Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

June 30, 2020

Given all that we have discussed above in terms of increases in speculation, unsustainable valuations and excessive recovery optimism, it is difficult for us paint a very bullish outlook for stocks right now. But we also have to remain aware of the fact that interest rates will be staying extremely low for probably a very long time, meaning that bonds and cash will not be providing the types of returns that many investors are looking for, which could continue to drive money into stocks. In that type of scenario, stock and sector selection will be much more important than just index exposure for generating superior returns going forward. We continue to find the best opportunities in what we call the ‘middle ground’; companies that may not have superior growth but which have moderate valuations and generate positive cash flow such that they can continue to pay and grow their dividends. In Canada, we continue to have overweight positions in the pipeline, telecom and utilities sectors, where we are seeing dividend yields of 6% or more and valuations of less than ten times operating cash flows, which compares very well to the more expensive high growth sectors without the risk associated with more cyclical sectors. We have also added to some of our Canadian bank holdings in the past month as the major six banks all kept their dividends intact and maintained sufficient capital ratios despite three-fold increases in loan-loss provisions and a dour outlook for growth. We also continue to add preferred shares to the portfolio, particularly where there are strong credit ratings and little risk of lower rate resets. Our overall holdings in the sector right now are generating dividend yields of close to 8% with no missed payments or cuts. These are the types of low risk, low volatility and high yield opportunities that we would prefer to invest in now rather than ‘rolling the dice’ on an expectation of a recovery to anywhere close to where we were economically before the pandemic began.

In our ‘macroeconomic-based’ hedge fund we also face the same conundrum as our other investment strategies. We have to balance the market risks associated with high valuations and overly-optimistic outlooks for economic recovery against the knowledge that central banks will continue to stand behind financial markets with extremely low interest rates for an extended period of time, thus providing a continued tailwind for stocks. While March was mostly to the downside, April and May reversed the bulk of those losses. Rather than taking large ‘macro’ positions on either the ‘long’ or the ‘short’ side of the stock market, we have stuck closer to a ‘market neutral’ strategy over the past few months by having core long positions in gold while maintaining and adding (on weakness) to long positions in defensive and growth areas such as utilities, pipelines, telecom and technology. At the same time we have mostly offsetting short positions in cyclical indices such as the Wilshire2000 and S&P500 as well as some extended names in the ‘recovery’ sectors such as energy and consumer cyclicals. The strategy has worked fairly well as the Fund is up about 8% so far in 2020.

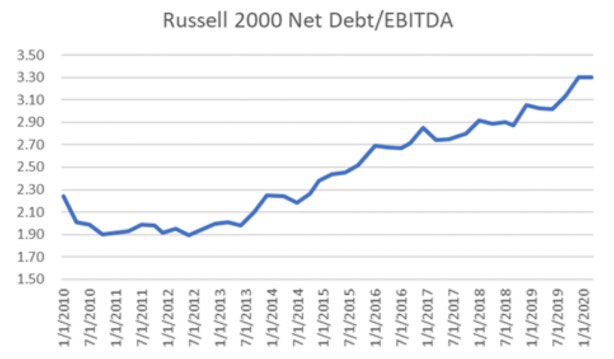

One more bearish wrinkle; the corporate debt bubble! The consumer housing and debt binge in the early 2000s sowed the seeds that ultimately lead to the banking and financial crisis in 2008. The reason we saw such an anemic recovery post-2009 was because consumers effectively went into a spending hiatus which was necessary to repair the balance sheets which had been getting worse for over 20 years. We may now be seeing a similar scenario developing in the business sector, which has become dramatically more indebted since 2008. But companies haven’t been borrowing to increase real economic activity like households did in the 2000s. Instead, businesses have mostly just been switching the composition of their balance sheets from equity to debt. In the process that has made their balance sheets much more vulnerable to the kind of shock we’re seeing today, which helps explain why the Federal Reserve has been so much more aggressive with its corporate credit program compared with 2008. The chart below shows how the debt/EBITDA ratio of the broadly-based Russell2000 companies has gone up by about 50% over the past decade.

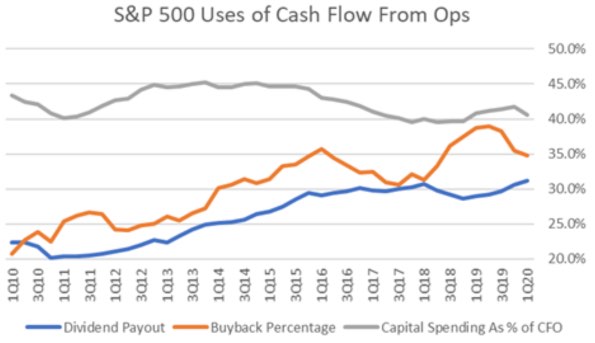

The debt boom of the 2000s boosted household consumption far above household income growth, but it wasn’t sustainable. It ended with a wave of foreclosures and a sustained period of consumption growth below the long-term trend. Since most of those loans were held by the major banks, they were the ones that took the biggest hit. This time around most of the debt has been raised by corporations directly as bonds. While banks are large holders of this paper as well, we expect that the corporate bond sector could be most at risk as we start to see defaults rise. In terms of the destination of all the cash raised in these debt offerings, it has not been into productive means such as capital expenditures (capex) or even acquisitions. In fact, capex has been basically flat for the past ten years. But we have seen more ‘shareholder friendly’ uses such as buybacks and dividends increase meaningfully.

No matter how you shake it out though, there are going to be far less funds available for stock buybacks over the next few years and that had been the single largest source of demand for stocks over the past decade!

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.