Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

March 31, 2022

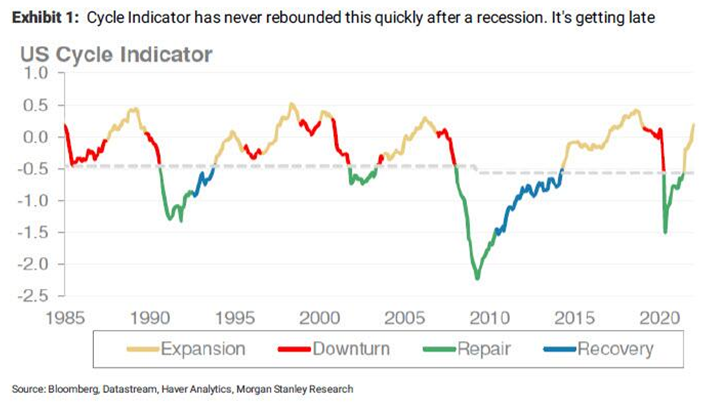

Getting a good read on the path of the current economic recovery seems a key to getting earnings forecasts right, and thus the stock market as well. The US Cycle Indicator, shown below, aggregates key data to help signal where we are in the economic cycle and where headwinds/tailwinds exist for different asset classes. The latest rebound following the Covid pandemic has been the fastest on record, increasing the worry that this cycle has been truncated and could end quickly. The recent tightening of monetary conditions by central banks also increases worries about the duration of this cycle. Growth outlooks have been slashed by many strategists, recession has moved to nearly the base case in Europe and the past history of extreme oil price spikes would suggest a similar future could await the U.S.

When it comes to the impact on stocks, if the fears about a slowdown come to fruition, then the ‘growth to value’ switch which has worked out so well over the past six months could come to an early end. The last time that economically-sensitive (short duration) stocks outperformed growth for an extended period was the 2001-2008 period, which was driven by strong, synchronous global growth, lead by exceptionally strong growth in China as it increased commodity imports to support its industrial capacity expansion. We are not moving into a repeat of that period. Debt levels are already at records as are fiscal deficits, which was needed to get economies through the pandemic.

Taking all of these points into account, we need to update our investment strategy. The technology sector takes up most of the discussion about where to be positioned. The bearish case, which lead us to reduce our overweight position in the group, is that the rise in interest rates presents the greatest risk to these ‘high multiple’ stocks. Boosting interest rates increases the cost of borrowing and negatively impacts growth-oriented stock valuations. Tech stocks are seen as sensitive to rising rates because increased debt costs make their future cash flows less valuable. This occurred again in the 2022 correction as growth stocks, innovative tech in particular, suffered the most severe sell-off, helping to briefly drive the Nasdaq Composite into bear market territory (down more than 20% from its record high) before the recent rally brought it back onside.

Another factor against continued outperformance by technology stocks is that the earnings growth advantage in this sector that has existed since the pandemic lows has ended. Other sectors such as energy, industrials, basic materials and consumer cyclicals are all set to see earnings growth that will match or exceed what we have seen from the technology sector during the ‘pandemic period.’ We understand the bullish scenario, that the war in Ukraine will have no impact on anyone’s plan to buy an iPhone, move their corporate data onto a Microsoft server or continue to stream data from Amazon Prime or Netflix and that the earnings profile remains strong. Also, the valuation of the tech stocks are nowhere near the extremes seen during the 1990s technology ‘bubble.’ In our portfolios we had reduced tech holdings but retain an overweight with a focus on semi-conductors, cloud service providers and cyber security. We also like the space and defence sectors, where we see increased government and commercial spending as satellite constellations continue to be launched and data interpolation providers see a substantial growth in demand for their services.

We reduced our overweight in the telecom sector as BCE, Rogers and Telus have all moved closer to our target prices with their recent rallies. Quebecor, on the other hand, has lagged and looks like it could play ‘catch up’ since it doesn’t look like it will get into a bidding war for Shaw’s wireless assets, which Rogers is expected to be forced to sell in order to get approval for its purchase of Shaw Communications. Pipeline stocks such as TC Energy, Enbridge and Pembina have also reached our short-term target prices, but we retain partial positions due to their attractive dividend yields. Gold stocks are still cheap but have failed to generate expected returns despite what should have been great tailwinds for the sector (i.e. low interest rates, heightened geo-political risks and high inflation). We reduced positions in the sector, selling Torex Gold and Kirkland Lake and retaining only Agnico Eagle and B2Gold. On the buy side, we increased our exposure to some extremely beaten-up consumer cyclical names, particularly autos, such as Magna, GM and Martinrea, as well as Air Canada and BRP, which just reported an earnings beat and increased 2022 guidance despite continued headwinds from supply chain issues. Finally, we increased portfolio weights in the industrial and transportation sectors on recent weakness, adding to holdings in CP Rail, Fedex, CargoJet and MDA on the view that energy prices have seen their peaks for this cycle and that the economy will only slow down but not see a recession this year or next.

Banks, however, have seen their best earnings gains for this cycle and we reduced exposure. While banks initially lagged the 2020 recovery, they made up that ground in the past year as they took in excess loan loss provisions, increased dividends and buybacks, basked in strong capital market activities and saw their loan books improve on a steeper yield curve. Those trends have almost all played out now. The banks in Canada have traded up to the high end of their historical valuation ranges. The dividend yields are also less attractive than the telecom, utility or pipeline sectors. Recent acquisitions by BMO and TD show how they have to go outside Canada in larger ways to sustain growth, which also increases the risks associated with the integration of such large purchases. We don’t think there is large downside in the sector and they have always been a good safety play in softer markets, but don’t see nearly as much upside as we potentially do in the consumer discretionary, technology or industrial sectors, all of which have been under more intense selling pressure this year.

While stock markets have faced increased risks, bonds have not provided their traditional ‘safe haven’ status during that period of weakness. Global bond markets have suffered unprecedented losses since peaking last year, as central banks including the Federal Reserve look to tighten policy to combat surging inflation. The Bloomberg Global Aggregate Index, a benchmark for government and corporate debt total returns, has fallen 11% from a high in January 2021. That’s the biggest decline from a peak in data stretching back to 1990, surpassing a 10.8% drawdown during the financial crisis in 2008. It equates to a drop in the index market value of about $2.6 trillion, worse than the approximate $2 trillion loss in 2008. While U.S. 10-year bond yields have surged to 2.5%, that still represents a negative real rate of return with core inflation running higher than a 5% annual rate. The traditional 60/40 stock/bond portfolio might be another ‘thing of the past’ as all investors search for alternatives and add asset classes such as private equity, private debt, crypto currencies, preferred share and other income alternatives. However, with the recent bond sell-off, we would argue that the TINA (there is no alternative) trade is now dead. Bonds are starting to look like good hedges for balanced portfolios again and could provide a better buffer during any economic slowdowns. When everyone seems ready to throw in the towel on a particular asset class, it is probably time to take a closer look at it. “Plus ça change, plus c’est la même chose!” We are slowly starting to add back some bonds into the asset mix of portfolios.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.