Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

July 15, 2019

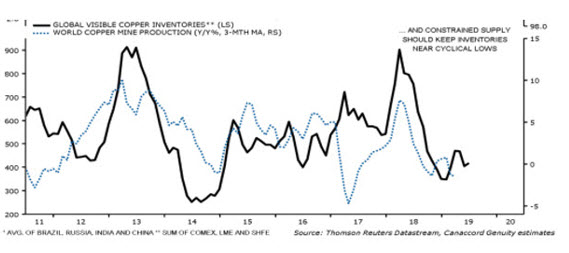

Lastly, if we look at copper supply, we expect global inventories to remain low as depressed copper prices have led to reduced mining capital expenditures. This will keep future copper supply muted.

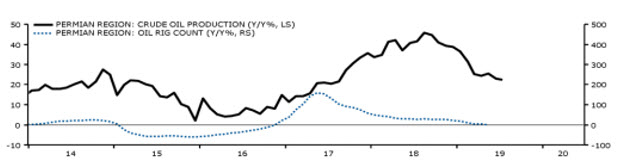

Energy is a different story because of the constant supply from the Permian Basin and the issues in Canada pipelines egress. While the portfolio was underweight the energy sector last quarter, we have added to energy stocks due to valuation and improving supply conditions. Falling rig counts, lower production from the shale basins and the extension of the 1.2 mill barrel cut from OPEC and Russia have us more constructive on the energy sector going into the second half of 2019.

With US growth slowing (but still positive), we are also concerned with stocks focused on the US consumer and industrial sectors. We are underweight both sectors in the portfolio. We also continue to look for special growth situations, that can do well despite the economic back drop.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.