Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

May 2, 2022

The financial, consumer discretionary, industrial and energy sectors are trading at discounts to long term valuations and acting as if we had already entered a recession. That level of pessimism and low expectations present the best buying opportunities. Our favourite sectors are the ones that have been hit the hardest during the current sell-off, especially the consumer discretionary. Autos and parts such as GM and Magna top this list as well as the banks (Bank of America, Morgan Stanley, CIBC) while, in technology, the semi-conductor names have been crushed and still have strong fundamentals (AMD, Qualcomm and the semi-ETF; SMH). Energy stocks remain cheap as they still don’t reflect current prices (Crescent Point, Suncor, Cenovus, Arc) and gold stocks are acting very well technically despite the new headwinds of rising real interest rates and a stronger U.S. dollar. There we like B2Gold, Agnico and Torex.

Two members of the FAANG group have been ‘defanged’. In the five months since the Nasdaq’s peak late last year, Netflix and Facebook (now Meta Platforms) have gotten crushed, giving up most of the gains they’d accumulated over the prior half decade. Netflix is down over 70% since the Nasdaq peak last November, while Meta was down more than 50% from its high prior to a bounce in the past few days on an earnings report that was not ‘as bad as feared’. Even Amazon is down 33% from its November high after dropping sharply this week on earnings that failed to meet expectations, as higher spending and costs have hurt cash flow margins. In the recent past, all of these companies appeared to have unstoppable growth and impenetrable moats. Netflix was so embedded in American households with must-see original content that the company could periodically raise its monthly subscription cost and not miss a beat. And Facebook, with its billions of users and dominant ad-targeting engine, was accumulating envious amounts of online ad revenue. Those stories have flipped relatively quickly — with investors reassessing the companies’ prospects in the face of increased competition and a deteriorating macroeconomic environment. Bottom line; these stocks are still ‘over-owned in most institutional and retail accounts as well as most index funds. Unwinding those overweight positions will take some time and they will not be going back to those previous highs anytime soon.

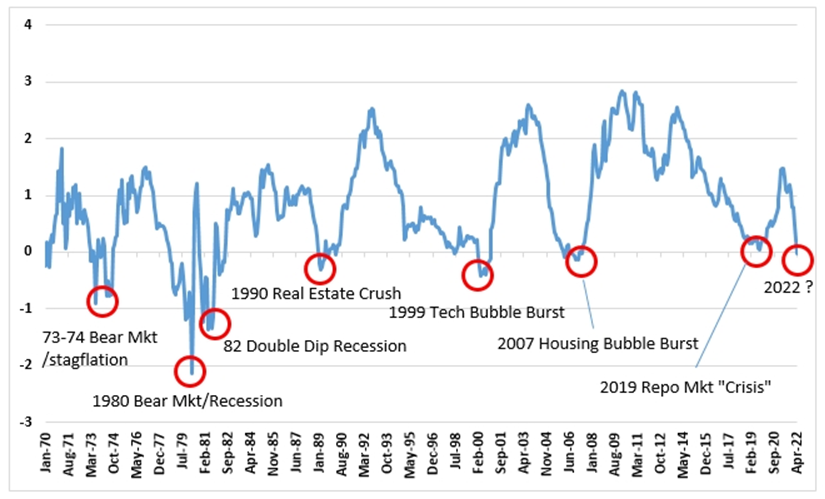

While we believe that stocks have factored a lot of bad news in already and that we don’t see a recession on the immediate horizon, there are clearly some more bearish signals coming from other corners that are feeding the negative narrative. One very worrying sign for those looking at the economic risks for the stock market is the recent Inversion of the ‘Yield Curve’. While many versions of this measure exist, the most widely-followed metric is the difference between the yield on 2-year Treasury Bills versus 10-year bills. Typically, longer-term rates have the higher yields but, when central banks are tightening policy and raising short term rates, it often leads to a period when the shorter-term rates rise above the long-term rates. This ‘yield curve inversion’ has often been pointed to as a harbinger of weaker economic conditions or even a recession. The chart below shows the times that this measure has once again turned negative. While not an exact timing tool, investors need to pay attention to the warnings from the yield curve since it has a very good track record or predicting recessions and bear markets. In the U.S. the Fed has been in rate hiking cycles 13 times since 1955, with 10 of those 13 episodes ending in recessions (hard landing). The bullish case is that central banks can raise rates and reduce inflation without driving the economy into a recession, also known as the ‘soft landing.’ Last time they did this was in the mid-1990s.

The history of this indicator suggests that recession risk is clearly present. Since consumers and businesses are still relatively well funded and interest rates are still at historically low levels, we would hope that central banks could achieve a ‘soft landing’, but as we’ve heard many times over the last 40 years of managing money, ‘hope is not a sound investment strategy.’ Some continued caution in the stock market still seems like the logical strategy for now. We are keeping stock weights close to neutral with a ‘value bias’, are still underweight on bonds and overweight on cash.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.