Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

November 1, 2018

A decline in U.S. growth would simply line-up with what we are seeing in the rest of the global economy. The OECD Leading Indicator has fallen for nine straight months now. The September China PMI data released recently show a material deterioration in the conditions for the industrial sector; something we have been concerned about for the past few months but had yet to flow through in the data; at least until now!

Traffic Problems Ahead? After nearly a decade of growth, new-vehicle sales in the world’s largest auto markets are entering their first sustained slowdown since the global financial crisis, putting pressure on profits as uncertainty around the U.S.’s trade policies looms. China’s once-booming car market is cooling, in part because of escalating trade tensions with the U.S. American demand for cars and trucks—long a bright spot for the global auto industry—has topped out, following a seven-year growth streak that helped lift earnings for many car makers and auto-parts suppliers world-wide. In Europe, where new-vehicle sales have benefited from the continent’s recovery, the car market is also softening as demand returns to prerecession levels. That is making profits harder to come by in a region where many car companies have long struggled to make money. While global demand remains robust, driven by continued economic strength, headwinds are gathering. Trump’s trade policies are undermining consumer confidence in many markets outside the U.S. and are widely seen as the biggest threat to continued economic growth. The weakening outlook comes as firms grapple with higher steel and aluminum prices stemming from new tariffs imposed by the Trump administration this year. Stiffening emissions regulations in Europe and China are also forcing auto manufacturers to spend billions of dollars on new technologies to curb tailpipe pollution.

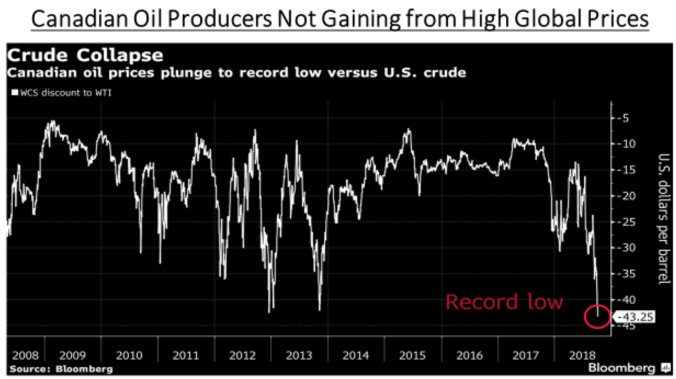

Have we hit bottom in Canadian Energy stocks? Western Canada Select’s discount to U.S. crude sank to US$44.50 a barrel in October, the widest on record in Bloomberg data stretching back to 2008. Canadian crude production recently surpassed available pipeline space, and even with the country’s producers signing contracts to move more crude by train, Canada doesn’t have enough rail capacity to alleviate the transportation bottlenecks. The country will need more pipelines and more domestic refining capacity to clear the glut, and those could take years to develop. Oil-sands producers are getting less than 40% of Brent crude price. This has been reflected in the very weak performance of Canadian energy stocks during the current bull market, despite the sharp rise in global crude oil prices.

The group is trading at the largest valuation discount to the overall market in more than a decade. Moreover, the group is positioned to generate significant levels of free cash flow over the 2019-2021 period. We expect the Canadian Large cap group to generate roughly $78 billion in free cash flow over the 2018-2021 period This represents roughly 30% of the current enterprise value of the Canadian group. We do not believe this change in the financial position of the industry is reflected in current valuations, which would retreat to record lows if current market values are maintained.

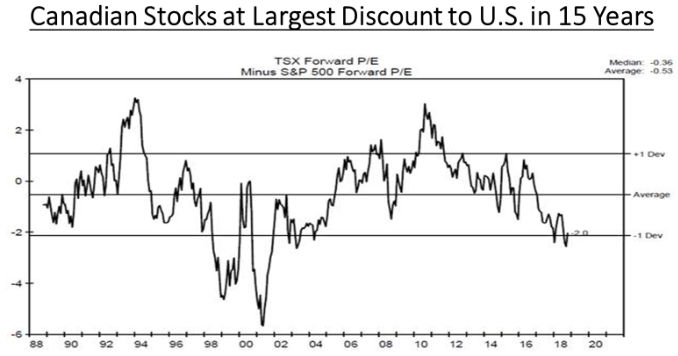

Are we finally seeing an opportunity for better Canadian stock market performance? Shares of the industrial metals and bulk commodity producers continue to come under pressure, in part due to increased expectations for a slowdown in global demand over the next one to two years. On the surface, selling a cyclical stock at the peak of a demand cycle is logical. However, there have been meaningful improvements within the metals, mining and other industrial sectors that make up a substantial part of the Canadian economy compared prior economic cycles, suggesting these sectors may meaningfully better positioned to withstand a slowdown in global demand than they have in the past. Meanwhile, the discount being applied to Canadian stocks compared to the U.S. market is approaching the widest levels ever seen, at the end of the technology bubble and before the commodities boom of 2003-2008. As it stands now (and shown in the chart below), Canadian stocks are already trading at the largest discount to U.S. stocks in 15 years.

The lack of high growth “FANG’ names in Canada and worries about an inflated housing sector and record consumer debt levels have certainly hurt capital flows into Canada. Combined with the mass exodus of funds out of the energy sector (due to structural, regulatory and pipeline worries) as well as weakness in the commodity sector in general valuations on this side of the border have been decimated. But a lower Canadian dollar, the assumed signing of a renegotiated NAFTA and other operating improvements at the company level should all help to insulate Canadian earnings better in any downturn than in the past. If global investors start to acknowledge these improvements and allocate capital accordingly, Canada should see a pickup in relative stock performance, similar to the 2003-2011 period. As we have always seen in the past, once all the bad news is fully reflected in current stock prices, the bottom is near! That would be much needed good news for Canadian investors in the year ahead.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.