Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

October 28, 2021

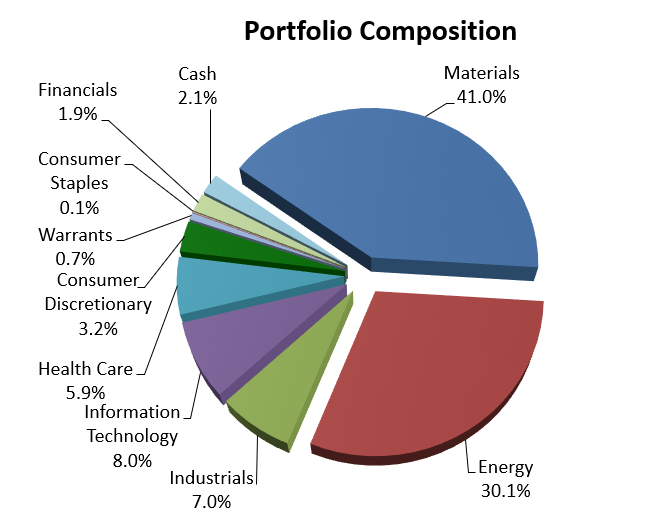

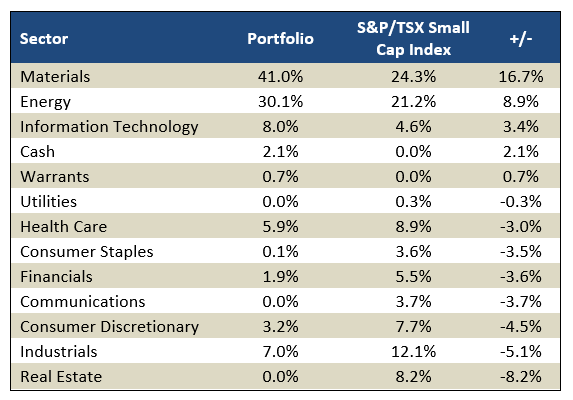

Below are the portfolio and index sector positions as of September 30, 2021:

As anticipated, this quarter was challenging with many factors at play. Last year, as we entered the COVID economy, governments globally opened the spigots providing monetary and fiscal stimulus which rescued financial markets. The extraordinary government spending helped engineer a rebound in consumer spending and assisted economies recover out of the worst pandemics in recent history. Stock markets exploded to the upside.

As we turned the calendar to 2021, we were in the rotating phases of COVID with the Delta variant creating concerns about future economic growth. The word “transitory” inflation became a commonly used description for the higher CPI and PPI data; which were much higher than what we had historically become accustomed to. There were sudden and rolling supply chain issues (example being semiconductors) and labour constraints became common. Although revenue targets for the most part were being met, margin compression became a concern which pressured many stocks who missed earnings or guided lower.

With the higher inflation (albeit “transitory”) levels, strategists and economists began speculating on when the Fed would begin to tighten. US treasury yields bounced higher by quarter end, helping elevate the US$ creating headwinds for many resource-oriented stocks. China was having issues of there own, there was the Evergrande Real Estate crisis and the power crunch with rolling brown outs adding to global supply chain issues and concern over the macroeconomic outlook in China. With all these issues, it is not surprising that the Canadian small cap market consolidated prior quarters very strong gains.

Going forward, we believe the consolidation and reset was healthy and will lead to another push higher in stocks. We believe investors are underappreciating the impact of low rates and high inflation on material stocks. The market has begun to price in the Fed tapering with yields moving up and trading around 1.5%. The US$ strength seems largely about safety and concerns about global economic growth. As the Delta variant crests, global economic growth is likely to pick up in the fourth quarter helping the market move beyond the current correction and begin a period further weakness in the US$.

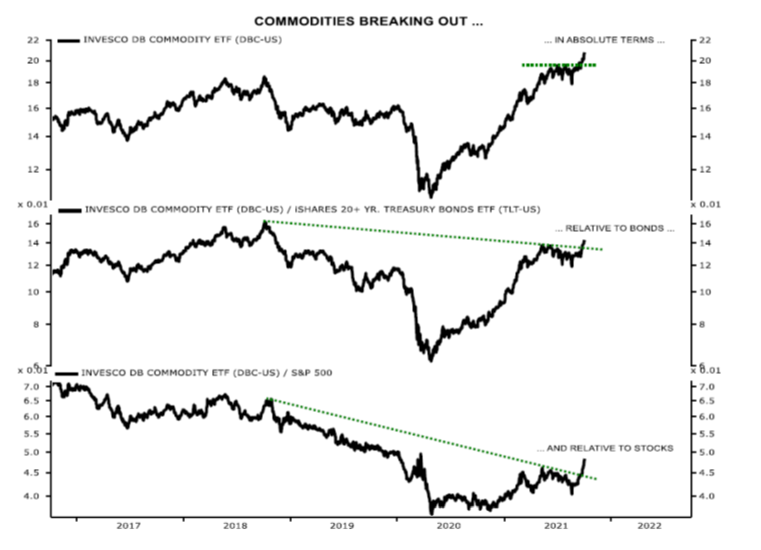

Commodity stocks have broken a three-year downtrend against all asset classes (see chart below).

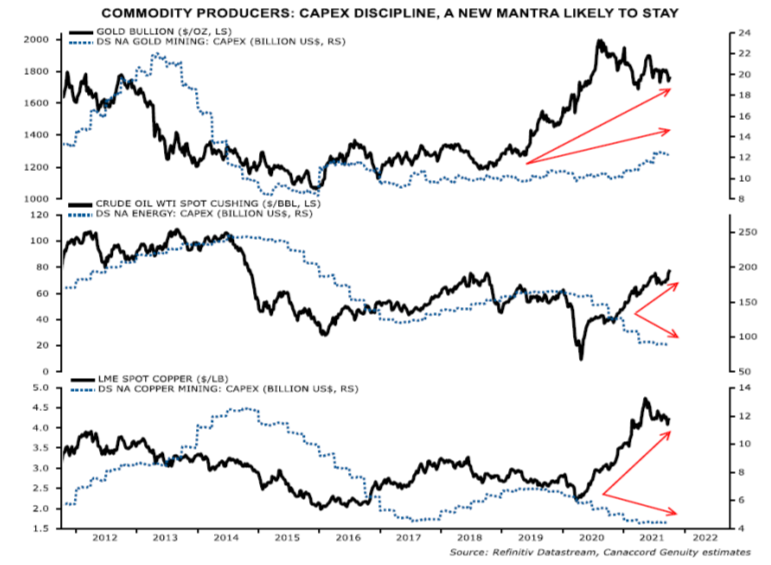

This bodes well for the sector as global growth begins to reaccelerate. As an asset class, despite the move in the underlying commodity, the stocks are still very undervalued on a historical basis when looking at multiples/valuations. The group is showing strong capital discipline because of shareholder pressure. Whatever the reason, the result is clear, strong demand and less supply will result in robust commodity prices. This bodes well for cashflow and earnings and may eventually bring higher multiples to this unloved area of the market.

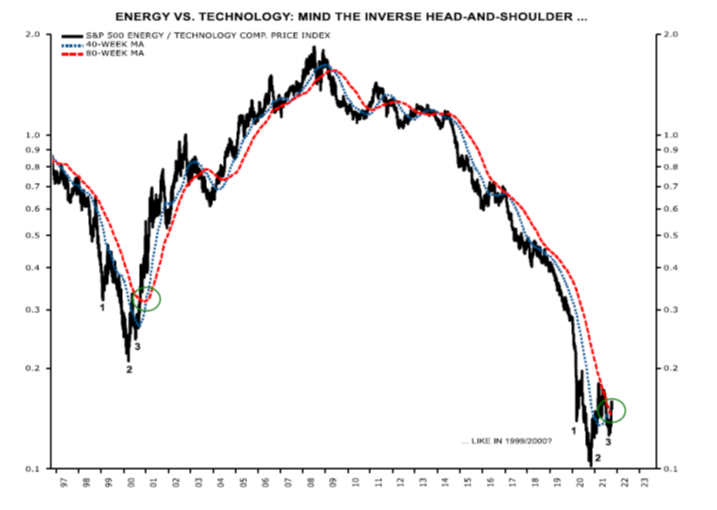

Energy companies in the third quarter began returning capital to shareholders via longer-term dividend policies; something rarely seen by this group in the past. We hold overweight positions in energy, base metals as well as precious metals. The chart below shows energy versus technology over the last 25 years and leads us to ask, “are we entering a period of strong outperformance in hard assets”?

As mentioned in the past, we continue to search for new, emerging companies that are growing at significantly higher rates than the Canadian Small Cap universe.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.