Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

May 30, 2020

There are also some other significant market risks that have crept into the picture in the past month that have yet to fully incorporated into the investment outlook. Topping that list would be a recent escalation in China-US trade tensions, which have threatened both to scuttle the Phase One trade deal signed late in 2019 and disrupt the supply chain for semi-conductors and other key industrial products that are so dependent on global trade. This risk appears to have grown as the U.S. put more of the blame on the Covid-19 epidemic at China’s feet. The U.S.-China relationship took another beating as the White House rolled back some of Hong Kong’s special treatment after Beijing imposed a national security law that further eroded the territory’s autonomy. The U.S.-China relationship has hit a low point, including new technology restrictions against Huawei Technologies and increase scrutiny of U.S. listed Chinese companies.

Other notable risks are cited in the Citibank Panic/Euphoria Indicator, which is now back to euphoric levels, suggesting there is a 70% likelihood that markets are lower in following twelve months. Also, Citi’s Risk Positioning Monitor shows that recent moves higher in equities have been driven by significant short covering.

The Canadian economy took a historic dive in March, as the country imposed lockdown measures to curb the spread of COVID-19, and worse results are expected for April.

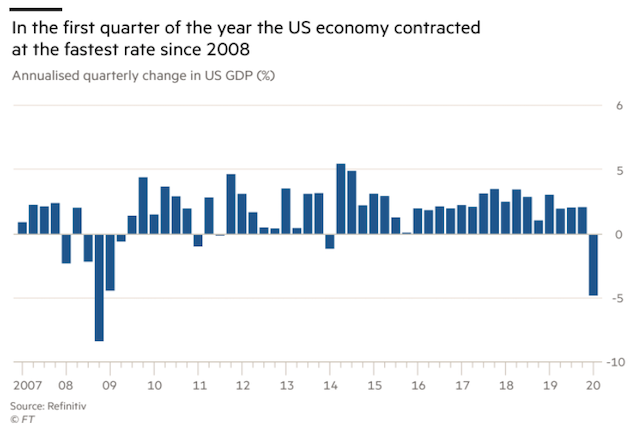

Real gross domestic product fell 7.2% in March, the largest monthly decline on record, Statistics Canada reported. In the first quarter, real GDP shrank at an 8.2% annualized rate, the sharpest drop since the financial crisis of 2008-09. StatCan estimates an 11% decline in real GDP in April, the first full month with lockdown restrictions in place. South of the border we saw similar results as the U.S. economy’s first-quarter contraction was also slightly steeper than initially estimated. Also, a key measure of corporate profits weakened as the coronavirus and related shutdowns began to have a more pronounced effect on consumers and businesses. Gross domestic product—the value of all goods and services produced across the economy—fell at a 5.0% annual rate in the first quarter, the largest quarterly rate of decline since the last recession. Most economists expect a bigger contraction in the second quarter, when lockdowns continued for weeks before states started slowly reopening their economies. Second quarter will be even worse

Second quarter will be even worse

Given all the economic risks noted above and the fact stocks have had one of the most significant recovery on record in the past two months, we find it prudent to be once again reducing stock market exposure to average levels and will reduce to underweight on any further strength, more quickly if we get indications that even our pessimistic recovery outlook is proving too positive. Reductions of weights in sectors included financials, energy and technology, where we still hold core positions in all but in reduced scope. We have maintained positions in the precious metals sector (gold and silver) as well as telecom and pipeline stocks, mostly for their higher dividend yields and safer earnings profiles. We still find the risk-reward trade-off in both bonds and preferred shares as somewhat unfavourable so have not added to positions there, remaining under-weight in bonds and market-weight in preferred shares. Cash positions have therefore built up in portfolios both as a source of liquidity for any pullback in stocks and/or preferred shares. In our Hedge Fund we added short positions in key U.S. indices (S&P500, Nasdaq and Russell2000) which acted as hedges against long positions in Canadian telecom, gold and pipeline stocks as well as U.S. industrial and technology stocks. The Fund was net-neutral on equities at month end after having been ‘net long’ 70% at the end of March and ‘net long’ 40% at the end of April.

With stock buybacks waning, how companies manage their dividends will take on new importance as investors make judgments about equity valuations. In the current viral crisis there has developed a “social aversion” toward buybacks since they are seen as favouring larger, wealthy investors and corporate insiders who are the biggest beneficiaries of these programs which, until recently, had been a popular way for large U.S. companies to return capital to shareholders. But amid the coronavirus pandemic and its economic fallout, many companies have suspended buying back their shares, even though they continue to pay a dividend. That includes large banks such as JPMorgan Chase, Bank of America and Citigroup, which were among a group of financial institutions to suspend buybacks in mid-March. Unlike dividends, buybacks have been portrayed as a return of capital that doesn’t make financial sense at a time when capital conservation is a focal point for many companies. Also, some observers have criticized buybacks as having contributed to the weak financial position of many companies heading into the crisis.

But dividends are ready and able to step in if buybacks are about to lessen in importance. Dividends are more powerful signals of management confidence in the business than buybacks since they are meant to be sustainable through a cycle. Most importantly though, with bond and cash returns so low the relative attraction of dividend paying stocks has gone up dramatically. Our focus in managed portfolios has been to add higher dividend paying stocks with safe, non-cyclical earnings profiles.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.