Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

August 29, 2022

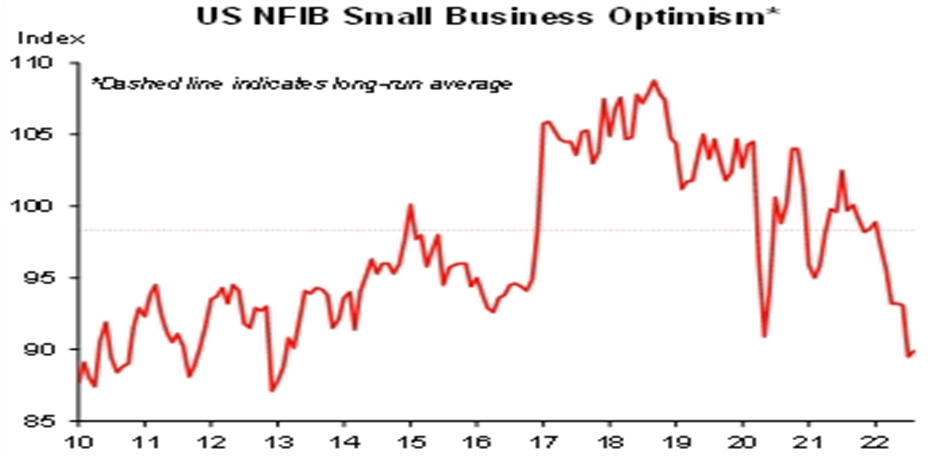

The economic indicators are still somewhat ambiguous about a slowdown. Some broad economic indicators, such as the U.S. labour market, have held up strongly and Canadian employers were looking to fill an all-time high of 1,037,900 jobs in June, according to Statistics Canada. That ongoing strength in labour markets is not indicative of any upcoming economic weakness. But those tend to be ‘lagging indicators’ of economic conditions. Leading economic data has clearly turned lower. Retailers are having to shed excess inventories at discounted levels as retail sales have slowed down sharply this summer. Technology companies are seeing longer sales cycles for many of their services, typical of a slowing economy. Consumer confidence measures have absolutely collapsed due to the expiration of many government support programs, the increase in interest rates and the sharp drop in financial markets in the first half. But one of the more telling lead indicators has been the absolute collapse in the NFIB Small Business Optimism index (shown below), which has now actually dropped below those levels seen in the early days of the pandemic.

In Canada we also have one more factor working against any shorter-term upside in stocks; a withdrawal of foreign funds from our market! Foreign investors pulled the most money out of Canadian stocks in 15 years amid fears that recession would hit an equity market that’s highly sensitive to changes in the economic cycles. They reduced their exposure by C$12.6 billion in June, the third consecutive month of outflows and the most since 2007 as inflation soared at its fastest pace in four decades. The Canadian market, due to its smaller size, has always been more susceptible to shifts in foreign investor funds and this sets up additional risks. Domestic investors also continued to pull their money out of Canadian mutual funds. The latest data from the Investment Funds Institute of Canada (IFIC) showed there was a net redemption of $4.5 billion from equity and bond mutual funds in July, following a net redemption of $10.4 billion in June. The biggest outflows came in bank stocks, which make up about a fifth of the S&PTSX Composite Index and have dropped about 15% from their February highs. Bank earnings reports last week showed year-over-year declines in core earnings as weaker capital markets and increased loan loss provisions offset the positive impact of higher interest rates. While we don’t see major downside in Canadian banks currently and they do carry attractive dividend yields, we have said for months that the tailwinds of the last few years are turning into headwinds for the sector and earnings growth will be negligible. Hard to advocate a large position in banks with that outlook. We have minimal holdings in Canadian financials in client accounts.

Will the 1% buyback tax make a difference for stocks? In the recently approved IRA (Inflation Reduction Act) Bill in the U.S., corporations will now pay a 1% tax on stock buybacks. According to data from S&P Global, U.S. buybacks set a record in the twelve months ended March 2022, hitting a whopping $985 billion. By sector, Tech ($275 billion), Financials ($210 billion), and Communication Services ($140 billion) accounted for the bulk of the total, whereas sectors like Real Estate ($2.1 billion) and Utilities ($2.4 billion) barely explained any of the repurchases. Therefore, to the extent that the new 1% tax reduces the appeal of engaging in buybacks, some sectors will see virtually no impact whereas others (such as Tech, Financials, and Communication Services) are going to be comparatively more affected.

This tax would impact no company more than Apple Inc. which has been the epi-centre of stock buybacks and the resultant ‘magic’ for the stock from what many refer to as ‘financial engineering.’ Their numbers over the past decade on buybacks are staggering. They spent over $500 billion on stock buybacks, more than the market cap of over 490 companies in the S&P500 Index. In a rising stock market that was rewarding tech companies with earnings growth, these results boosted prices sharply, even if the real growth was less than impressive. From 2015-2020 Apple basically had a flat operating income (i.e. no growth). However, during that same period they bought back almost 20% of their outstanding shares, leading to ‘earnings per share’ growth of over 25%. That made investors believe that Apple was more of a growth story than it had been, and they rewarded it with a higher stock multiple. The combination of higher earnings per share from the buybacks alone and a higher earnings multiple on the stock lead to a doubling of the share price over that same five-year period, despite the fact that operating income had basically not grown. Nice work if you can get it! Maybe taxing these buybacks isn’t the worst idea we’ve heard and may ‘level the playing field’ a bit in the stock market.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.