Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

July 15, 2019

Outlook

As alluded to earlier, the global economy is entering the 2H /19 with a downshift in momentum. The narrowing in U.S. and global growth rates leads us to believe the U.S. dollar has likely peaked and will depreciate relative to other currencies. The new dovish stance of the US Fed plays into this dynamic.

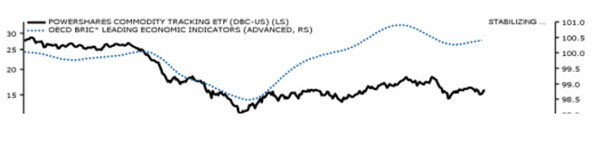

With global growth slowing, the decline in leading economic indicators worldwide has been concentrated in the developing countries. If we look at emerging markets (which account for 78% of GDP growth and the largest component of demand for base metals), we see strength. The BRIC LEI is positively diverging and reaccelerating due to reflating monetary policies in China and India (see below).

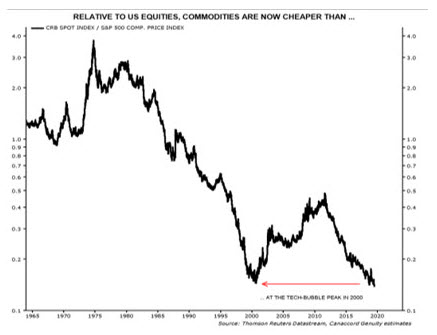

Furthermore, when we look at commodity stock valuations; we see they are at all time lows relative to the stock market. This gives us confidence that we are setting up for a very strong cyclical/commodity rally in the second half of the year.

Currently we are overweight both precious and base metal stocks. This quarter, gold stocks broke out with gold trading through $1400/oz. The last time gold traded near this level; gold stock prices were 30% higher. With global central banks increasing monetary stimulus, and the technical indicators strengthening, we believe that gold has significant room to rally and have positioned the portfolio accordingly.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.