Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

March 31, 2021

Staying on the economy theme, one of the largest current risks to the economic outlook in our view stem from variants of the Covid-19 virus. So far, vaccines have proven to be effective at reducing the severity of cases even from new strains, though this could change if a more aggressive mutation emerges that’s resistant to current shots. As well, as in Europe, Canada’s slower vaccine rollout puts it at greater risk of a third wave than the U.S. Italy has returned to lockdown to suppress a recent rise in cases. But despite the increased lockdowns and slow rollout of vaccines, the March economic data on ‘the other side of the pond’ has held up remarkably well. Eurozone preliminary PMIs for March blew out expectations, with all major countries we track experiencing sequential improvement. The Eurozone Manufacturing PMI hit an all-time high last month, with Germany reaching a record level and France accelerating at the fastest pace since late 2000. Manufacturing activity also expanded briskly in the UK, with the PMI coming in ahead of expectations. Manufacturing companies benefited from a pickup in demand and saw average input prices surge at the sharpest pace in over a decade. The Eurozone Services PMI also rose in March and recorded a seven-month high. The services industry however remains in contraction land and recent lockdowns suggest that this two-speed economy could persist for some time.

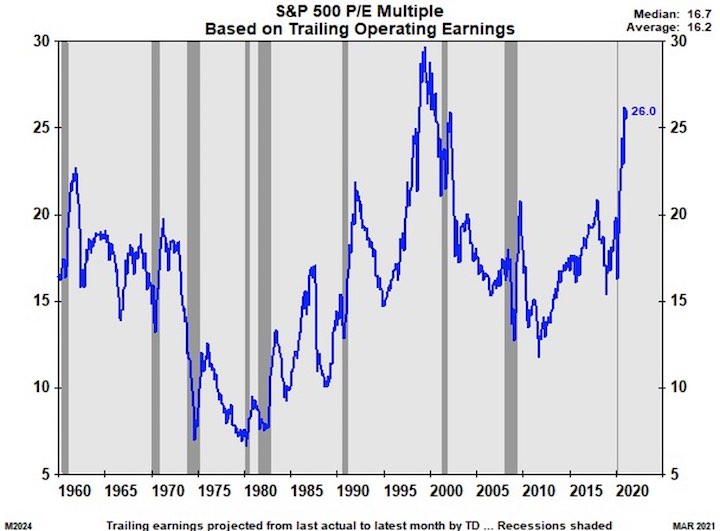

Back on the risks we see in stocks, the top concern has to be the simple overall level of valuation. The earnings multiple on the S&P500 is so clearly running at a very high historical level (see chart below), driven in large part over the past few years by the record low interest rates. To be bullish on the stock outlook, we have to be convinced that the re-opening will take place along with a level of ‘pent-up demand’ for services that will need to be met. The bottom line is that the key to sustaining higher stock prices over the next few years will have to be through earnings growth, which can sustain higher stocks even if stock market multiples begin to contract.

While technology has ‘ruled the roost’ for much of the past decade, we have been talking hee about the more recent sectoral shift from ‘growth to value’ as interest rates have headed higher and expectations for economic growth have gotten revised higher. The ratio of technology to energy stocks spiked significantly last year, similar to what happened in the late 1990s during the last ‘tech bubble.’ While we don’t argue that technology has a far better growth profile over time, it looks like an adjustment is still taking place. While the ‘long energy’ and ‘short tech’ trade has worked well over for the last few months, many short-term traders wonder if it may have almost run its course for now. The chart below,though, shows just how far out of whack the ratio of tech to energy has gotten over the past five years and how long it took for that trade to find a bottom after the 1990s tech bubble. Our strategy is still to hold long positions in the energy sector but continue to look for longer-term opportunities on weakness in the ‘renewable energy’ as well as technology stocks. No need to hurry though!

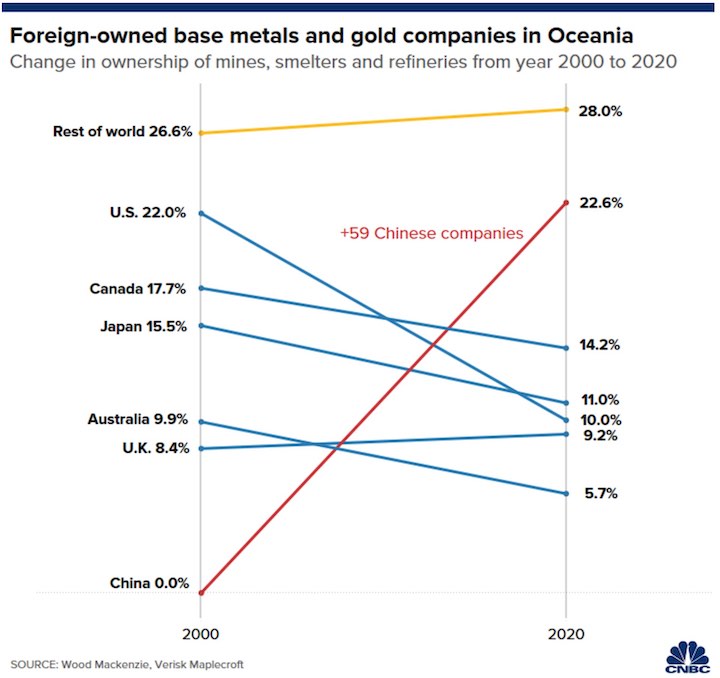

Another good reason to stick with the resource trade, at least in the short term, is on the premise that corporate activity with pick up in this sector. Will China’s resource buying binge expand into Canada in a bigger way? China is a large consumer of major commodities including crude oil and iron ore. But the country has always relied heavily on imports to meet its domestic demand for those commodities. One way the country is now diversifying its import sources is by buying stakes in overseas companies. Doing that increases the proportion of Chinese-owned resources in the country’s total imports. China is seeking to strengthen its control over global supply chains via overseas investments and partnerships with international majors. Beijing has been supporting Chinese SOEs [state-owned enterprises] to ‘go global’ and establish control of resource bases overseas since the late 1990s. as shown below, China’s ownership of the resource industry in Oceania has risen from zero to over 22% in the past 20 years to become by far the largest single country player in those industries.

I took some time last week to chat with former BNN anchor Catherine Murray on her new YouTube channel for an in depth look at the current outlook for the stock market and some investment ‘picks and pans.’ Here’s the interview: https://youtu.be/vtivTcmO43Y

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.