Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

May 14, 2020

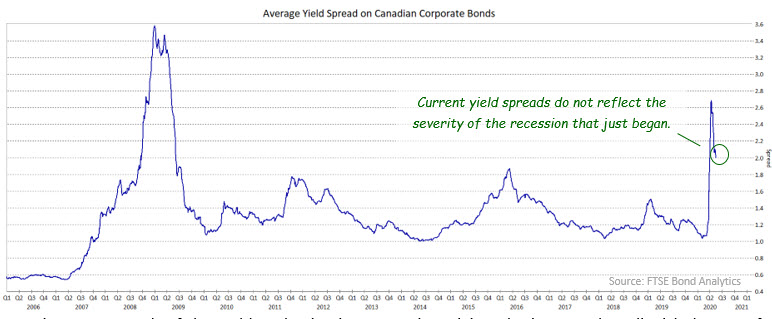

Corporate yield spreads widened very sharply in March, but never reached the widest levels hit in the 2008-2009 financial crisis. Subsequently, the Bank of Canada’s announcement of a $10 billion corporate bond purchase programme and investors’ fear of missing out on any corporate rally led to a partial reversal of March’s spread widening. We are skeptical that the recent narrowing of spreads is appropriate given how recently the recession started, its severity, and the unpredictable impact on corporate creditworthiness. The spread widening that occurred in March reflected a revision to corporate risk premiums as a result of the sudden slowing in economic activity. The

increased credit risk due to a far more severe recession than the financial crisis has not been significantly reduced by the Bank’s plans to purchase bonds. At this point, corporate profitability for the next few quarters is very difficult to predict. With unemployment possibly as high as during the Great Depression of the 1930’s and the economic recovery likely to take years, we believe it makes prudent sense to be cautious about the corporate sector at this time. Accordingly, we have been increasing the average quality of the holdings and looking for opportunities to reduce the overall corporate allocation. We continue to avoid sectors such as retailing, resources and real estate, and have reduced exposure to autos and subordinated bank debt.

With regard to the provincial sector, the size of the Bank of Canada’s purchase programme and the federal government’s implicit support makes us slightly more optimistic about that sector, but we recognize the risk of ballooning fiscal deficits.

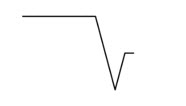

Economists are arguing about the potential shape of the recovery. Some believe the rebound will be rapid (V-shaped), while others anticipate it will be somewhat slower (U-shaped). Still others are more pessimistic and anticipate the recovery will not begin for a year or two (hockey stick shape). Our estimation is different again; we look for a partial, quick rebound followed by disappointingly slow growth that makes full recovery some years away. Our choice of shape would be a flipped square root sign as in the following:

As this is being written, Tiff Macklem has been appointed the next Governor of the Bank of Canada. He will take over from Stephen Poloz on June 2nd. Dr. Macklem is a former Senior Deputy Governor of the Bank who lost out to Poloz as Governor seven years ago. Given his previous experience at the Bank, we do not anticipate any significant change in policy as a result of his appointment.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.