Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

May 6, 2021

The U.S. economy is rebounding more quickly than its global rivals, thanks to two additional rounds of COVID-19 relief money from Washington as well as easing anxiety over the pandemic, which has boosted domestic demand and allowed services businesses like restaurants and bars to reopen. There are concerns among some economists that the massive government funding could ignite inflation, but Fed Chair Jerome Powell expects this higher inflation to be “transitory”, arguing that the labor market remains 8.4 million jobs below its peak in February 2020. Though the labor market recovery is back on track, it will probably take a few more years to recover the more than 22 million jobs lost during the recession. For these reasons, the Fed indicated that they would be keeping their very ‘easy money’ policies in place for now and would not be reducing the Quantitative Easing program that has the Fed buying $120 billion of Treasury Bonds every month. This effectively ‘monetizes’ the substantial debt being run up by the US government as is continues to run massive budget deficits to support growth.

Not sure how this one plays down in Mar-a-Lago but, despite the warnings to the contrary, the S&P500 has risen 10% since President Joe Biden’s Jan. 20th inauguration. The index is on course for its strongest performance since the start of Franklin D. Roosevelt’s first term in 1933, when it surged 80% after a spectacular crash in the Great Depression, according to a Dow Jones Market Data analysis. By comparison, the S&P500 rose 5.3% in the first 100 days of President Donald Trump’s term in early 2017 and on average has gained 3.2% over that period in presidential terms since Herbert Hoover’s in 1929. Investors recognize it is no surprise that bountiful spending, increasing vaccinations, growing faith in the economic reopening and continued support from the Federal Reserve have powered the latest leg up in the stock market.

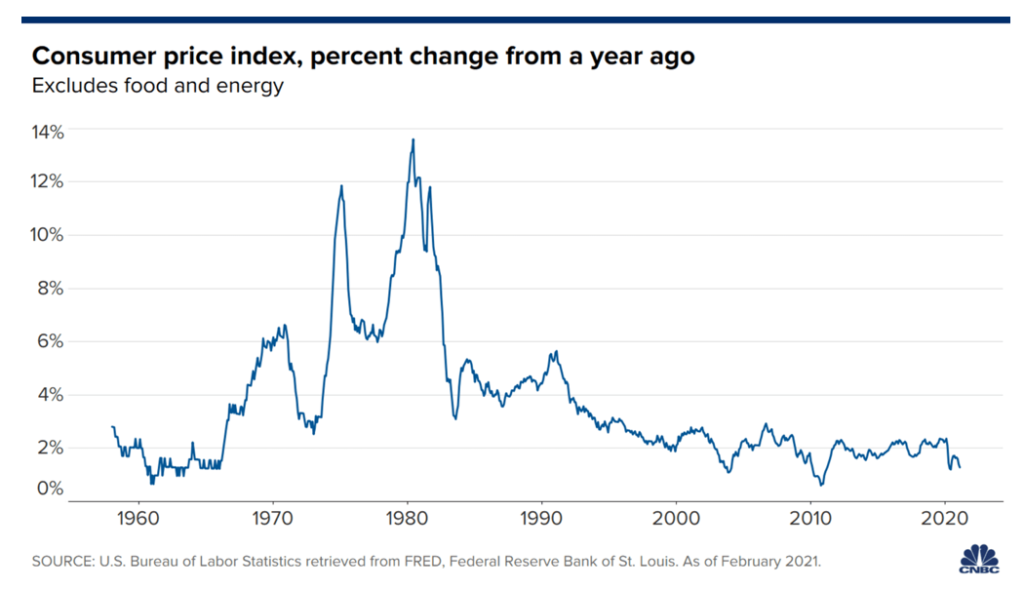

The one big risk that could really ‘upset the apple cart’ for investors in both stocks and bonds would be the return of inflation. The inflation risks are real too, since we have never before seen the type of global monetary expansion that we have seen in past decade in general, and the past year in particular. While inflation is the focus for central banks, it really has been in a low range for the past two decades, coinciding with both the globalization of most businesses as well as the broad penetration of technology into all aspects of business and consumer behaviour. Central banks have indicated a willingness to allow a higher inflation for a short period of time before moving to tighten money, but financial markets have clearly been levitated for some time now on the belief that interest rates will remain ‘lower for longer.’ A period of sustained higher inflation would change that outlook and present a real risk to the stock market.

But the great University of Chicago monetarist, Milton Friedman, famously said, “inflation is always and everywhere a monetary phenomenon’, meaning that the excessive printing of money will always lead to its devaluation. One of my university economic professors from many decades ago once rebutted the simplicity of that statement with his own premise that ‘the price of pencils is always and everywhere a pencil phenomenom!.’ Point taken. You create too much supply of anything and you depreciate its value. Wasn’t the ‘tulip mania’ bubble of almost five centuries ago just such an example? Bottom line here, if all this new money starts to find its way into the real economy instead of just stock buybacks and savings, then we will really see some rising price levels across the board and the U.S. Fed and other central banks will be forced to remove their ‘easy money’ policies. Maybe that’s what the prices of lumber and copper are telling us right now, and that is the real risk for the stock market. For now, we’ve got an ‘all clear’. But we need to remain wary of the inflationary risks.

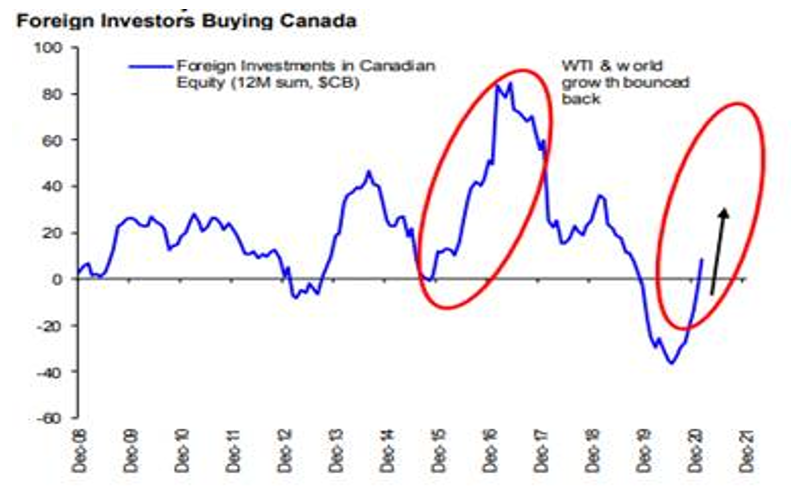

Canadian stocks, after a decade of underperformance relative to the U.S., are starting to show some relative strength in 2021. The recovery of the Financial, Basic Materials and Energy sectors, all heavyweights in the Canadian index, has helped fuel those relative gains. Rebounding commodity prices and stronger employment numbers have also helped the Canadian economy despite continued provincial lockdowns and the slow rollout of vaccinations. This all has pushed the Canadian dollar to a multi-year high, rising to 81 cents U.S, last month. This has also drawn foreign investors back into Canadian stocks, and not just the cannabis names! The chart below shows how the flows have reversed back up after a five-year downturn.

Canadian banks should be a big beneficiary of these money flows. Their valuation relative to U.S. financials is attractive and the capital levels are far superior. Canadian banks are sitting on massive excess liquidity since they haven’t been allowed to do share buybacks or increase dividends. Meanwhile, the loan loss provisions they took last year when the pandemic broke have proven to be more than sufficient, particularly since governments backstopped some of highest risk business clients and provided additional support to consumers and small businesses. At the same time, a booming housing market and recovery in the stock market have reaped windfall gains for both the lending and capital markets businesses. After seeing how U.S. financial stocks have blown through first quarter earnings estimates, we look forward to seeing similar results when banks here start reporting their second quarter results in late May. We continue to own CIBC, Scotia and Bank of Montreal as well as Manulife and CI Financial Corp in that sector.

Finally, after the blowout earnings from all the big tech stocks in the U.S. (Alphabet/Google, Apple, Microsoft, Facebook and Amazon), it’s hard to argue against owning these stocks for the long term. While the valuations are clearly extended for the group, the results show that all these companies continue to dominate their respective market niches, are generating substantial free cash flows and have established themselves as market leaders. While valuations may not rise from here, and may in fact begin to contract as interest rates nudge higher, there is a clear case for continued growth in all of these companies. That alone argues for some level of holding in all stock portfolios. The iOS and Android operating systems (Apple and Google) are the dominant (and basically only) operating systems for wireless devices. The online advertising industry is the largest source of advertising growth and is dominated by two players, Facebook and Google. Cloud computing is becoming a ‘must have’ for almost every business, service provider and consumer. The ‘cloud’ is basically being driven by three large players; Microsoft, Amazon and Alphabet. These companies are dominant players in the fastest growing and most important industries and the ‘engines of the new economy.’ We expect them to remain dominant for some time and use their massive free cash flows to increase their dominance. In our view, the decision is not whether to own those names, but more about how much to own! Given all that we have said above about the shorter-term risks we have slightly reduced our weight in those names, but would not be removing them from stock portfolios.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.