Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

May 2, 2022

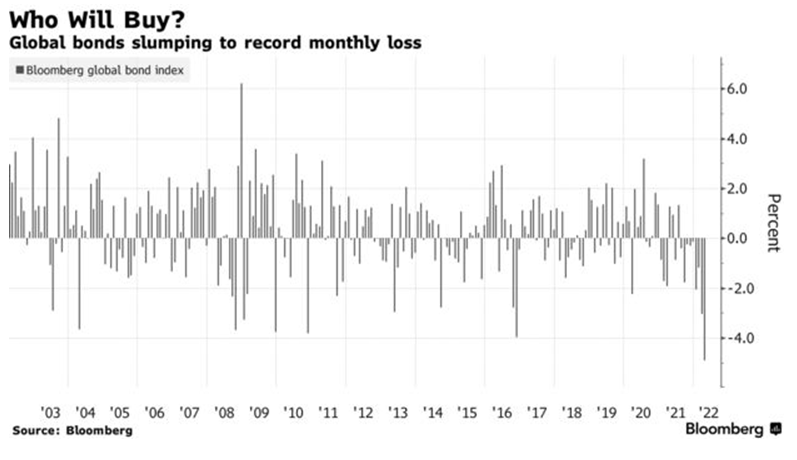

There was ‘no place to hide’ for financial markets in April as stocks, bonds, preferred shares, commodities and crypto currencies all succumbed to the most aggressive selling pressure seen since the early days of the pandemic. In the U.S., the S&P500 had its worst month since the onset of Covid over two years ago, as the index broke down below the lows seen earlier this year. The ‘technology heavy’ Nasdaq Index took the biggest hit, registering its worst month since the lows of the Financial Crisis in 2008. Canadian stocks were not immune from the losses, although the continued strength in the Energy sector offset some of the losses in the index. Meanwhile, bonds continued to sink despite coming off their worst quarter in three decades. Global bonds had their worst month on record as investors braced for a flurry of rate hikes, including the most aggressive U.S. tightening since May 2000. The Bloomberg Global-Aggregate Bond Index lost 4.9% in April, its biggest monthly drop since its inception in 1990.

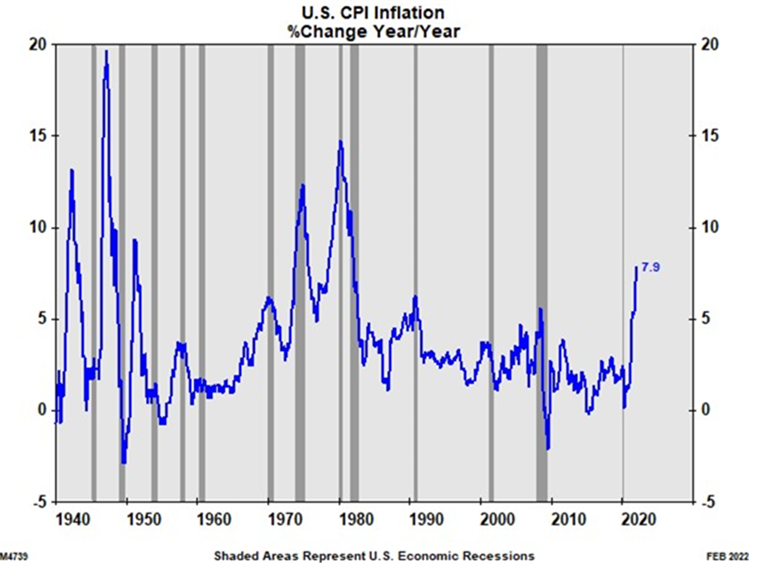

The source of the selling was apparent as there was no shortage of worries for investors. Stock indices are still trading near record valuations, particularly in the high growth sectors, just as central banks are removing the stimulus of ‘free money’ that has provided the fuel for the bull market in financial assets over the past decade, thereby challenging the logic of continued high valuations. Moreover, inflation is running at 40-year highs and investors fear that the central bank actions to control runaway prices could force the global economy into a recession. This is starting to show itself in the first quarter earnings reports and guidance for the balance of the year, thus putting in doubt many of the current earnings estimates. Also, a resurgence of Covid in China, which is attempting to maintain a zero tolerance on new cases rather than focusing on vaccinating their population with a proven vaccine, has lead to a near shutdown of that economy and further problems for both the global supply chain as well as the demand for core consumer goods such as cell phones. On top of all that, the war in Ukraine is worsening a global shortage of raw materials, particularly in the energy and agricultural sectors, which is adding to the global inflation fears.

Serious Market risks still exist from central bank tightening. While all investors know that central banks are starting to raise rates, the debate is about how many increases are ultimately in store, how quickly that will happen and are the central bankers really as ‘hawkish’ on rates as they recently claim to be? The answer goes to their ability to use these rates to bring inflation down from 40-year highs. It’s important to recognize that this is not a ‘1970s style’ inflation, driven by rapidly rising wages and robust growth. This is a ‘supply shortage’ inflation due both to the breakdown of global supply chains from the pandemic and now the additional pressure on commodity shortages from the Ukranian conflict. Raising interest rates will do nothing to fix those supply-side issues issues. If supply can’t be increased, then the policy has to be to reduce aggregate demand for goods and services. Most of the extra demand for spending is coming from consumers who have higher savings (from less travel etc. during lockdowns) and are feeling wealthy due to surging stock markets and rising home prices over the last two years. This ‘free money effectively created a bull market in financial assets that central banks need to wind down in order to reduce aggregate demand and relieve the inflationary pressures; at least until the supply shortages can start to be addressed. All of this suggests that one of the primary targets of these rate increase is the stock market and that investors can no longer count on the ‘Fed put’ wherein central bankers would be expected to rescue any stock sell-off with more interest rate relief. The training wheels have come off for stock market investors!

However, despite all of these warnings, we don’t think investors should be panicking. While risks remain, investors have been positioning for this weakness with high cash levels in institutional accounts and investor sentiment among private investors reflecting extreme pessimism. Investors have been pulling money out of the market at an accelerated rate over the past six months. Investor sentiment, in the process, has been driven near all-time lows. The most recent weekly AAII (American Association of Individual Investors) in stock prices was the most bearish it has been in 35 years. This all suggests we are close to at least a ‘tradeable low’ in stocks. One key metric we have been watching for a signal of a bottom is the ‘last hour of trading.’ For the last few months, we have seen sell-offs into the close and even the ‘up days’ seem to lose steam in the last hour. This shows that investors had still been over-invested in stocks and were ‘selling the blip’ instead of ‘buying the dip’ in stocks as they had been doing for much of the 2020-21 bull market. Once we start to see those late-day selling pressures subside, we expect the stock market could start to recover.

Moreover, although economic activity is clearly slowing down, we don’t see a high risk of recession in the near term. Consumer balance sheets are strong, job openings remain plentiful and the demand for many goods such as cars are still in backlog, which suggests production needs to continue to rise. Not the ingredients for a recession! We are also seeing a resurgence in spending on services as global economies re-open further. First quarter earnings reports are starting to come in and they look to be exceeding the depressed expectations. Money centre banks and ‘re-opening’ businesses are doing well and we haven’t seen any negative surprises from the big tech companies on their reports this week. While ad spending has been hurt a bit, the supply chain issues and war in Ukraine have not impacted demand for iPhones or the migration of business to Microsoft, Google or Amazon clouds. Semi-conductor demand is still in backlog and needs to grow. We also believe that earnings will continue to grow despite some economic weakness. Businesses retain pricing power and strong balance sheets. Since we don’t see the risk of a near-term recession as high then we see the current stocks pullback as limited and that is another reason to add to stocks in this sell-off, since no bear market has occurred without a subsequent recession!

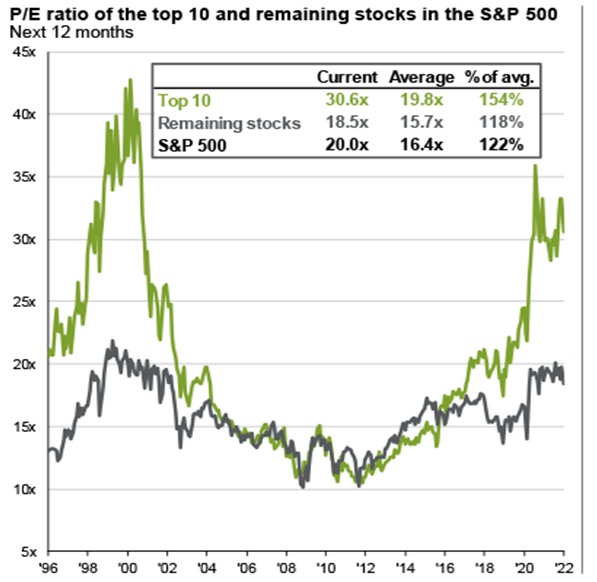

While stock valuations are extended in the largest S&P500 companies, the valuations of the rest of the index are actually right in line with historical averages. The chart below shows the current valuation split of the main U.S. stock index. The top 10 stocks in this index (which represent over 25% of the index weight) are trading at over 30 times forward earnings, a 54% premium to the long-term average. The remaining 490 stocks in the index trade at 18.5 times forward earnings, just 18% above the long-term average. Clearly investors have been viewing Apple, Microsoft, Amazon and the other tech giants as almost the equivalent of what bonds have been in prior weak market conditions. The action of some of the largest stocks in the index over the past week shows that this narrative may be changing and the megacaps are suddenly not the ‘safe haven’ that they seemed to be! That happened when we were coming out of the tech bubble in 2000, as the indices fell but most of the stocks outside of those largest tech names actually held their value or even increased.

Finally, unlike the 1970s, wage pressures are not expected to be persistent. Retirees are actually coming back to the workforce and the re-opening is bringing many workers back to offices and retail businesses. The ‘participation rate’ in recent employment numbers is rising again. This should alleviate the worker shortages to some degree and remove wage pressure as an ongoing source of inflation. We also expect that the ‘supply crunch’ on commodities will start to ease as alternative supplies are sourced and demand is reduced due to tighter financial conditions and less demand from China. All this suggests we are seeing peak inflation now and may mitigate the need for central banks to be as aggressive as they appear now on interest rates.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.