Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

November 6, 2017

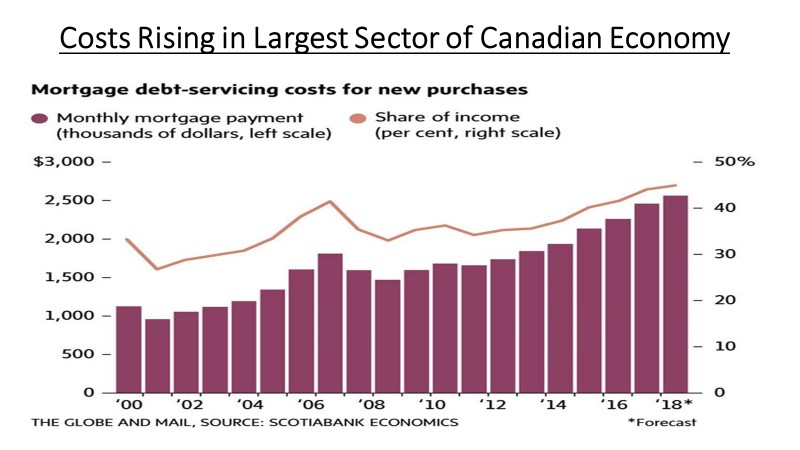

The cost of home ownership in Canada continues to rise, adding to the risk in the country’s somewhat ‘inflated’ housing market. To put that in perspective, those increases will “easily” eclipse the rise of about 2.5 per cent in average annual per-capita income. Average mortgage carrying costs among new buyers are estimated to climb by about 8% next year. Deteriorating housing affordability, moderately higher borrowing costs, and consecutive rounds of regulatory policy changes have moderated national resale activity. Much of the recent slowdown in sales and softening in prices has been concentrated in the Greater Toronto Area and surrounding municipalities, and follows the implementation of a series of provincial measures in the spring of 2017.

In terms of the impact of the real estate slowdown in some of the key urban centres on bank earnings, we keep thinking that this will eventually be a ‘revenue event’ not an ‘earnings write-off’ event. What we mean is that, even though sales are down year-over-year and price gains have reversed, we don’t think you will see any negative impact from mortgage issues at any of the major banks. They just don’t have large exposure there anymore and it is better hedged than it was in the past. The negative on bank earnings from a housing slowdown will come further down the road, in my view, when the downturn in housing starts turning into slower/negative growth in the economy since the housing boom was so much more responsible for jobs, growth and spending than most people realize. Housing and related industries now account for about 25% of the Canadian economy, more than double that of the energy sector. When we think about how many ancillary jobs have popped up due to the strong housing market, such as home staging businesses, storage etc. But housing is in the process of peaking and I think it will lead to slower growth in Canada, including less loan growth. We are already seeing weaker economic numbers in Canada after the booming first half. The Parliamentary Budget Office seemed to echo the view that the best growth is behind us and a multi-year slowdown period is ahead. In its most recent report they wrote “we project real GDP growth to slow from 3.1 per cent in 2017 to 1.9 per cent in 2018 and then to 1.8 per cent in 2019 before averaging 1.7 per cent annually over 2020 to 2022.”As growth slows down then we will see the impact bank earnings. It is one reason why we currently don’t hold any Canadian bank stocks in our portfolios.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.