Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

December 27, 2019

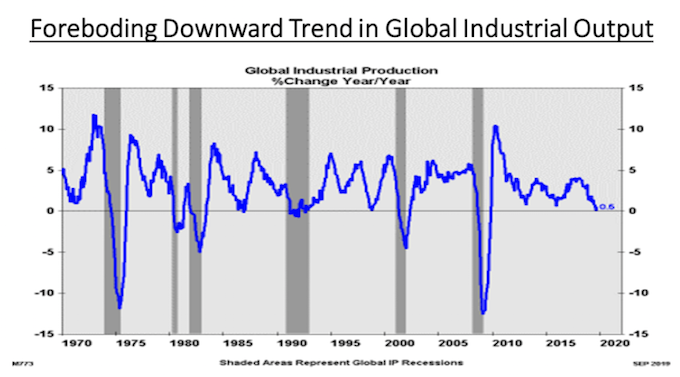

Elsewhere, Germany’s sprawling industrial sector is suffering its steepest downturn for a decade, underlining how the engine of the eurozone’s biggest economy is sputtering. Industrial output, which includes Germany’s dominant factory sector, dropped 5.3% in October. The figures suggest that the German industrial slowdown is likely to weigh on overall eurozone growth in the fourth quarter. Combined with data published this week showing industrial orders fell sharply in October, and with most manufacturers expecting a further shrinkage in November, the figures suggest that the two-year downturn in German manufacturing is nowhere near close to ending. Far from bottoming out, Germany’s industrial recession may be getting worse. The latest data support the view that a recession is still more likely than not in the coming quarters.”

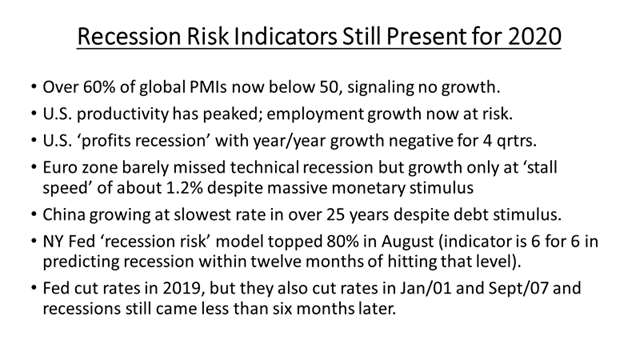

While we see no shortage of risks going into New Year that could de-rail the ten-year bull market in stocks, the top risks we shouldn’t ignore are some of the warning signs we are getting from the credit markets. It is well known that government debts across the globe have risen to record levels in the past decade, lead by China and the world’s largest debtor, the U.S. However, corporate debt has also swelled to record levels as companies have taken advantage of record low interest rates to load up on debt, much of which has been funneled back into stock buybacks which have buoyed the bull market. But slowing economic growth and declining earnings are under-cutting corporate strength, leading to a wave of downgrades which has pushed over 50% of U.S. corporate debt down into the BBB category (only one ‘notch’ above ‘junk rating’). This is far in excess of the prior peak of about 47% back in 2005, just before the fallout from the housing crisis and collapse in corporate debt markets.

Record low interest rates have kept the servicing of this debt more manageable, one more reason why we continue to see ‘easy money’ conditions from central bankers. Markets would be totally unprepared for any significant rise in interest rates.

But Stock Markets Do Eventually become rational! With record low interest rates and slower economic growth over the last few years we have witnessed what we like to refer to as the ‘Amazonification’ of stock markets, meaning that investors have become accustomed to the idea that high growth companies do not need to generate profits or have a business plan that ultimately generates positive cash flow as long as they have strong revenue growth. Amazon has been the groundbreaker in this group as they have shown consistent revenue growth over 25% and watched their stock soar, sending their CEO, Jeff Bezos, near the top of the list of the world’s wealthiest individuals. This occurred despite not showing any regular profitability and continuing to generate negative free cash flow. That entire fallacy of ‘growth without profitability’ got destroyed in 2019 with the sub-par performance of many ‘unicorn IPOs’ such as Uber, and Lyft, weakness in Netflix and the failed offering of WeWorks. WeWork’s failure to even make it to an IPO became the poster child for money-losing businesses and sky-high valuations not always translating to public markets. Uber and Lyft — among the biggest three listings this year — have been criticized for lack of a clear path to profitability. Companies such as Airbnb and DoorDash are looking to tap public markets in 2020 and will likely be held to higher standards when it comes to profitability However, the cannabis sector in Canada provided the clearest example of the failure of these models as the excessively overvalued stocks in that sector dropped by over 70% from their early year peaks. These companies committed the ‘cardinal sin’ for ‘concept growth’ stocks when the actual revenues both missed growth expectations and actually saw some decreases despite the hype around legalization in Canada and potential further medical use in the U.S. Stock investors do end up acting rationally, but it often takes a long time. Momentum investors can do well in the early stages but fundamentals do actually matter in the end!

Given the short-term positive momentum in stocks but our cautious economic outlook and worries about stock market risks, we have to maintain a much more ‘balanced’ strategy in our Hedge Fund to try to achieve positive returns. While we have a net short position in stocks overall, we also have significant long positions in sectors where we see exceptional value but low stock market risk, such as energy and basic materials. Within the technology sector we have tended to hold long positions in core ‘GARP’ (Growth at a Reasonable Value) names such as Alphabet, Facebook, Open Text and Microsoft against short positions in the technology indices (QQQs and semi-conductor ETFs) as well as individual stocks where we see valuation risk, such as Shopify and Constellation Software. We have adopted the same strategy in the ‘video streaming’ sector (long Disney versus short Netflix) and the autos (long parts suppliers trading at single digit multiples such as Martinrea and Magna versus short position in Tesla). To further protect against stock market downside, we have a long position in the U.S. Treasury Bond ETF (TLT) as well as proxies for any rises in stock market volatility as measured by the VIX.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.