Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

December 31, 2018

Why have longer-term interest rates fallen in the back half of 2018 when central banks have been tightening policies and raising short-term interest rates? The simple explanation is that they are moving lower in anticipation of slower economic growth, despite the continued rhetoric from the U.S. Federal Reserve that growth remains exceptionally strong and they expect to raise short-term interest rates two more times in 2019. Also, consumer confidence readings lately versus economists’ expectations are falling short by a magnitude and consistency last seen prior to the recession in 2007. Receding sentiment indicators have always been a signal of economic weakness ahead.

Money flows are also heading in the wrong direction for the first time in three years. December has been particularly rough as investors have pulled over $75 billion from mutual funds and exchange-traded funds that track stocks this month, the biggest exodus from stock funds in a single month ever, according to Lipper Analytics data going back to 1992. Sentiment is also reversing. For the first time since 2013, the majority of mom-and-pop investors said they believe stock prices will drop over the next six months, according to a survey by the American Association of Individual Investors in their most recent report. Fewer than 32% of investors said they expect to see prices rise over that period. One key warning signs for stocks that we paid attention to at the beginning of the quarter was the breakdown of some key stock leadership groups, namely the Financials and the Semi-conductors. If neither of those groups can rally, it is usually a very bad economic sign since they are both key determinants of economic growth, in so much as financials reflect loan growth and semis are the front end of technology spending.

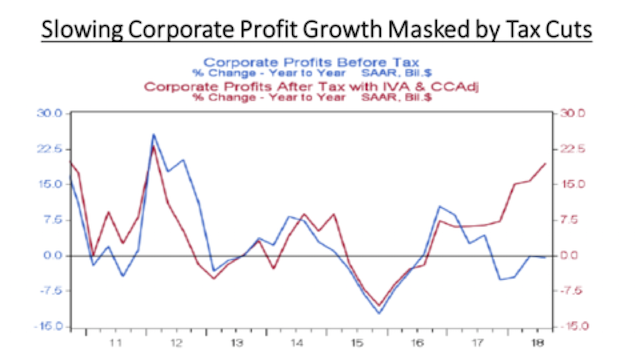

There has been a lot negative economic news recently, with some analysts forecasting a significant economic slowdown and even a recession in the near future, a forecast driven by the U.S.-China and U.S.-European Union trade wars. Trade wars among powerful countries such as these are a recipe for economic growth destruction. History has provided us with a lot of insight in that respect. Moreover, when you add the potential of slowing economic growth to rising interest rates, the issue of global debt comes into play. Global debt at both the consumer and government level has been on the rise for years, reaching a record high in 2017. This was not a problem when economies hummed along and interest rates were at rock bottom. But with economies slowing down and interest rates rising, these excessive debt levels start to become a serious issue. In light of all this, the U.S. corporate sector is widely expected to experience weakening earnings, possibly a “profit recession,” as profit margins are squeezed by rising costs and reduced economic growth. Profit growth has been the backbone of the bullish story for stocks in the past two year. However, as shown in the chart below, profit growth has been ‘super-sized’ by the 2017 tax cuts. Underlying ‘pre-tax’ profit growth has not been nearly as buoyant and actually has shown no growth in the past year. As the impact of the tax cuts disappears in 2019, we believe that profit estimates will have to be cut by most analysts.

While the bulls could effectively argue that the recent weakness in stocks is already reflecting a sharp slowing in profit growth next year, we still have no idea what the magnitude or duration of the slowdown will be.

Back on the home front, economic risks are being under-estimated, in our view. While the current trend on Canadian real GDP growth is 2%, the excess indebtedness is really the top risk, especially as we have yet to see the full lagged impact of the 125 basis points of rate hikes the Bank of Canada has implemented. Canadian household debt has expanded to $2.2-trillion, almost doubling in the past decade. That is equivalent to nearly 100% of GDP or about $150,000 a household – an untenable number. Moreover, it isn’t just consumer and mortgage debt. Canadian debt in aggregate, including households, businesses and all levels of government, now sums to nearly 290% of GDP. That is well in excess of numbers in China and Italy, which are both renowned basket cases when it comes to excessive leverage, but are closer to 260% all-in debt-to-GDP ratios. Even the United States, with its gargantuan fiscal stimulus and wave of bond-financed share buybacks this cycle, has a debt ratio of 250%. A recent Citigroup report warns that Canada risks a financial crisis within three years as rising interest rates collide with already lofty levels of indebtedness. Several other countries are also vulnerable, according to the Citi report titled, “Are we headed for a global debt crisis?” It estimates that governments, households and corporations around the world have amassed a mountain of loans roughly three times as large as the level of 20 years ago. “The outsized amount of debt, as well as the seeming pick up in the pace of accumulation, has raised concerns that the world is primed for a debt crisis.” It warns that rising interest rates could pose a particular threat to Canada, as well as Norway, Sweden, Australia and the Netherlands. In each of these countries, debt is high compared with the size of the underlying economy, and borrowing has been expanding rapidly compared to income growth. In addition, “house prices are also relatively high and may correct if interest rates rise.”

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.