Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

June 4, 2024

Many investors, ourselves included, have been looking at the small cap sector of the stock market for opportunities since the large cap stocks have rallied so much more and the valuation differential between the two groups is near record levels. But investors need to be careful even if small-cap stocks are as cheap as they’ve been in decades. First off, with more than half-trillion dollar mountain of debt looming over the next five years, it’s going to take a significant risk-on signal from the Federal Reserve to entice investors. Firms in the small-capitalization Russell 2000 Index hold a total of $832 billion in debt, 75% of which needs to be refinanced through 2029. For comparison, companies in the big-cap S&P 500 Index have just 50% of their obligations due by then. Also, smaller companies tend to have a considerable amount of floating-rate debt, usually in the form of loans, because they often aren’t big enough to borrow in the bond market. That means their interest expenses often reset higher soon after the Fed hikes rates, while a bigger company with fixed-rate bond debt may wait longer before higher rates have a significant impact on their borrowing costs. In addition, the performance of small companies typically is tied to how the overall economy is doing. Small caps are increasingly money losers, with about 42% of the Russell 2000 currently posting negative profitability, compared with less than 20% in the mid-1990s. With economic conditions in flux and uncertainty the theme in markets at the moment, we are somewhat skeptical about buying into these riskier stocks, even at seemingly bargain valuations. We see elevated stock market risk currently and are looking for sectors and stocks that have less economic sensitivities, can benefit most directly from a decline in interest rates and are more fully funded. That outlooks favours sectors such as telecoms, utilties, pipelines, technology and gold. However, when we do see an upturn in the economic cycle again, it seems clear that there should be a lot of relative upside in the small cap sector, which would also support a stronger move back into Canadian stocks which have far more economic sensitivity than their U.S. counterparts.

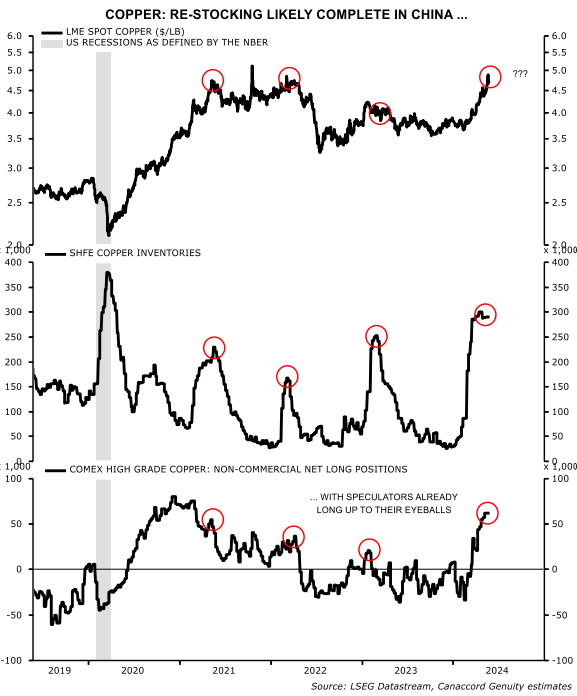

One of the biggest winning sectors so far in 2024 has been the copper stocks. We, however, have recently been reducing exposure in this group. In the medium/long term, the secular demand tailwinds for copper are well understood (EVs, electrification, data centers, etc.). This year, supply constraints and investment demand seem to have intertwined, leading to a bit of a ‘short squeeze’ which sent prices briefly above US$5 per pound, a record level. On the supply side, production disruptions at First Quantum, Rio Tinto and Anglo American have led most copper analysts to predict a deficit for both 2024 and 2025. Then, global manufacturing activity started to turn higher again just as China was busy importing copper to rebuild Shanghai (SHFE) copper inventories. It did not take long for speculators to start covering their short positions and then extending their net long, which lead to the most recent surge in copper prices. However, copper prices tend to peak at the same time as SHFE copper inventories. Furthermore, speculators are aggressively long on copper (third panel). In our view, this opens the door for a lengthy consolidation in the $4-5/lb range until physical demand comes back and push copper sustainably above $5/lb.

Bond market strategy: A good hedge against economic and stock market weakness. Given that we expect the economic data to deteriorate further over the balance of the year, we believe we have seen the high in interest rates for the next year and therefore are looking at increasing positions in the bond market in order to benefit from an expected fall in rates. However, we prefer government bonds in the mid-term maturity range as opposed to long-term bonds or corporate bonds. Our issue with corporate bonds is that investors have been “piling into” high-grade corporate bonds to avoid the negative carry of government debt. That has caused the corporate ‘spreads’ (the higher yield of corporate bonds over government bonds) to narrow to levels seen at prior economic peaks, such as 2008, 2018 and 2020. All of those periods were prior to recessions which pushed spreads back up again and caused corporate bonds to lag government bond returns, even though interest rates fell overall. We also see less upside in longer-term bonds since we expect that ongoing government deficits will mean continued large borrowing and therefore a higher ‘term premium’ on bonds in order to attract buyers. In Canada, bonds in the 10 to 30 year maturities have yields in the 3.6% area. Continued borrowing will mean ‘term premiums’ in the 1.5% range which, along with inflation expected to hit its 2% target, means interest rates should be in the 3.5% range, suggesting limited price upside. Economic weakness might push us to the lower end of that range and therefore justifies having some weight in bonds right now. However, similar U.S. bonds currently yield closer to 4.5% so we can see more upside in the U.S. treasury market than in Canada, assuming that both ultimately could fall to about 3.5%.

Overall this looks to be a stock picking environment! In the absence of unexpected macroeconomic or geopolitical events which could cause strong overall moves up or down in the stock market we believe that stock selection will be the key determinant of relative performance for at least the rest of 2024. Our criteria on stocks is that we like less economic sensitivity, leverage to declining interest rates and reasonable valuations. Some names that fit this criteria that we have been adding to lately include ‘green energy’ stocks such as Boralex Inc and Northland Power, which have massive exposure to both onshore and offshore wind and have fully financed their existing expansion plans over the next five years. Capital Power is another high-yield name that has great exposure to the massive rise in electricity demand expected as data centres continue to grow with the AI spend. In the techology sector, we used the recent weakness in software stocks to add to some positions including Telus International, Open Text and Lightspeed Commerce in Canada and PayPal and Meta in the U.S. While adding some software names on weakness, we did take some profits in our semiconductor holdings, AMD and Nvidia, after both stocks surged again last month on another strong quarter results from industry leader Nvidia. Also, in the materials sector while we did reduce our holdings in the copper stocks, we added to stock Torex Gold for both its exceptionally low valuation and its successful expansion at the Morales region in Mexico, where over 30% of the output from the new Media Luna mine will be from copper. Finally, we did add to some names in the industrial sector (CargoJet and MDA Space) which have fallen in the past few months on economic worries despite our expectations of continued strong growth for both companies in the year ahead.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.