Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

May 1, 2018

Debt growth has not been confined to government either as U.S. corporate debt has climbed to record levels and consumers also remain highly indebted. JPMorgan Chase CEO Jamie Dimon warned in his annual letter to shareholders that “we have to deal with the possibility that at one point the Fed and other central banks may have to take more drastic action than they currently anticipate,” and rates “may go higher and faster than people expect.” Higher rates are already having an effect. Rising U.S. household debt is paced by credit-card delinquencies, and Chapter 11 bankruptcies grew 64% in March from a year ago, says the American Bankruptcy Institute. We are seeing the telltale signs of the end of the credit cycle. The painful process of refinancing debt into the face of rising interest rates isn’t going to be compatible with many business models that have relied on a never-ending flow of cheap debt and virtually nonexistent interest expense. U.S. corporate debt stood at $6.2 trillion midway through last month, versus $2.5 trillion in December 2008. Much of that was used to fund dividends, stock buybacks, mergers, and capital expenditures. Borrowing money to buy stocks by both individuals (margin debt) and corporations (stock buybacks) has been a hallmark of the current bull market. The end of that trend is just another headwind for the stock market going forward.

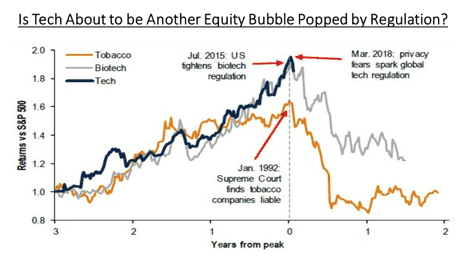

Finally, we continue to have concerns about the social media stocks despite the strong recent earnings reports. We sold our position in Facebook (FB) at US$180+ and then went short that stock in our Hedge Fund in addition to a short position in Twitter (TWTR). We think that the recent concerns about data privacy will slow down or even reverse the growth rate of users and their level of engagement with these platforms. We also think that the companies will have to spend much more money to improve the data protection as evidence by Facebook’s announcement that they will be adding 20,000 positions in areas of data privacy. Good for the national employment numbers but probably not good for Facebook profit margins going forward.

Washington’s increased scrutiny of technology giants could spell trouble for their stocks, if history is any guide. Technology is the least regulated industry sector, with just 27,000 regulations versus 215,000 for manufacturing and 128,000 for the financial sector, according to Bank of America. Tobacco (1992), financial (2010), biotech (2015) industries illustrate how waves of regulation can lead to investment underperformance.

How does all of this impact our current investment strategy? While we recognize that strong earnings growth and a recent reduction in excess stock valuation could set up the market for a re-test of the January highs, we continue to see the headwinds of slower global growth, rising interest rates and a potential peak in earnings growth leading to a peak in stock prices that we may have already seen. Within our managed portfolios we have increased our exposure to shorter-term bonds as a hedge against potentially slower economic growth and overall more attractive yields than seen over the past few years. We have taken some profits in preferred shares after a very strong two-year run in that group. We still have a slight overweight in preferred shares, though, due to the very attractive gross dividend yields. Stock weights remain below average levels as we have recently reduced positions in U.S financial and technology stocks as well as some Canadian energy stocks, which had strong gains in the March-April period. The recent gains in the U.S. dollar also prompted us to reduce gold stock weights for now as gold prices have failed on three occasions to break through the critical US$1350 range. Cash levels in all our portfolios have risen as a consequence but, with the increased market volatility seen over the past three months, extra trading liquidity in investment portfolios could prove to be a very good option as market conditions present buying opportunities in sectors with strong long-term growth.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.