Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

November 30, 2020

One of the many ‘old adages’ about the stock market says that “bull markets climb a wall of worry.” Clearly there has been no lack of worries over the past seven months as stocks rallied back to record levels after briefly suffering through what turned out to be the shortest bear market in history. But unlimited support from central banks and an unprecedented deficit-financed wave of government stimulus spending did much to offset the economic damage from the worst downturn since the 1930s. This financial support allowed stocks to rally all the way back to the old highs, despite continued economic uncertainty, rising virus infections worldwide and stock valuations that exceed all measures except those during the technology bubble of the late 1990s. Renewed bullishness over the vaccine news sent stocks to their best monthly results in over thirty years in November, lead by the ‘formerly weak’ recovery sectors such as banks, retail, airlines, cruise lines, restaurants, real estate, industrials and autos.

For investors, the bigger question now is where do we go from here? We continue to have an overweight in stocks, as we have since March, but with some shifts away from the ‘safety plays’ of the initial lockdown and towards the laggard sectors which would benefit the most from a global economic recovery in 2021. Some of the shorter-term risks have been removed in the past month, including decisive election results in the U.S. (even if they have yet to be fully acknowledged by the outgoing administration) and a wave of enthusiasm on extremely positive news on recent news about three potential vaccines with exceptional trial results. Market were also buoyed over the belief that a Biden administration will push a massive new stimulus spending program in the U.S. and his strong contacts on both sides of the aisle in the U.S. Senate, will help to achieve a bipartisan solution. Markets were also cheered by the expected nomination of Janet Yellen to the role of Treasury Secretary in the Biden administration. She is a well-known and liked entity on Wall Street and certainly less contentious than one of the more ‘progressive’ choices investors had been worried about. Putting all of this together, investors are clearly ‘looking across the valley’ of the current economic risks from the ‘second wave’ of shutdowns from the virus.

Having said all of that, the problem with looking ‘across the valley’ is that you ‘start to look down’ and realize how high you are.’ It’s our way of saying that we do see some shorter-term risks despite strong seasonality and have taken profits in some energy, technology and consumer names and reduced our overall equity overweight slightly. Key short-term risks include the inability to extend stimulus programs in the U.S. and negative earnings/economic revisions over the next few months due to the ‘second wave’ slowdown. Our biggest short-term concern, though, is how far investment sentiment is extended on the bullish side. While sentiment indicators are not a reliable market timing tool, it’s hard to ignore how far some of these measures have moved and how they match levels prior to market pullbacks in 2018 and earlier this year. Re-balancing of major pension funds into year-end alone is expected to lead to over $160 billion of stock sales into bond purchases. While this activity can be absorbed in a $95 trillion global stock market, $30 trillion of which is in U.S. stocks, it can send a flutter through markets nonetheless.

In terms of specific extended sentiment measures, portfolio managers surveyed by Bank of America boosted their equity allocations to the greatest overweighting since January 2018 and cut cash holdings to their lowest levels since April. Investors Intelligence also found that 59.6% of advisors it polled in the latest week were bullish, while the percentage of bears fell to 18.2%. The spread between bulls and bears, which has a historical average of around 8%, exceeded 40%, a level of exuberance that tends to be seen at market tops. The American Association of Individual Investors poll is even more extreme as the bulls soared from 38.0% to 55.8%. It was only at 26.2% at the end of September and is one of the sharpest moves in such a short time frame in the bullish positioning. Public investors have also been piling into the stock market. Data from EPFR showed inflows into global stocks in the last two weeks soared to over $70 billion, the biggest ever. The flows were led by U.S. and emerging market stocks. More concerning is that the buying has been on borrowed funds, as margin debt on the NYSE has exploded 18% from year-ago levels on record low interest rates, the reduction (elimination?) of trading fees and an onslaught of new online accounts.

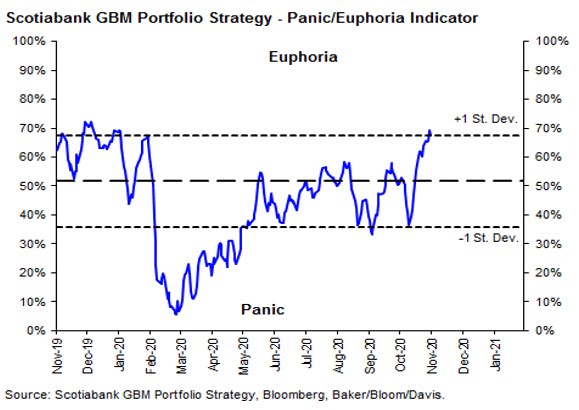

Putting much of such similar data together, we show the chart of the Scotiabank Panic/Euphoria Indicator over the past year. While none of these indicators should be taken as part of any longer-term investment strategy, they are worth paying attention to since there has been a pretty good correlation with ‘excessive euphoria’ indicators reaching high levels at or near stock market peaks, and the reverse when ‘panic’ rises.

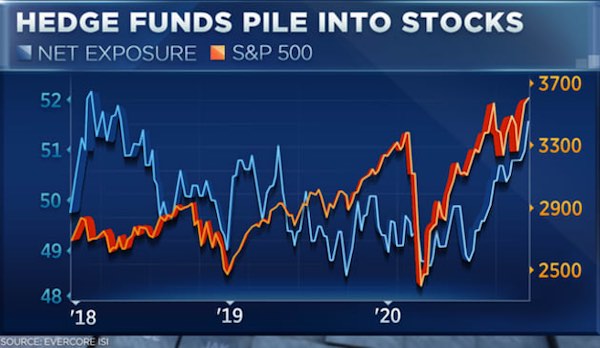

While all this suggests to us that stocks have probably gotten ahead of their underlying support in the short term, we have seen such indicators remain high for longer periods of stock market strength. We only have to look back to the ‘technology bubble’ of the late 1990s to see a period when valuations and sentiment were all well above their longer-term averages for a period of years. While stocks didn’t hit their cycle highs until March of 2000, Fed Chairman Alan Greenspan’s famous ‘irrational exuberance’ reference to the stock market took place back in 1997! Hedge funds and other tactical professionals, too, are pretty close to being “all in.” The Evercore ISI survey of hedge fund managers in the chart below showed net exposure to equities near a three-year high. Bottom line is that investors seem to be ‘all in’ on this move.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.