter-trend rally. That spark was then lit by hopes that the slight cooling in rampant inflation would get the Federal Reserve to slow the pace of its rate hikes in time to avert an economic contraction, as it did after a similar market meltdown in the 4th quarter of 2018. Stocks bounced sharply, lead by the technology and other ‘high growth’ sectors that had taken the worst drubbings in the first half sell-off. The S&P500 bounced more than 16% off the June lows, while the ‘tech heavy Nasdaq Index advanced over 20%, which put U.S. stocks on course for one of their best summers on record. Canadian stocks participated in the bounce as well, with the S&P/TSX Index gaining over 10% off the lows. But the gains here were less than those ‘south of the border’ as Canadian stocks were held back by some aggressive selling in the ‘formerly red hot’ energy sector.

We believe it is premature for investors to begin celebrating the end of monetary tightening from the central banks. While we expect inflation will pull back into the 4-5% range from the weakness in commodities, cooling in housing market and the ‘fire sale’ of bloated retail inventories, the further reduction down to the 2% target range that central bankers have announced will take both time and a lessening of economic growth. The much anticipated ‘pivot’ in Fed policy back to easing that ignited the summer rally in stocks is more ‘hope’ than ‘reality.’ The next big event for the Fed that investors are still gearing up for is the late September meeting. The consensus seems split between a 50 basis point (bps) increase or another 75 bps like we saw in both June and July. The only logical reason we see for keeping the increase to only 50 bps would be that the increases in rates seen so far this year have been one of the most aggressive on record, and another 75 bps coming this soon might end up being ‘overkill’ on financial conditions. Probably a better strategy would be for the Fed to watch to see how the data on inflation and growth unfolds over the next few months before making another big move. However, no matter which path they take, rates are going to stay higher for a longer period of time than investors currently expect. Stock market investors will have to deal with either higher interest rates (which compress stock valuations) or an economic slowdown from these rate increases (which reduces or reverses earnings growth) or maybe both! While we don’t advocate ‘market timing’ as an investment strategy, it’s hard not to see the headwinds that investors will continue to face in the near term and we have adjusted all of our managed portfolios accordingly, reducing equity exposure slightly, going to more defensive, recession resistant sectors and adding to bond exposure as a hedge against economic weakness.

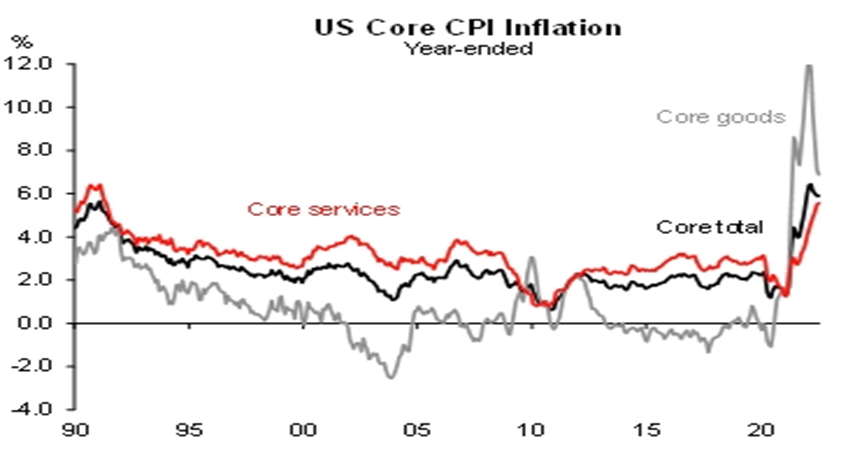

Investors celebrated the July inflation data, which showed some respite from peak levels on a drop in some key commodities and price reductions on retail inventories. While inflation might have come down slightly, it’s still at 8.5%, which is stubbornly high, particularly with a very tight labor market. As shown below, ‘goods inflation’ has pulled back more substantially in the past two months, but cooling off the core ‘goods’ inflation was easier than bringing down core ‘services’ inflation, which is a bigger reflection of the tightness in labour markets and the embedded expectations of rising wages and costs. There is absolutely no reason for the Fed to slow down their tightening cycle yet.

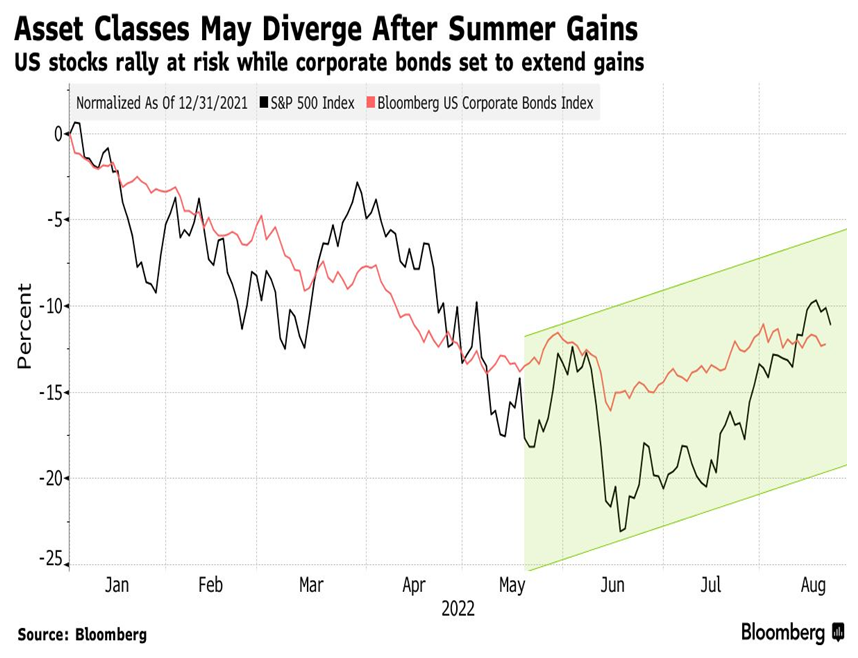

Bonds did also come along for the ride in the summer rally, recovering a bit after they suffered their worst six-month periods on record. But now investors are finally starting to see slight ‘cracks’ in the inflation data while economic weakness in Europe and China has put global growth worries back into focus. While it’s been a summer of love for both stocks and bonds, we believe equities are set to fade while bonds could strengthen as central banks continue ‘tightening’ of financial conditions and recession fears take hold.

Having moved in tandem for most of 2022 thus far, we believe that stock and bond markets are now set to diverge, with bonds looking better as the dash to safety in an economic downturn gains speed. Stocks have done well as the second-quarter earnings did restore some faith in the health of corporate America and Europe as companies largely proved demand was robust enough for them to pass on higher costs. But many companies see slowing demand in the second half of the year, combined with continued supply chain issues, rising input prices and higher labour costs. The bottom line is that we still believe earnings estimates, as a whole, remain too high and will have to be reduced over the next few quarters. Those earnings estimate reductions will be another headwind for stocks, where consensus estimates are still pointing to 8% earnings growth in 2023.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.