Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

May 24, 2018

In May we saw stocks rally off the February support levels for the third time and then break up through some key resistance levels. This occurred as strong first quarter earnings report and a resumption of stock buybacks buoyed the stock market averages despite some weaker economic numbers in Europe, Japan and the emerging markets and continued geo-political issues and rising tensions concerning global trade.

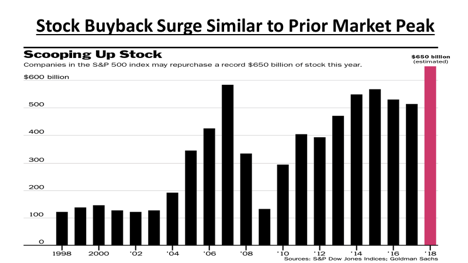

Bullish investors were initially frustrated as earnings which soared past expectations generated little enthusiasm. In some cases, it even lead to market weakness as exemplified by Caterpillar, which reported earnings well ahead of expectations and a subsequent increase in earnings and revenue guidance for the balance of 2018. But an off-handed comment by the CFO during their conference call, where he said that the first quarter might represent ‘the high-water mark for the year’, lead to a sharp reversal in those gains and turned then into losses. Also absent during the reporting season was the huge buying impact from ‘stock buybacks.’ Most corporations had been in a ‘quiet period’ before and during their respective reporting periods and were therefore not allowed to be active in the market. But, once the earnings were reported, they were then able to go back into the market as buyers and this wave of buying increased as the flurry of earnings releases died down. These companies were also armed with the proceeds from the recent tax cuts and the repatriation of some overseas funds. While the goal of the tax cut was to use the money to build capacity and expand in the U.S. and therefore create more jobs to sustain growth, the funds have been primarily funnelled back to shareholders in the form of increased dividends and share buybacks. The numbers for the first quarter currently show about US$178 million in buybacks, which equates to an annual rate of over US$700 million! As a point of interest, that’s the highest level since the fourth quarter of 2007, six months before the market peak!

To show how these buybacks are impacting individual companies, though, we need to look no further than the biggest stock in the S&P500 Index. Apple’s stock recovery and move to a new high during the past month has more to do with their announced plans to return $100 billion to shareholders as anything fundamental in their first quarter earnings report. Unfortunately, we always tend to see this type of extreme buyback activity near the end of the economic (and stock market) cycle. The chart below shows how the S&P500 companies are on track to spend over US$650 billion in stock buybacks in 2018. That would be the highest annual total since 2007, the year before the financial crisis and shows corporations, once again, making decisions based on short-term stock moves rather than the longer-term growth.

Having pointed out that most of the excess profits have been directed towards dividends and buybacks, we have to acknowledge that U.S. companies are directing some of those profits to growth initiatives. The data shows corporations are ramping up spending on their businesses at the fastest pace in years, a long-awaited development following years of tepid growth. Spending on factories, equipment and other capital expenditures by companies in the S&P500 is expected to have risen 24% in the first quarter to $166 billion, on track for the most ever spent in the first quarter of a year, according to Credit Suisse data going back to 1995. The pace of growth is expected to be the fastest since 2011. While these capital expenditures are good for long-term corporate profits and the broader economy, history suggests it could also pressure share prices. But data shows shares of companies with large and growing capex tend to underperform the broader market—which could weigh on returns just as the stock market has become more volatile. The reasons for the somewhat lackluster market reaction to the strong earnings season are well-documented: Fears that this may well be the peak, along with concerns that rising inflation will prompt an even stronger interest rate response from the Fed continue to be the offset to the strong numbers. Trade worries may have been more subdued in the past month, particularly with China, but they are a long way from settled.

Stocks have risen in the past year as global growth and corporate earnings have been strong while both inflation and interest rates remained historically low. But, at the margin, these ‘stock tailwinds’ are stating to abate. The bottom line is that the global economy is beginning to cool off. Japan’s growth was negative in the first quarter as consumer spending and capital outlays were down. European growth has slowed down to a 1.25% rate this year versus over 2% in 2017. Rising U.S. interest rates and a stronger dollar will put downward pressure on emerging economies. In the U.S., retail sales have stalled as two key sectors, housing and autos, appear to have peaked for this cycle. Also, recent economic releases show a slowdown in income growth with price increases outstripping nominal growth. Since late last year, consumer spending growth has been easing, as has personal income growth. That points to a fresh softening in a big part of the U.S. economy. Spending is outpacing income growth. That puts a lot of pressure on consumers, especially as interest rates continue to rise. The net result is that retail sales have been lower in 4 of the past 5 months. More importantly, gasoline prices have risen above the critical US$3/gallon level while mortgage rates have also been on the rise.

Rising gasoline prices are worth paying attention to since four of the past five recessions were preceded by a sharp increase in the price of oil. Since last summer, the oil price has soared by about 50% and more increases could be coming as supply constraints occur. Additional sanctions on Iran imposed by the Trump administration will limit that country’s ability to supply world markets, while the deteriorating situation in Venezuela could mean further cuts in its production.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.