Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

April 4, 2019

Because oil is traded in a global market, it is often used as an indicator of global economic health. In the fourth quarter of last year, the price of oil plunged and that raised concerns that global demand was faltering. However, oil prices have recovered significantly since last fall. The price of the West Texas Intermediate (WTI) dropped from over $75 per barrel to under $43 in the fourth quarter but has since rebounded over $60. More importantly for Canada, the price of Western Canadian Select has recovered from a low of less than $15 last November to over $50 per barrel. That rebound should bolster the economic performance of the oil-producing provinces, which have been lagging the rest of Canada. In addition, rising energy prices should lead to an acceleration in inflation that will make the Bank of Canada reluctant to lower its interest rates.

Another reason that we are optimistic that economic growth will improve is the U.S. election cycle. U.S. growth has slowed from the robust pace of the second and third quarters of 2018, and we believe the admittedly unpredictable U.S. administration will try to boost growth to improve its re-election chances in 2020. Given the negative effect of the various U.S. protectionist measures on U.S. businesses (due to retaliatory tariffs, increased costs, and uncertainty), we think there is a good chance that some measures such as the steel and aluminum tariffs will be lifted, which would be a mild positive for Canadian growth.

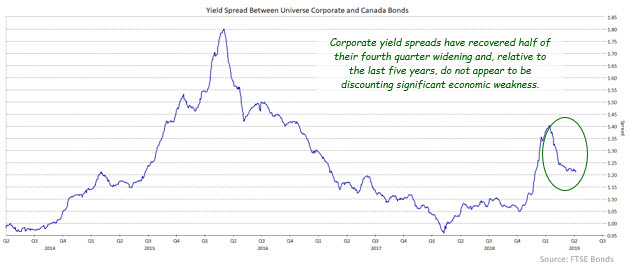

We believe that as the Canadian economy continues to exhibit positive economic growth, the pessimism that pushed Canada bond yields below the Bank of Canada’s 1.75% overnight target will dissipate and yields will rise. Accordingly, we have positioned the portfolios defensively, with durations shorter than their respective benchmarks. That said, we do not expect the Bank of Canada to change its interest rates either up or down this year. We also believe that the yield differentials for bonds of different terms out to 10 years are too small. We have, therefore, structured the portfolios to benefit from a steepening of the yield curve. Our sector allocation strategy is maintaining a moderate overweight of the corporate sector, but we are looking to further improve overall credit quality given the current stage of the economic cycle.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.