Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

June 30, 2020

The veracity of the rise in the stock market off the March 23rd lows has confounded many stock fundamentalists as the contrast of the ongoing economic deterioration versus the record-high valuation level of stocks seems to defy logic. The quick, aggressive action of the Federal Reserve to provide massive amounts of liquidity into financial markets effectively put a floor under stocks as investors believed the U.S. central bank had ‘their backs covered.’ Larger funds re-allocated money from bonds into stocks and passive investments once again surged. The subsequent recovery was lead by the technology sector and other ‘stay at home’ stocks. But the real surprise in our view has been how the recovery has continued and now migrated over to the most speculative names and sectors, as money has shifted into the laggards such as airlines, cruise companies and the ‘resurrection of the value trade’. Moreover, the most shorted stocks have surged over 80% since the lows; outperforming the overall index by a factor of two times!

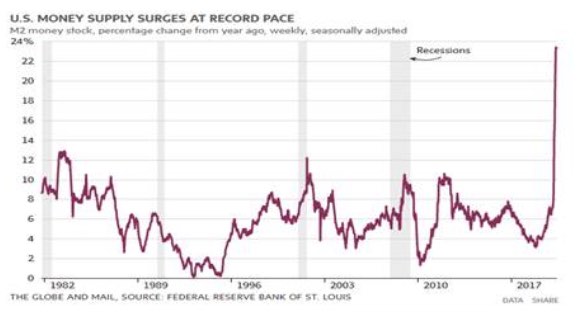

Reading the daily news about the continued increase in Covid19 cases across the globe and the massive negative impact on the global economy in 2020 (and probably for years to come) it seems paradoxical that stocks have surged back close to their all-time highs in the U.S. But the chart below gives a very good visual on the expansion of money recently, lead by the massive liquidity provided by the Federal Reserve. Since very little of those funds are finding their way into real spending by businesses or individuals, it ends up going into financial assets, with stocks right at the top of that list. From this perspective it seems less confusing as to why stocks have rallied so sharply since the March lows!

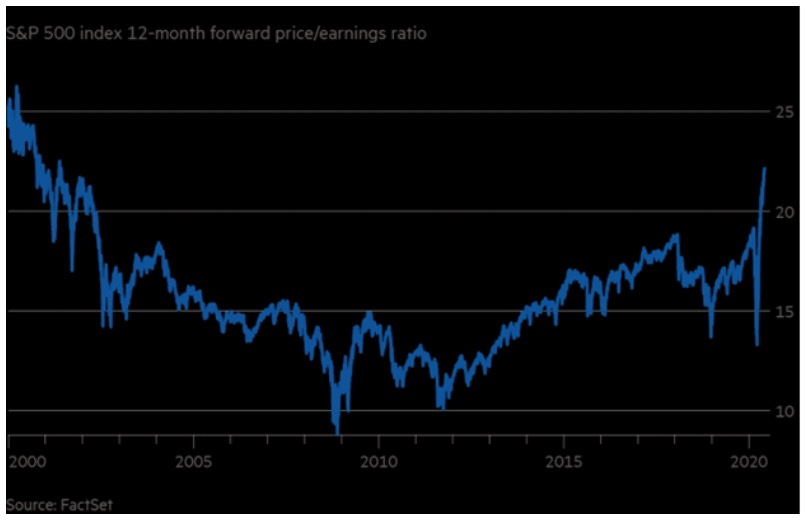

For much of the past three months investors have really viewed any data in a ‘win-win’ scenario. If the data is stronger than expected then investors jump onto the recovery narrative and shift money towards cyclically-oriented sectors such as discretionary spending, energy, financials and airlines. On the other side, any weaker data seems to reinforce the thesis that more central bank ease and/or government programs will have to be enacted to get the data turned around. This usually leads to a resurgence in the highly-valued growth stocks which benefit from longer period of low interest rates. The bottom line is that ‘hope’ and low interest rates continued to fuel the rally. But, in the end, ‘all roads must lead to Rome’ meaning that there will have to be better economic data at some point in time to sustain these moves. Record low interest rates can push valuations to extreme levels (see the chart below which shows the S&P500 Index at the highest valuation levels it has seen since the ‘tech bubble’ 20 years ago) but without earnings growth the valuations eventually become unsustainable. Quite honestly many of us thought those ‘sky high’ valuations of the late 1990s were a ‘once in a lifetime’ occurrence. All it took to get there again was a global health pandemic and some of the worst economic data in 80 years!

When people wondered in March who would make up for the buying power lost in the stock market as companies stopped doing buybacks, “small-time day traders” wasn’t the answer most expected. But as American companies retreat from buying their own shares to preserve cash during the coronavirus pandemic, retail investors have stepped in, lured by a flood of economic stimulus. While net corporate demand is likely to plunge 80% to US$100 billion this year as repurchases slow and share offerings increase, the decline is being partly offset by a roughly US$270 billion increase in buying by households. In much the same way as the extremely easy money policies post the Financial Crisis actually encouraged companies to borrow at cheap rates and use the funds to buy back their own stocks, we may now be seeing something similar at the individual level as the swath of stimulus cheques and a lack of venues for risk taking has sent money surging into the stock market. Broker data show a surge in retail equity trading activity as foreign investors and households supplant corporations as the largest 2020 source of U.S. equity demand. It’s a turnaround from the previous four years, when companies spent more than US$2 trillion buying back their stocks, dwarfing every other category of investors, according to Federal Reserve data compiled by Goldman.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.