Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

August 1, 2019

Stocks rallied again in July, lead by the U.S. technology group as investors celebrated second quarter earnings that beat expectations and looked forward to more easing from global central banks, especially the U.S. Federal Reserve. Fed Chairman Jerome Powell then did deliver on July 31st the ‘expected’ first interest rate cut since the Financial Crisis in 2008. However, he did not indicate that this was the first of more cuts, instead pointing to the Fed’s “data dependency” for future rate moves. For the month the TSX Composite in Canada was basically unchanged as further weakness in the Energy sector (down 4%) and Health Care (down 13% due to Cannabis stocks) offset slight gains in the Consumer and Information Technology sectors and a 9% gain in the gold stocks. U.S. stocks were relatively stronger due to their heavier weight of technology stocks and a slight recovery in the financial sector. Overseas markets were mostly down, particularly in Asia, with drops of almost 5% in South Korea and India.

But looking ‘under the covers’ of the optimistic conditions that have driven U.S. indices back to their old highs this year, we once again find reality falling far short of expectations. The fact that over 80% of reporting companies beat expectations is more a reflection of the fact that expectations had already been reduced significantly such that the ‘expectations bar’ was exceptionally low. The reality is that earnings shrank by about 3% year-over-year. Moreover, guidance points to more negative growth in the third quarter. The much-anticipated ‘second half recovery’ that investors were banking on early this year doesn’t seem to be taking shape! We still see earnings risk lurking in the stock market, that should at some point lead to a pullback. The list of negatives is long – the percent beating consensus on earnings and sales has fallen since the start of reporting season while cost-cutting and restructuring continue to take up a lot of air time on earnings calls. Negative pre-announcements are also rising for the third and fourth quarters and the 2020 analyst growth forecasts still seem too high.

While investors continued to celebrate an expected easing in interest rate policy by the U.S. Fed in July, the economic data continued to look rather suspect, in our view. Chinese economic numbers for the second quarter were the worst in two decades and extended an ongoing reduction in growth that has been going on for the last 15 years. The real surprise last month though was the European data, where the Purchasing Manager’s Indices for the manufacturing sector slid into the recession zone of ‘less than 45.’ The Services Indices continued to hold up well, but manufacturing has always been a better lead indicator for overall growth. That is just simple economics; manufacturing grows through business spending which is, in turn, driven by profit growth. Those expansions then translate into employment growth, rising spending and increased confidence. The fact that profits are now sinking is a much more important lead indicator for future growth than the fact that employment is at a multi-year high and consumer confidence is exceptionally strong. The latter are ‘lagging indicators of growth.

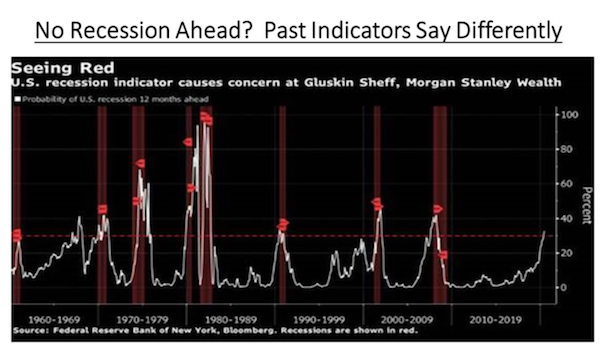

Similar economic trends are showing up in the U.S. While the ‘economy bulls’ pointed out the exceptional 4.3% growth rate in consumer spending in the second quarter GDP report, the overall number was only up 2.1%, a long, long way below the U.S. President’s claim that the U.S. economy is in the ‘best shape ever!’ The real problem in the U.S. has been the reduction in the manufacturing sector, where the PMI dropped to 50 for the first time since 2008. The bottom line is that the next recession is already emerging in various sectors of the economy. The monthly indicator shown below uses such forward indicators as the gap between yields on three-month Treasury bills and 10-year notes. The latest reading is 32.9%, a 12-year high!

We see many other economic indicators pointing to weaker economic times ahead. Morgan Stanley’s Business Conditions Index, which captures turning points in the economy, fell by 32 points last month. That drop was the largest one-month decline on record and the lowest level since December 2008, during the financial crisis. An often-stated quote from famed investor Warren Buffett is that, if he was stranded on an island and able to look at only one data set, he would choose the Weekly Rail Volumes. But that data doesn’t seem very supportive of a positive economic outlook either as volumes last week 27 fell -5.5% year-over-year. It also suggested that most end markets are contracting, with coal being especially weak.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.