Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

May 14, 2020

As noted above, having lowered their interest rates as low as they could go in March, global central banks took additional steps in April to mitigate the impact of the sudden recession on their respective economies. The most aggressive central bank in this regard was the U.S. Federal Reserve. In the 2008-2009 financial crisis and its aftermath, the Fed had purchased only government issued bonds and mortgage-backed securities. In April, the Fed cast a wider net, deciding to purchase corporate bonds for the first time, and not just investment grade ones. The Fed said it would purchase some types of high-yield bonds, collateralized loan obligations and commercial mortgage-backed securities. It also said it would loan up to US$2.3 trillion to small and mid-sized businesses and state and local governments. The amazing breadth of the Fed’s programme led one observer to quip “I think I have a buyer for that old bike in your garage…you guessed it…your local central bank. Global central banks are seemingly buying any assets they can find.” The Fed’s buying announcements spurred a surge in demand for corporate bonds that allowed record new issuance of US$292 billion in the month.

The Bank of Canada’s bond buying programmes were somewhat more circumspect than the Fed’s, but still surprised the bond market. In mid-April, the Bank announced that it would be buying up to $50 billion of provincial bonds with maturities limited to 10 years or less. The amount coincided with several estimates of additional provincial spending to offset the impact of the recession. While the purchase programme had been partially anticipated, provincial yield spreads at all maturities tightened sharply after the Bank’s announcement. In a surprise move, the Bank also announced it would be purchasing up to $10 billion of corporate bonds. The eligible corporate bonds must have ratings of BBB or better, maturities of 5 years or less, and not be from a financial institution. It is estimated that only $80 billion of outstanding bonds would qualify, meaning the Bank will be trying to buy up to 12.5% of the available bonds. Notwithstanding the relatively small portion of the corporate bond market that qualifies, the Bank’s announcement sparked a sharp rally in the yield spreads of almost all Canadian corporate bonds.

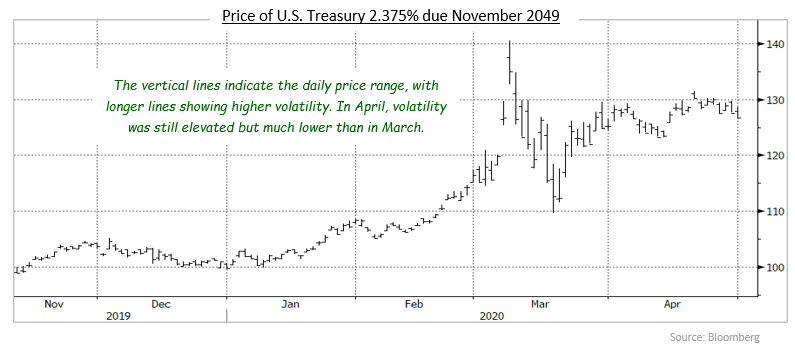

The extreme volatility in government bonds that we had noted in March subsided in April. However, daily swings in prices remained higher than in the months prior to the pandemic. The price chart we showed last month for a long

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.