Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

May 6, 2021

The stock market continued to work higher in April despite some volatility towards month end. Canadian stocks rose by another 2.2% to push their ‘globe leading’ gain for the year to almost 10%. U.S. stocks also pushed higher, driven by strength in the cyclical and transportation sectors and supported by snapback rallies in the big technology stocks. European stocks also added to their gains despite some weakness in the headline economic numbers due to the renewed shutdowns in the major EC economies. Better vaccinations and more re-openings helped the French and British markets buck the European softness with those markets each gaining over 3%. In Asia there was some weakness as a slowing recovery in China, softer Japanese results and record new levels of Covid infections in India muted the gains in those markets. Rising yields pushed bond prices lower again in April, after registering their worst quarter in decades to start the year. Surging growth in the U.S. and some worries about inflation risks have taken the shine off the fixed income market this year. Commodities were the big winners in April, though, as copper and lumber surged to record highs on economic re-opening, oil markets showed renewed strength on continued supply restraint and the U.S. dollar rally once again lost some momentum, providing a tailwind for commodities.

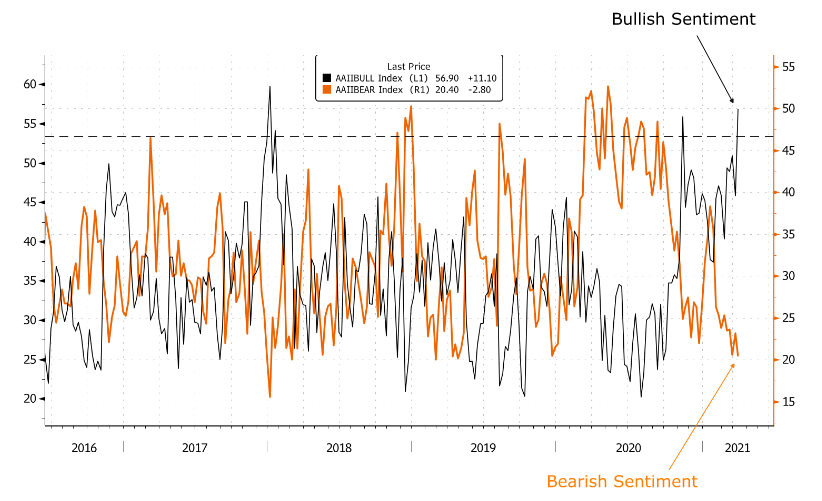

Among the many big events of the past month, the first quarter earnings reports drew the most attention from stock market investors. Expectations were already high as companies were finally starting to ‘lap’ the miserable first quarter results of 2020 which included the first month of the Covid lockdown. Despite the ‘bar being set so high’, companies were still beating even those optimistic predictions, as almost 90% of companies reporting thus far surpassed expectations. In fact, ‘surpassed’ might be a true understatement as the largest players, including Microsoft, Apple, Google, Facebook, Qualcomm, Texas Instruments, Bank of America, JP Morgan, Goldman Sachs, 3M and Caterpillar, all ‘demolishing’ the expectations. Stronger economic growth, low interest rates, improved operating margins and improved overall execution all contributed to the results. If there was any disappointment, it was the fact that many of those stocks actually traded lower after the reports. One of our ‘cardinal rules of investing’ has always been to beware of stocks that don’t react positively to good news (and conversely looking for opportunities when stocks no longer fall on negative news). Clearly investors had already priced in some pretty good news with stocks trading at record levels and near ‘record high valuations.’ Not only was the good news priced in, investors are also positioned quite bullishly if the AAII Sentiment Data shown below is any indication. Bullish Sentiment at almost 60% and Bearish Sentiment down to almost 20% is a spread not seen since late 2017, just a few months before sharp corrections in the first quarter of 2018 and again in the fourth quarter of that year.

The market has had a pretty much ‘straight up’ move over the past 13 months and is likely well overdue for a correction at some point. Guessing the timing of such a correction, though, is rarely a successful investment strategy, so we are not actively selling down our stock portfolios despite some probably short-term volatility. The bigger picture is that we are still relatively early in a new economic cycle and the earnings gains are likely to continue, even if not at the blistering pace of ‘beats’ as this past quarter. While we could easily get a 10-15% correction in stock prices at any time, particularly given elevated sentiment and valuation levels, the reality is that stocks could also get carried another 10-20% higher by the strong current momentum before seeing any correction. The better strategy, in our view, is to remain invested but try to reduce portfolio volatility by favouring under-valued cyclical sectors of the market and by having some hedges in the portfolio such as Treasury bonds, gold stocks and high dividend payers such as pipeline and telecom stocks.

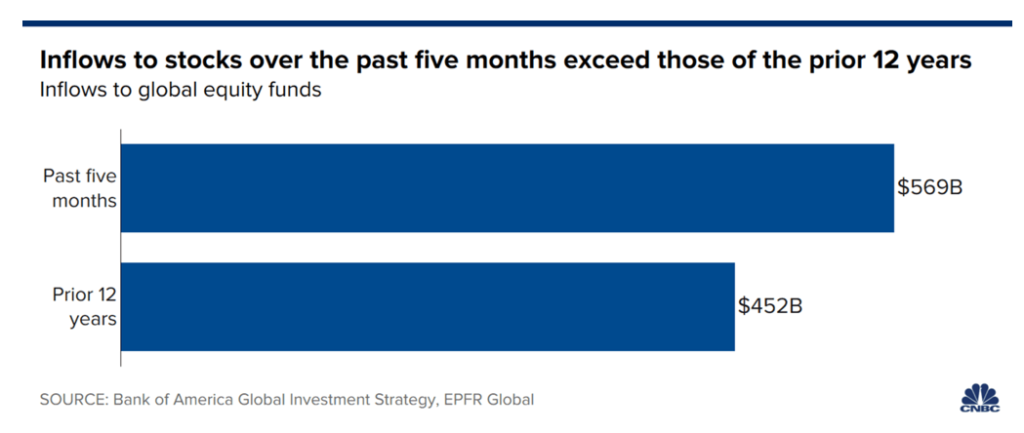

Not only is sentiment showing extremely bullish readings, but investors are also putting their ‘money where their mouths are’ in terms of actual market positioning. The latest wave of market enthusiasm has brought with it a stunning rush of money, in which more of investors’ cash has gone to stock-based funds in the last five months than the previous 12 years combined. Those numbers easily could exacerbate ongoing worries about financial market bubbles as valuations are around the same levels as just before the dot-com bubble popped in 2000. Again, more reason to be cautious but not enough to justify a wholesale move out of stocks, since indicators such as these have never ben particularly accurate market-timing tools.

The most pervasive argument for remaining invested in stocks at this time is the strength and early age of the current economic recovery. U.S. economic growth accelerated in the first quarter, fueled by massive government aid to households and businesses, charting the course for what is expected to be the strongest performance this year in nearly four decades. The U.S. economy expanded 6.4% annualized in Q1, up from a 4.3% pace in the fourth quarter of 2020. While output is still down a touch from pre-COVID levels, it’s safe to say that a full recovery will be reached in the second quarter. That would be just six quarters from peak to full recovery, which is impressive considering the hole was the deepest one seen in the post-war era. It took the economy 3½ years to recover after the financial crisis in 2008/09, but that was a much different credit-driven downturn. Looking ahead, we continue to see strong momentum into 2022 as the economy more fully reopens.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.