Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

November 6, 2017

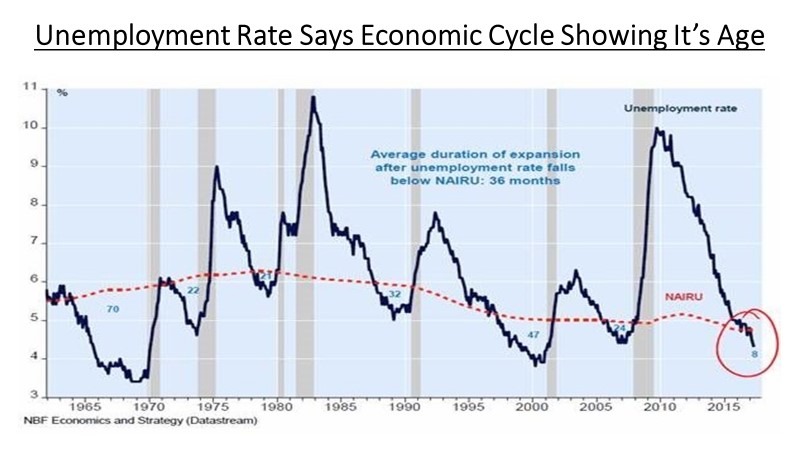

Looking at the long-term picture, when the unemployment rate has dropped below NAIRU we generally see a recession develop. While the timing clearly differs, it is hard to argue against the view that this cycle has gone on for longer than normal and that inflationary risks are rising. That view has been echoed by the U.S. Federal Reserve members in defense of the four interest rate increases they have enacted in the past 12 months. More bullish investors would point out that, in the great stock market of the 1990s, the UE rate dropped below NAIRU almost four full years before the recession began. But, no matter how you cut it, the reality is that inflationary pressures have always increased when unemployment dropped to such low levels and the current skilled labour shortage in the U.S. is a clear example of how this leads to wage pressures and then higher interest rates. Those higher rates are what put stock market valuations at risk. The interest rate holiday is what fueled this financial asset bubble and it will also be its undoing!

Another risk that we see right now is the bullishness of the average investor. In terms of sentiment, the difference between bulls and bears hasn’t been this high in 30 years, according to the latest Investors Intelligence (II) reading. Bulls in this week’s II survey totaled 63.5% against just 14.4% for bears. That’s a spread of 49.1 points, well above the level that represents potential danger in the market. A spread above 30 points signals “elevated risk” while 40 points calls for “defensive measures.”

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.