Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

November 2, 2024

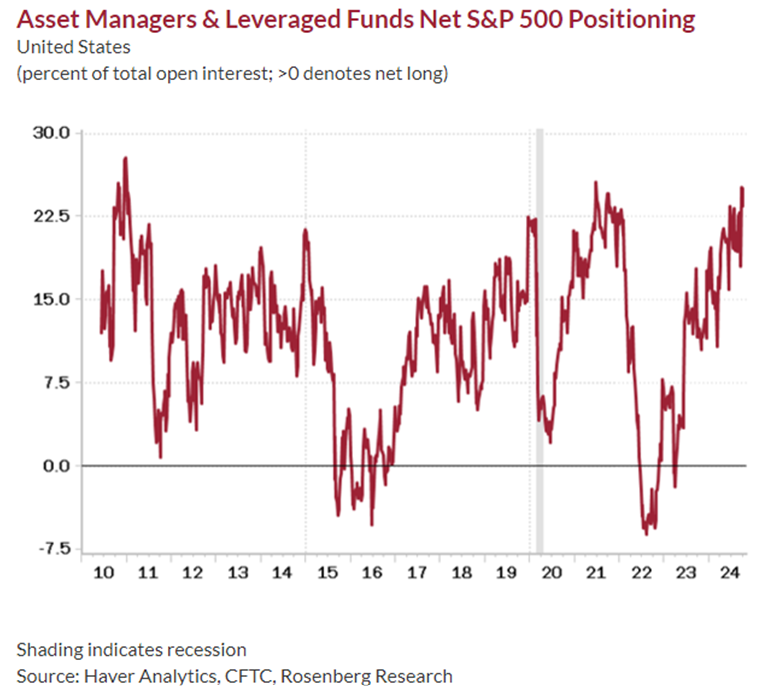

Asset managers and hedge funds have also gone ‘all-in on the S&P500’, creating a very crowded backdrop in the process. In the latest CFTC data (shown below), this group is net long just over 700,000 S&P 500 futures and options contracts on the CME — roughly 25% of total open interest, in line with historical peak readings back in 2021 (ahead of the -25% correction in 2022) and just shy of the 2010 all-time high of 27% (a -20% decline was seen during the following year). While not a timing tool in and of itself, such a one-sided backdrop combined with extreme valuations and technical readings, as well as euphoric sentiment data, continues to argue for short-term caution despite the positive momentum in the stock market. It also suggests that the longer-term risk/reward profile is looking increasingly challenged, another reason to hedge stock market allocation with a healthy weight in bonds.

The gap between stock market performance and earnings has continued to widen this year as the S&P500 has continued to make new highs even with analyst earnings revisions for 2025 having peaked and year-over-year earnings growth only in the single digit range. The result is that the equity risk premium (the excess return that investing in the stock market provides over a risk-free rate) has dropped to a mere 50 basis points versus the historical norm of around 300 basis points. Only two other times in recorded history have valuations been as excessive as today; 1929 and 1999!

Goldman Sachs is one dealer stepping away from the bullish consensus, pointing out that the recent gains are only taking away from potential future gains in the market by elevating valuations and expectations to unsustainable levels. Specifically, they say that the S&P500 will serve up a miniscule return over the next decade that falls far short of the booming gains from the last decade, citing today’s high concentration in just a few stocks and a lofty starting valuation. “The broad market index will produce an annualized nominal total return of just 3% the next 10 years”. The Goldman team is worried that these returns have been driven by just a few stocks that can only keep up their dominance for so long. “The intuition for why concentration matters for long-term returns relates to growth in addition to valuation. Our historical analyses show that it is extremely difficult for any firm to maintain high levels of sales growth and profit margins over sustained periods of time.” Along with concentration, Goldman looks at four other market variables for its model: valuation, economic fundamentals, interest rates and profitability. They conclude “the current high level of equity valuations is a key reason our 10-year forward return forecast sits at the lower end of the historical distribution.”

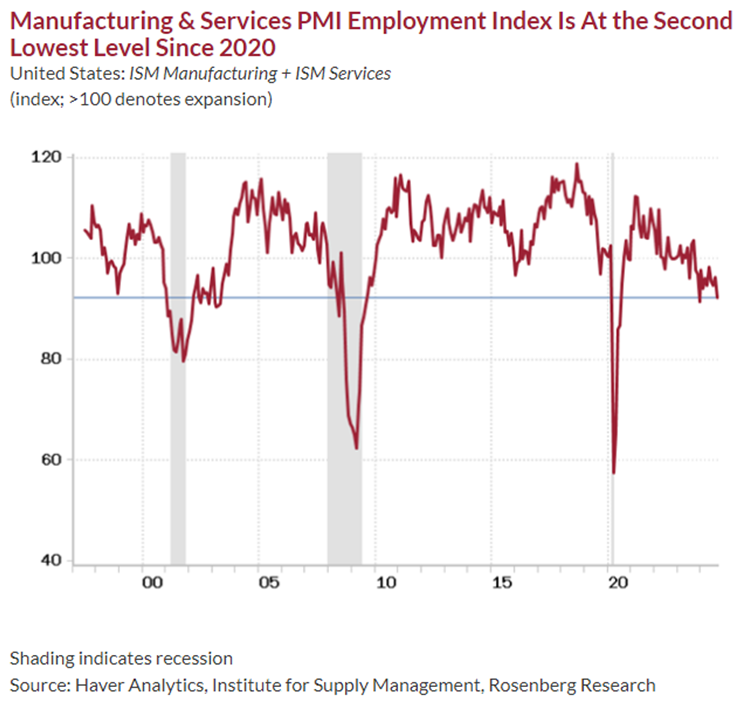

While stock markets have basically written off economic risks, particularly in the U.S., global growth news continues to come in on the weaker side. The International Monetary Fund shaved its global growth forecast for next year, citing accelerating risks from wars and trade protectionism. Meantime, the Bank of Canada stepped up the pace of interest-rate cuts and signalled that the post-pandemic era of high inflation is over. Policymakers lowered the benchmark overnight rate by 50 basis points, the most since March 2020, to 3.75%. Chinese banks also cut their lending rates after easing by the central bank at the end of September, part of a series of measures aimed at reviving economic growth and halting a housing market slump. While the U.S. has continued to be a ‘growth oasis’ in a slowing global economy, the manufacturing sector has already been in a sharp reversal, and we expect the services sector to follow that path. As shown below, the dual ISMs came in with a combined 92 employment reading in September (the average being 46, which is contractionary). This is the second lowest reading since June 2020 and at a level consistent with the 2001 recession (and subsequent shaky recovery) as well as the 2008-09 downturn.

Finally, the news on global debt levels has shown no signs of being less of a risk. Global government debt loads are set to surpass $100 trillion this year for the very first time and fast approaching 100% of global GDP. That means that global debt as whole will be at the levels we used to just associate with very troubled economies (i.e. Latin America in the 1980s, Africa in the 1990s or Greece in 2010). From an investment perspective, the case for gold from this unstable condition could scarcely be stronger. No surprise then that gold bullion prices have continued to hit one record level after another this year, touching a recent high of US$2800 per ounce from ongoing aggressive buying by central banks, particularly those in emerging markets. Are we coming to an end of the U.S. dollar as the global reserve currency? It certainly is not without its risks. Gold stocks have continued to lag the move in gold bullion and remain a very attractive investment in our view.

It might feel like we are ignoring ‘the elephant in the room’ by not talking much here about the upcoming U.S. elections. While the polls show a tight race we have to admit that we are not even sure what the market reactions would be if we knew the results in advance! Both candidates have advocated fairly aggressive spending/ tax cut program that would most likely result in higher longer-term interest rates as borrowing to fund those growing deficits rises. Much of that positioning has already been seen in the past month, particularly as the ‘betting pools’ focused more on a Republican win and drove up the values of some expected beneficiaries under that scenario, including crypto currencies, gold, energy infrastucture and financials, where less regulation might be expected. However, election impacts are generally short-lived. Outside of the 2000 election, where the stock market sold off over 7% while the (legally) disputed results were subject to a recount and the very volatile overnight market action following the 2016 election results, we expect investors will quickly shift their focus back to the upcoming Federal Reserve meeting, the employment numbers on November 8th and Nvidia earnings the following week. In other words, we could (hopefully and thankfully) stop talking about U.S. politics for a while!

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.