Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

June 30, 2021

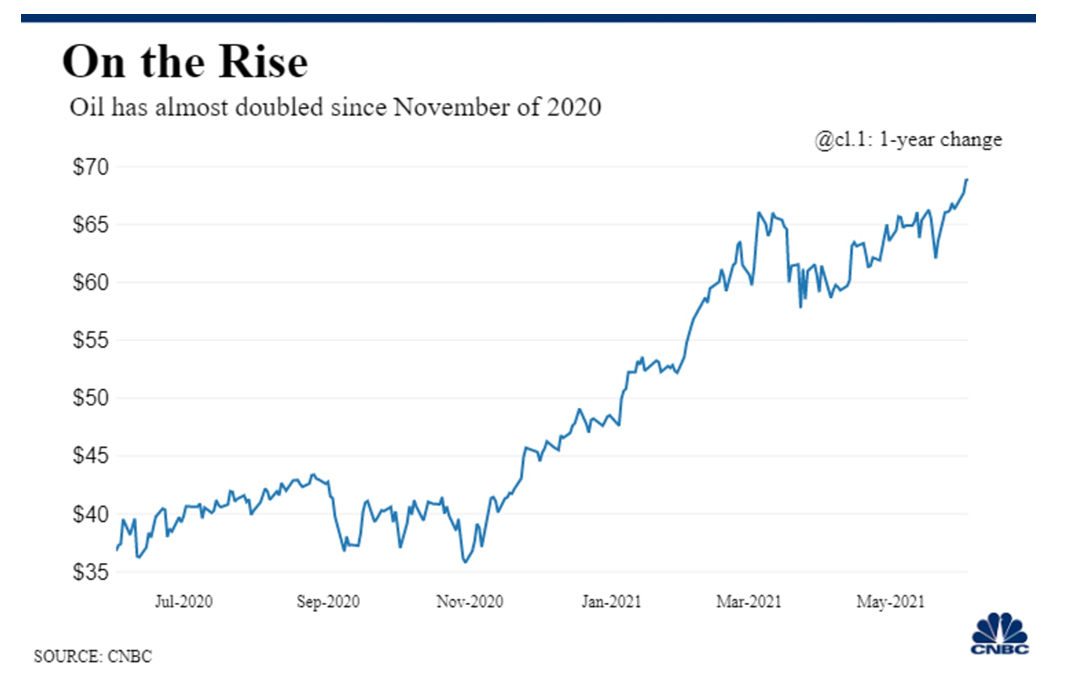

That does lead us to highlight the Energy sector, which we still favour even though it has already risen sharply this year. Oil prices dropped sharply and even went negative, at the beginning of the pandemic, which lead to a sharp drop in U.S. production after five years of growth to record levels. The U.S. was the world’s largest oil producer prior to the Covid-19 pandemic, as independents and majors drove shale production to higher and higher levels. But as oil prices have recovered all of their losses, U.S. production has been mired in the range of 11 million bpd. OPEC+ is expected to start slowly putting back some of the production that they removed in the wake of the pandemic when they meet next month. That will probably define the shorter-term moves in the sector. But the overall picture is that the market is currently experiencing a surge in demand but production is not running at the same pace, such that the world is currently producing less oil than is being consumed.

Most energy stocks are still trading at levels below where they were three years ago, when energy prices were last near this level. Moreover, they have shifted their focus to profitable cash generation and shareholder returns as opposed to simple growth. This makes the energy stocks, in our view, very similar to the tobacco stocks of the 1980s. For those with long memories, you will recall that those stocks generated good returns and high yields for years despite the lack of overall industry growth.

While it’s one thing to talk about overall strategy, investors are always more interested in specific names. Currently, we like the auto manufacturers and parts companies for their exposure to the shift to growing electric vehicle (EV) production, the low valuations for stocks in these sectors and the strong demand for autos during the pandemic, which has driven inventories to multi-year lows and lead to a surge in used car prices. Parts maker Martinrea International (MRE) is our top choice in the sector and has multiple attractions, as is has an exceptionally low valuation, a strong balance sheet and positive free cash flow. It has a focus on the ‘lightweighting’ of vehicles through greater use of aluminum parts, a key factor in meeting the growing demand for electric vehicles without the associated valuation risks. MRE has the added benefit of an investment in VoltaXplore, a venture to produce battery components using Graphene, which gives MRE additional EV growth exposure. The heavily discounted valuation provides an opportunity much like it did at market lows in 2009 and 2016. Insiders at the company have also been active buyers of the stock recently, another endorsement of the attractive valuation and growth.

Another sector that stands out for us is the space sector. The ‘race to space’ has garnered more headlines in the past years as three of the world’s wealthiest billionaires, Jeff Bezos, Elon Musk and (Sir) Richard Branson, have engaged in high profile projects to get into space. The attraction is not only commercial space travel but, more importantly in our view, the launching of multiple satellite constellations to provide internet services to global customers as well as provide high quality digital images from space for a variety of uses, from urban planning to agriculture to military intelligence. Maxar Technologies has been our top choice in this group for its 2018 purchase of Digital Globe, which married its own strength as a manufacturer of low orbit satellites with the software capabilities to assimilate and interpret this data. Another Canadian aerospace company, MDA Ltd. returned to the public market this year. In its prior structure, the former MacDonald Dettwiler was sold by Maxar to private equity in 2019 and brought back to the public market this year with a stronger growth profile and better industry conditions. A global leader in orbital robotics and satellite infrastructure/subsystems, it is generating positive free cash flow, has a strong balance sheet and trades at an attractive valuation. Opportunity exists in the low-Earth orbit satellite constellations driven by the demand for internet communications as governments act to improve internet access. NASA also expects its budget for commercial low earth orbit operations to grow from $17 million in 2021 to $184 million in 2023. Spending by NASA becomes revenue for commercial space companies. MDA projects annual revenue growth of over 25% over the next five years as several key ‘flagship programs’ roll out.

Another sector we favour is semi-conductors, and our favourite way to participate in a lower risk investment is through the VanEck Vectors Semiconductor ETF, which encompasses the largest global players in the chip industry and includes 5%+ positions in Taiwan Semi, Intel, LAM, Texas Instruments, Applied Materials, Broadcom and Qualcomm. We view the semis as the ‘industrial sector’ of the next age of growth and should be a part of any growth portfolio. We have seen extraordinary demand for semiconductors over the past year due to the effects of the pandemic as the work-from-home era has spurred sales of laptops, cell phones, appliances, autos and other personal use items, all of which come with customized chips. The excess demand and supply chain issues lead to a shortage which has most negatively impacted auto sales, but these shortages are easing. The growth of cloud servers and 5G communications will further spur growth in this industry. Valuations are high relative to the past, but the growth trajectory also looks more secure.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.