Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

March 31, 2022

Stocks had been experiencing one of their worst starts to the year in the past decade on worries about central banks raising interest rates to quash multi-decade highs in inflation, putting a significant dent in the hyper-elevated valuations of growth stocks. Seemingly making this sell-off even worse, Russia invaded Ukraine on Feb. 24th, thereby potentially putting NATO forces in direct conflict with a major superpower for the first time since the Second World War! While stocks sold off sharply on that first morning of the invasion, they quickly rebounded over the following two days. They weakened again two weeks later in advance of the Fed’s March meeting, but turned higher again during Jerome Powell’s post meeting press conference and have not looked back since. From those mid-March lows to the end of the month, the S&P500 rose over 10% while the technology-heavy Nasdaq Index gained over 15%! The fact that stocks have rebounded so sharply in the last few weeks perplexed most investors, ourselves included. Particularly since the rally started around the same time that the U.S. Federal Reserve announced they would begin raising interest rates for the first time since 2018. We would chalk up the stock market reaction to a ‘sell on rumour, buy on news’ response. Some credit should be given to the Fed, which has done an extremely good job of telegraphing all of their moves in advance, and many investors had been worried that the increase might be a half-point rather than the announced quarter-point increase. More importantly, investors had already been very bearishly positioned going into both the invasion of the Ukraine and the Fed rate increase. One poll, conducted between March 4 and 10, covered 341 investors with an aggregate US$1-trillion in assets under management and showed a remarkable degree of negativity. The proportion of those money managers expecting the economy to strengthen in the months ahead was at the lowest level seen since the financial crisis of 2008. The same poll also showed an expected equity bear market in 2022 and allocations to global equities at their lowest levels since May 2020. Cash levels among those same investors rose to nearly 6% while allocations to commodities soared to a record 33%. Investors were clearly positioned for a pullback and put this cash back to work in stocks after the meeting when the Fed confirmed the rate move.

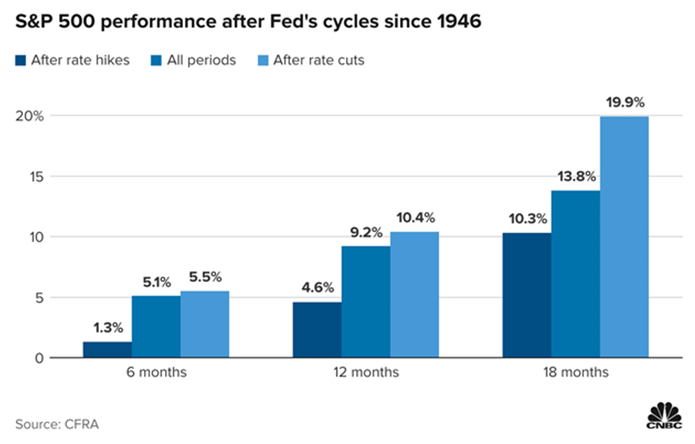

Another explanation for the bullish action of the market is that investors have paid attention to the chart below, which shows that the performance of the stock market had been positive, on average, in the 6, 12 and 18-month periods following the start of prior rate-tightening cycles. However, investors should take those results with a ‘grain of salt’ since those returns are lower than similar period returns, both after ‘rate easing’ cycles and average market returns. One of the many old adages for stock market investors is the ‘Three Steps and a Stumble’ rule, which alleges that the larger risk for stock investors comes after the third interest rate increase in any cycle. Bottom line is that when the Fed embarks on a series of rate hikes in a row, the stock market typically manages to go higher during that time, but the gains are harder to come by than normal times, or when the central bank is lowering rates.

The recovery in stocks over the past month does though seem to fly in the face of the increased risk. We do note that the gains have been heavily concentrated in the biggest growth names such as Apple, Nvidia and Tesla. In some ways those stocks have almost become defensive plays, much in the same way that bonds, gold and utility stocks have been in the past. The massive cash positions and commanding market shares seem to mitigate the risk in many investors’ views despite their rich valuations.

For us, the main conclusion from the recent strength in stocks, though, is that investors are ‘buying into’ the narrative that the Fed will indeed be able to engineer a ‘soft landing’ of the economy. Slowing down an overheated economy with inflationary pressures without driving it into a recession in the process is a difficult goal and usually fails, as it did when Paul Volcker tried to do something similar in the early 1980s and ended up pushing the economy into ‘back-to-back’ (or ‘double dip’) recessions. Jerome Powell, in a recent speech, cited three historical examples — the tightening cycles of 1964, 1984 and 1993 — as evidence that the Fed can achieve a “soft landing,” slowing growth and curbing inflation without precipitating a recession. The recent surge of buying of stocks amidst a backdrop of inflation, growth worries, higher rates and even war all suggest that investors are, for now, buying into the belief that the Fed can indeed pull it off!

Inflation has become the biggest worry for the stock market and the prime reason why central banks such as the U.S. Fed have become so much more hawkish in their interest rate outlook. Inflation acts as a tax on all consumers and is a bigger risk to the economy than the risk that raising interest rates leads to a sell-off in stocks, which impacts a smaller part of the population, indeed the wealthier portion that has the excess savings to invest in stocks. In terms of addressing the ‘cause’ rather than the ‘symptoms’ of this inflation, the primary source has been the sharp increase in the cost of goods, due to the shortages from supply chain problems, pandemic-related closures, and an overall underinvestment in new capacity, combined with an increase in demand from the massive stimulus spending and low interest rates. This can be seen most clearly in the action of the commodity sector. The chart below shows the 144% surge in commodity prices over the past year is the highest annual rise in over 100 years! This surge has contributed to the highest core inflation rate in the past four decades.

Adding to the list of risks to the stock market, the global economy is bracing for greater disruption as China scrambles to contain its worst Covid outbreak since the pandemic began. If China fails to contain Omicron’s spread it would derail that economy’s promising start to the year, weakening a key pillar of global growth. As manufacturer to the world, any disruptions to exports resulting in shortages could also worsen inflation internationally, just as central banks begin hiking interest rates. Over the past two years, China has had relative success in minimizing such disruptions by bringing virus cases quickly under control. Some of last week’s weakness in oil, base metals and steel were driven by worries about Chinese demand slowing down.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.