Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

April 23, 2021

As we entered 2021, we were somewhat apprehensive. 2020 was an extraordinary year by any measure resulting in an incredibly buoyant stock market with its continued strong rally into the fourth quarter providing the portfolio with large, outsized returns. With that in mind, we stated in our last letter that we thought markets likely needed to pause and reset, but in the first two months of 2021, small cap performance continued to push upwards undeterred. As the rally continued, we began to sell some of the most expensive stocks in the portfolio. “Green” stocks such as Xebec and Greenlane were sold, as were several technology stocks that were trading over 20 times sales, such as AcuityAds, Docebo and Tecsys. Positions that were added were in the Base Metal, Industrial and Energy sectors. Given the longer correction experienced in the Gold sector (which began in August of 2020), we also began adding positions in gold and silver stocks.

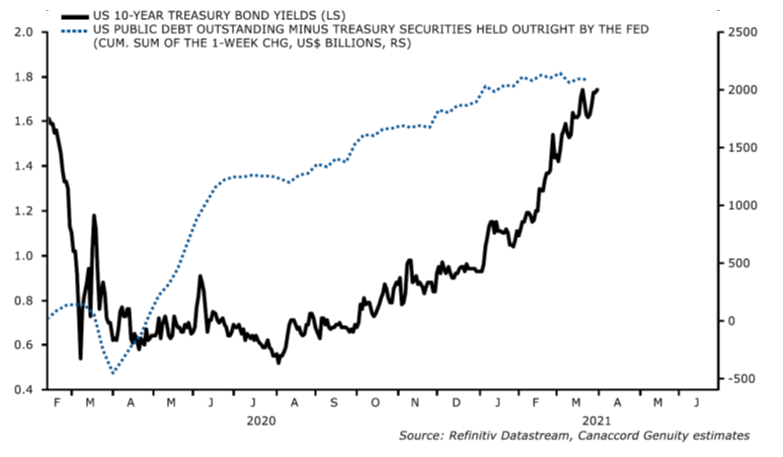

Towards the end of February, the market began to wobble, and it appeared that the consistent leadership of growth stocks that we had witnessed for the past many years was beginning to shift in favour of value. This trend change corresponded with the 10-year bond yield rising beyond 1.2%. The rise from 1.2% to the 1.8% level was swift and created ripples throughout the market.

With the rise in yields, the US dollar, which had previously been weak, mounted a counter trend rally which continued to weigh on the gold sector. We believe this is a counter trend rally and that the US dollar will continue to sell off, which will provide gold stocks with a more favourable backdrop in the next few quarters.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.