Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

February 26, 2019

Deteriorating economic data has also not been limited to the U.S. Global auto sales fell by 9% year over year in January owing to a steep 18% y/y drop in the Chinese market. German growth was negative in the 3rd quarter of 2018 and barely positive in the 4th (thereby avoiding been in a technical recession) and consumer sentiment continued to decline in 2019 along with most other indicators. Further to that, the European Commission (EC) published its latest growth forecasts and said the pace of growth is expected to moderate further and the outlook is subject to large uncertainty. It forecast Eurozone growth of 1.3% versus its prior forecast of 1.7%. It cut German 2019 GDP from 1.8% to 1.1%, France to 1.3% from 1.6% and Italy to 0.2% from prior 1.2%. It highlighted that its projections are subject to downside risk due to a high level of uncertainty. Europe’s economy faces a daunting combination of weaker demand for its exports from China and elsewhere, the prospect of a messy divorce with the U.K. and political problems closer to home. The Bank of England (BOE) sounded a similar warning on the global economy, saying it expected to see a “sharper and more persistent” slowdown. Both the EC and the BOE identified a deceleration in China while it navigates a trade dispute with the U.S. as a key headwind, a threat that was underlined by figures for December that recorded a fourth straight month of declining factory output in Germany, Europe’s exporting powerhouse. Italy is already in recession, defined as two straight quarters of declining economic output. Germany had almost joined them in that assessment but fourth quarter results showed 0.1% growth, allowing it to narrowly avoided a second quarter of contraction as 2018. But data released since then, such as the figures for industrial output, ISM surveys and retail sales have raised doubts about that assessment.

Meanwhile, we are back to having US$11-trillion of bonds around the world trading with a negative yield, fully a decade after the end of the financial crisis. The World Trade Organization’s (WTO) trade outlook indicator was the weakest since March, 2010, pointing to slower growth in the current quarter. Said the WTO: “The simultaneous decline of several trade-related indicators should put policy makers on guard for a sharper slowdown should the current trade tensions remain unresolved.” Perhaps the most pronounced change has been seen in Europe, which is now being flagged as ‘the most likely region to first sink into recession’. Between budget wrangling in Italy, the Yellow Vest protests in France, Brexit, more political uncertainty in Spain, and Germany’s auto-sector difficulties, all major EU economies are facing challenges.

Another surprise in the recent stock recovery is the degree to which poor corporate earnings guidance is being accepted by investors, believing instead that they will see a recovery in the back half of 2019. Nowhere was this more apparent than in the very ‘economically-sensitive’ semi-conductor industry. Many quarterly conference calls recently have included dour outlooks for the next quarter combined with a reiteration that the company would still hit its full-year 2019 targets. But most times they refer to the results this year as being “back end loaded,” putting out a belief that the current economic slowdown is only ‘transitory.’

We believe that we will continue to see dismal economic numbers and earnings downgrades on a regular basis as we are entering into a period of economic decline. Just looking at a few headlines this morning as I finalize this letter highlights some more negative news which we think is indicative of what we will see going forward:

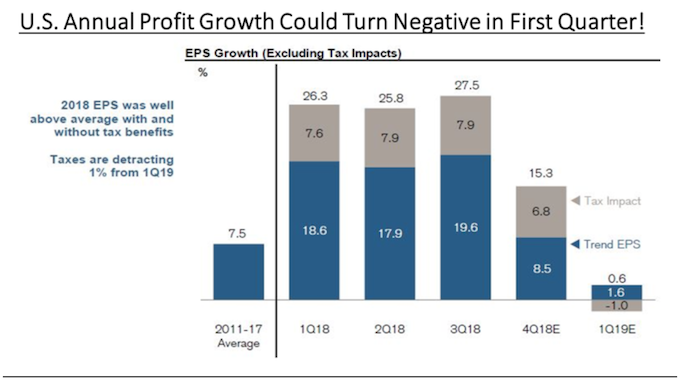

The net results of these downgrades should be reflected in first quarter 2019 earnings when they begin to be released in another two months. Earnings growth will most likely turn negative on a year-over-year basis, a significant comedown from the approximately 25% year-over-year growth we saw in the first 3 quarters of 2018, when much stronger global economic growth was being augmented by the full impact of the U.S. tax cuts.

When I add up the disappointments in global economic data and expected reductions in earnings outlooks, it’s hard not to see the glass as ‘half empty!’ when it comes to the outlook for stocks in 2019. We have been surprised by the strength of the current recovery and don’t deny that a deal on U.S/China trade and a much more dovish backdrop on interest rates from central banks are a positive for stocks. But financial conditions have already tightened due to the interest rate increases already enacted and economic growth has peaked for this cycle, in our view. While there might be more buying opportunities for stocks similar to that created in the December sell-off, we don’t see any good reason to have a significant overall weight in stocks at this time. We’re staying underweight U.S. stocks but have added some resource exposure in Canada, where we have watched a mass exodus of capital for much of the past four years. We expect a lower U.S. dollar to provide some strength to the commodity group and are seeing some better technical action in energy, base metals and gold stocks. We remain cautious on financials, industrials and tech.

But just so we don’t finish a very sombre commentary on a totall bearish note, the is some good news for beleguered Canadian investors! While the China trade war has clobbered U.S. farmers, it’s been a boon north of border. Canada’s shipments of soybeans to China, the world’s largest buyer, surged to a record 1.23 million metric tons last month, more than four times the amount a year earlier, and up from just over 800,000 tons in December. Imports from the U.S. collapsed to 136,000 tons from 5.8 million tons in January last year. China’s importers, usually processors that crush soybeans into cooking oil and animal feed, have shifted purchases to Canada and Brazil to avoid the 25% retaliatory tariffs the country slapped on U.S. farm products last year as the trade conflict intensified. Canada was the biggest shipper of soybeans to China in January after Brazil, which supplied 4.93 million tons. The spat between the U.S. and China has roiled global trade flows, with the usual routes disrupted as the Asian nation sought supplies from other origins. Still, China has recently been back in the market for U.S. soybeans as a goodwill gesture in talks to resolve the trade dispute.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.