Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

April 4, 2019

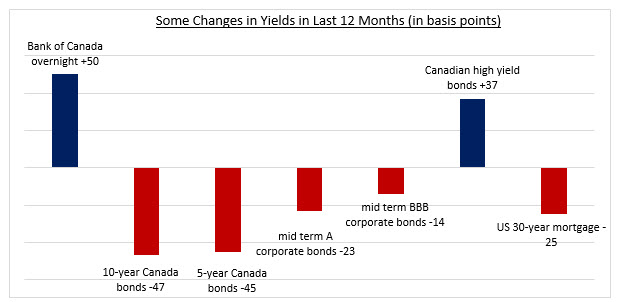

To the extent that the recent slowing of growth was caused by central bank monetary tightening and higher interest rates, the rally in government bonds and the resultant plunge in yields in the last few months has led to an easing of borrowing costs that should mitigate some of the economic weakness. Canadian mortgage rates have not yet responded to the 100 basis point decline in 5-year Canada bond yields since October, but that seems highly likely given historical patterns. When mortgage rates do decline, it should help increase demand in the housing sector. And, notwithstanding the Bank of Canada raising its interest rates by 50 basis points over the last twelve months, most bond yields (except for junk bonds) have actually fallen. And in the United States, the 30-year mortgage rate has fallen in spite of the Fed raising rates 75 basis points.

Not all investors are as pessimistic about near or medium term economic growth as government bond investors. Equity markets have rebounded from corrections in the second half of 2018 and are not displaying concern about a possible recession. In the bond market, credit spreads for investment grade issues have recovered roughly half of the widening that occurred in the fourth quarter. With benchmark government bond yields falling sharply in recent months, many investors are buying corporate bonds to improve their yields and do not appear worried about the risk of a recession.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.