Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

October 28, 2021

As discussed in our second quarter letter, we felt the market needed to digest last years move with the recent headwinds providing investors challenges as we move through 2021. The third quarter was just that; we continued to grind sideways with a decidedly downward bias. We do think this correction is healthy and is setting the Canadian Small Cap Index up for eventual outperformance. Markets are never easy through the September/October time frame and this year is no different.

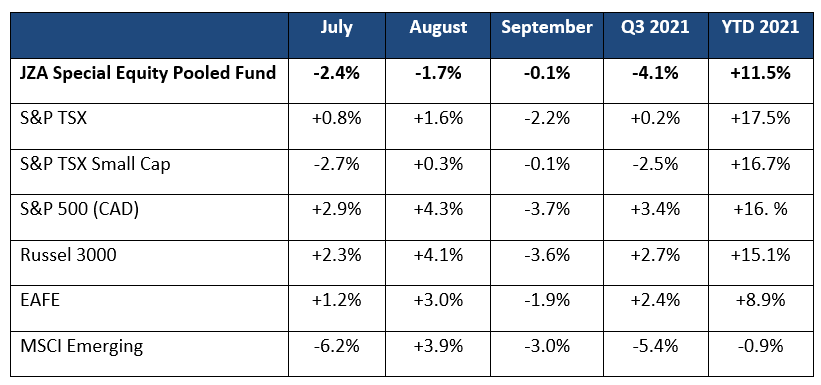

Below is a table with the fund’s performance relative to various global indices.

The fund was down -4.1% for the quarter versus the S&PTSX Small Cap Index which was down -2.5%. Despite the underperformance, the fund continues to perform well as we move through this correction. Last quarter the portfolio saw very strong performance in energy stocks with WTI gaining +5.8% and natural gas gaining +60.4%. The underperformance in the portfolio came from materials, both precious metals and base metals, as these sectors struggled against the strong US$, concerns of central bank tapering, slowing growth in China, and continued fears of a 4th COVID wave.

The three names that detracted most from the returns for the quarter were VIQ Solutions Inc., K92 Mining and Roscan Gold Corp. These three stocks cost the portfolio -1.8% in the quarter. There is no surprise that two of the portfolio’s detractors were gold stocks.

Starting with VIQ Solutions, this company combines artificial intelligence and voice/video capture technology to transcribe and manage data in rigid security environments such as legal, criminal justice, insurance, government, corporate finance, and media. The company raised money this past quarter in the US marketplace. We did not participate in the deal and have not added to our position as we are somewhat frustrated with management, who did not listen to our advice to not raise capital in the US market with a marketed deal. The stock price suffered prior to the stock offering, falling from $9 dollars in July to the eventual US offering at $4.25. Despite the poor execution in the financing, we continue to hold the position, and are looking for indications on how their acquisitions are being integrated before adjusting the portfolio’s position.

K92 is the portfolio’s largest gold weight. With the gold sector coming under pressure in the third quarter, it is not surprising that it detracted from the portfolio’s performance. K92 remains one of our favorite gold companies. The company owns the Kainantu Gold Mine in Papua New Guinea. The mine is a high grade, low cost underground mine that has doubled throughput to 400,000 tonnes/year and production to 120,000 oz/yr. As a result of successful exploration, the company will increase output to 315,000 oz/year by 2023 with an all-in-sustaining-cost of US$486/oz. The company continues to drill with 11 active rigs and expect further resource expansions which will be paid for through free cashflow. The stock’s weakness has provided us with an opportunity to accumulate more in your portfolio.

Roscan Gold Corp. is a well managed gold exploration company that is focused on expanding its resource in West Africa. It’s Kandiole Project is in West Mali and boasts a significant land position in the prolific gold prospective Birimian belt. Just recently, Asante Gold took a strategic position in Roscan. Over the last few months B2Gold has entered international arbitration against the Republic of Mali with respect to Menankoo exploration permits. This issue is specific to B2Gold but the dispute had a negatively affected investor perception on Roscan (in addition to the weakness in the gold sector). We have recently added more to the portfolio’s Roscan position.

The three names that added most significantly to the portfolio’s performance include NanoXplore Inc., Horizonte Minerals and Crew Energy. Collectively these three names added +1.8% to the quarterly performance.

NanoXplore is a graphene company which has begun manufacturing and supplying high-volume graphene powder for use in industrial markets. Graphene is the lightest, strongest, thinnest, best heat and electricity conducting material discovered to date and is a great substitute for carbon black. The company has a patented proprietary clean technology to produce its powders. Martinrea International holds a significant interest in Nanoxplore and has provided its manufacturing expertise to the company as it has gone from concept to producer. The company has announced significant orders and distribution agreements over the last few months. The stock has had a significant move and we have taken some profits but maintain a core position as the future growth prospects are tremendous.

Horizonte Minerals is a nickel company that is developing two, tier one projects in Brazil. The Araguaia ferronickel project and the Vermelho nickel-cobalt project are both high-grade, long-life projects with some of the lowest costs in the sector. These projects provide Horizonte with a scalable production profile of 50,000 tonnes of nickel per year which would position the company as one of the top nickel producers globally. This quarter, the company received formal credit approval from two export credit agencies and received approval for a US$346.2 million senior debt facility for the development of Araguaia. The stock reacted very positively to the news, and we have trimmed our position into the strength. While we are very excited about the prospects of Horizonte and the nickel market, we have trimmed the position on price appreciation and anticipate adding to our position later in the year. The company will likely need to raise equity to move forward which may provide some headwinds in the near term and give us an opportunity to add to our position.

Crew is a natural gas company operating in Western Canada. It was a new energy addition to the portfolio last quarter. The company has a large undeveloped Montney land base in British Columbia. This resource play ranks among the top natural gas basins in the world with strong tier one economics. As many smaller E&P companies in Canada, Crew has been using the current price environment to repair its balance sheet but in the second quarter it opted to accelerate spending to accelerate growth. The stock suffered and at this point, we decided to add the position on our positive mid/long-term outlook on the natural gas price environment and on Crew’s Montney assets which are highly coveted and could very likely be of interest to larger players in the basin. As energy stocks have had a significant move this quarter, we have reduced our position in Crew and in the entire energy sector (but continue to have a large overweight).

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.