Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

March 31, 2021

Stocks in March acted much like they did in February, starting off the month very strongly then stalling out a bit mid-month and seeing some weakness towards month end. Maybe this advance is just getting a little ‘tired’ after passing the one-year anniversary of the March 23rd, 2020, lows, but the investor ebullience of the post-election period has clearly faded. The biggest difference between the past few months and most of 2020 has been the change in leadership to the more economically sensitive stock groups and away from the technology, growth and ‘stay at home’ names that were the big winners last year. A long overdue recovery in the financials, basic materials and energy sectors has been somewhat offset by weakness in the Apple’s, Amazon’s, Zoom’s and Tesla’s of the world and leading to more muted overall gains for the S&P500, while the Dow Industrials moves to record highs and the technology-heavy Nasdaq stocks fade. Most of this trade-off is due to a sharp difference in the world of bonds and interest rates versus last year. While slow growth, massive central bank easing and zero interest rates made ‘long duration’ growth stocks the ‘go to’ choice last year, the sudden rise in interest rates and stronger economic has turned banks, energy and industrials such as Boeing, Deere, 3M and Caterpillar into the early winners thus far in 2021.

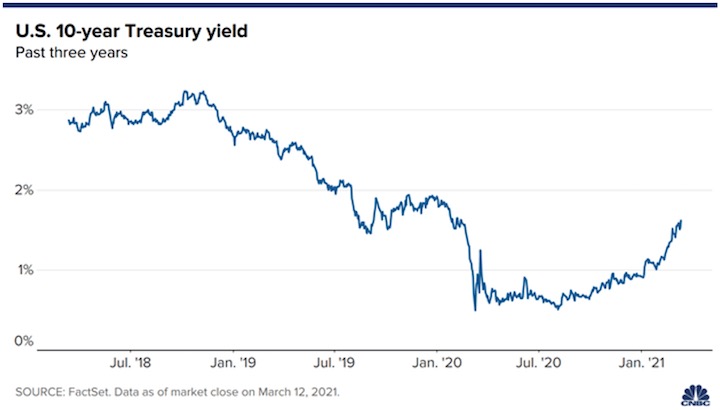

Going forward, the second year of any recovery does tend to run into a few more ‘roadblocks’ along the way. Assuming the sharp, fast economic recession and bear market last year set the stage for a new economic and stock market cycle, then we can expect a more challenging year for stocks in 2021, not unlike what we saw in similar recoveries in 1984, 1991, 2002 and 2010. The first year of bull markets associated with economic recovery tend to show large gains with minimal corrections as investors are usually underweight stocks coming out of a bear market/recession and tend to be buyers on any dip, thereby keeping the uptrend intact. Larger corrections tend to be seen in the second year of new bull markets when there are fewer underweight investors looking to increase their exposure. Earnings multiples also expand in the first year of a new bull market, but invariably decline following that, partly because accelerating earnings growth has been anticipated by investor. Rising bond yields also become more of a headwind for stocks as a recovery takes hold. Clearly, we have seen some evidence of that thus far this year as ten-year bond yields have basically ‘tripled off their lows’ (though to keep that in perspective, it is only about a 1.2% increase). While these rates remain far below the levels prior to the pandemic (which themselves were viewed as ‘record lows’ at the time), the recent direction is clear. Moreover, borrowings have increased sharply under these low rates and that alone is cause for concern in financial markets as risk-taking behaviour has risen, as shown by ‘margin debt’ among prime brokers and banks moving up to record levels.

We’ve all heard the phrase ‘a rising tiding lifts all ships’ (except maybe in the Suez Canal last week!). The aphorism is associated with the idea that an improved economy will benefit all participants, and that economic policy, particularly government economic policy, should therefore focus on broad economic efforts. But the antithesis of that is what is exposed when ‘the tide goes out.’ That risk that is becoming apparent in financial markets, which had been levitated by the tide of zero interest rates and financed by egregious levels of debt. As some of these most highly levered stocks have dropped sharply in recent months, the casualties of ‘the tide going out’ are starting to show up. Hedge fund manager Archegos, which managed US$10-billion of client money, collapsed last week after getting hit with margin calls. Investment banks Nomura and Credit Suisse, which had reportedly lent money to the hedge fund, now face billions of dollars in losses as they unwound those positions in names such as Discovery, ViacomCBS and some Chinese internet stocks such as Baidu, Tencent and Alibaba. It is the second major disruption fuelled by margin trading in as many months. In February, retail trading platform Robinhood was forced to raise US$3.4-billion in emergency capital after its clients borrowed excessive amounts of money to trade volatile stocks such as GameStop. Both scenarios have been resolved without a broader fallout, but a record US$814-billion has been borrowed to fund trading positions. All that debt makes financial markets highly susceptible to sharp corrections. Much like Archegos, many hedge funds try to ‘juice their returns’ by borrowing money to invest. When the bets pay off, the gains can be prolific. When they don’t, they can backfire quickly, forcing panic selling. If the fund is big enough, the sales can send the broader market spiralling, much like the sell-off caused back in 1998 when hedge fund Long Term Capital Management imploded on levered bets in the bond market.

Taking all of these factors into account, we have shifted the asset mix in our managed portfolios slightly. We are now 55% stocks (still slightly overweight in our typical range of 35-65%), 30% bonds/preferred shares (at the bottom of our range) and 15% cash (near the top of our range). At the sector level, we lowered portfolio risk by reducing growth sectors, which tend to be somewhat more volatile, while adding to core cyclical value sectors, particularly those with above-average dividend yields such as the pipeline and telecom stocks. We have also increased cyclical exposure, with higher sector weights in basic materials, industrials and financials.

Canadian investors were treated to the announcement of two ‘mega’ ($25+ billion) mergers in March as Rogers Communications acted on a long-expected move to consolidate their position in wireless and cable markets by offering to buy Shaw Communications in an all-cash deal at $40.50 per share. Then Canadian Pacific Rail tried its third ‘kick at the can’ to buy a U.S. railroad, with its cash and stock offer to buy Kansas City Southern Railway. The logic of this deal is very clear, particularly with the new USMC trade agreement now in place. If successful, this would give CP access to a sprawling Midwestern rail system that connects farms in Kansas and Missouri to ports along the southern ports and would also let CP reach deep into Mexico, which made up almost half of Kansas City Southern’s revenue last year. There’s an upside for the environment here, too, which CP highlighted. Rail is four times more fuel efficient than trucking, a competitive advantage as shippers take carbon emissions into account.

Both of these deals should provide a very important signal to investors. Large companies like this would not be committing this level of capital if they didn’t believe that economic conditions would be supportive of their expansion. We also like the fact that both deals are being done primarily for cash. If a company’s management thought it’s stock was over-valued to any degree then it would be more likely to use the highly-valued currency of its own stock to make those deals. The fact that both CP and Rogers are putting cash on the table rather than their own stock suggests they believe their stocks are under-valued, the high level of borrowing is manageable and that the deals will ultimately add to both their earnings and growth.

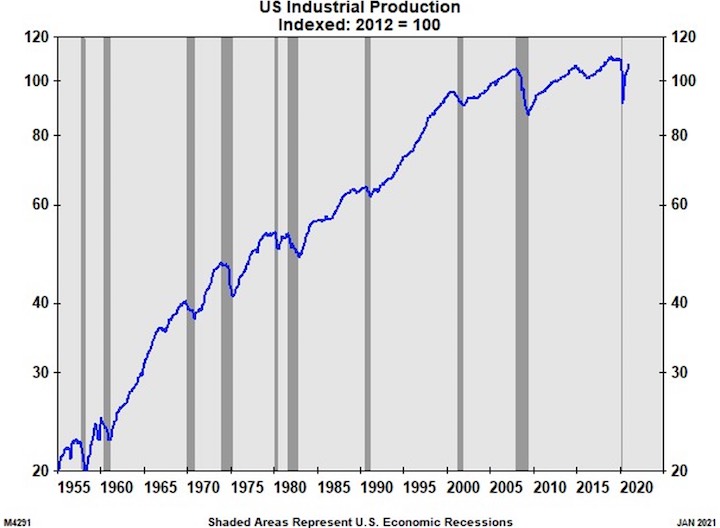

On the economic front, despite the expected boost from re-opening, the 70-year flattening of the growth curve for US industrial production is unlikely to be altered by any changes in policy. While a cyclical recovery is once again in place, aided by new infrastructure spending and some rationalization of global trade, we see this as only a ‘transitional’ period of stronger growth. Longer term, the impacts of globalization and trade specialization will continue to move manufacturing to lower cost regions and for North American growth to reflect the maturity of these economies. Some ‘nationalistic’ tendencies have picked up more support in economies all over the world, but we don’t think they will be enough to derail the longer-term growth trends in the industrialized economies. Intel Corp’s announcement this month that they were going to be spending $20 billion to build two new semi-conductor manufacturing facilities (FABs) in Arizona is clearly a departure from this trend and it will be interesting to see how this new strategy plays out. Stock market investors are not yet convinced on the success of this strategy if the recent volatility in Intel stock is any indication.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.