Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

April 23, 2021

After the robust ending to 2020, we fully expected that the first quarter would be somewhat challenging with perhaps a reset/pause in the market. Instead, we continued to launch strongly out of the gates, and it was not until March where we began seeing a pause. Despite the small correction, the portfolio had a decent quarter, albeit showing a small underperformance to its benchmark. The underperformance was a result of the Financials, REITS and Defensive sectors outperforming, playing catch up from their underperformance in 2020. Materials were in correction mode with the Gold sector leading on the downside while the Base Metals sector continuing to appreciate; the result being the portfolio added positive attribution relative to the material index. Energy was also an outperformer, which helped the portfolio stay close to the benchmark’s performance, given the portfolio’s overweight position. Technology, after being a long-term leader in the market, begun a correction process which is not surprising given some of the lofty valuations.

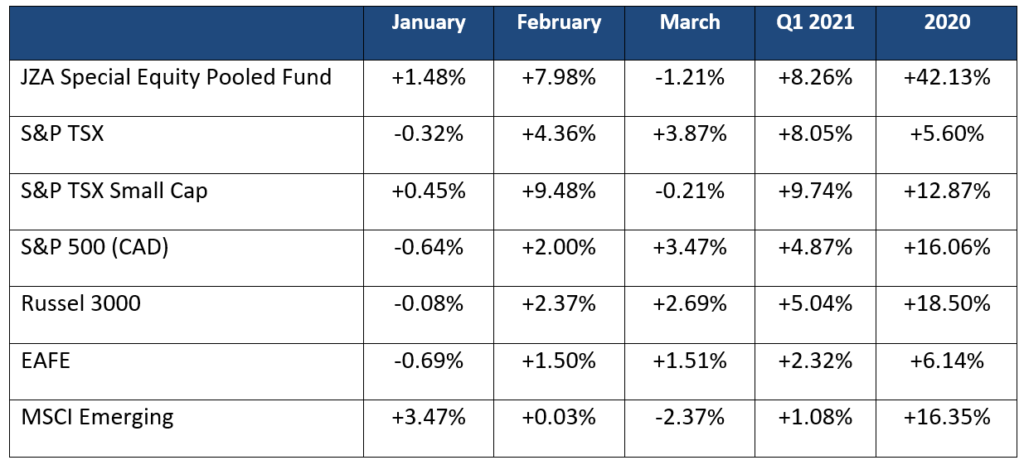

Below is a chart showing performance relative to our benchmark and other global indices.

The three stocks with the largest contribution to performance for the first quarter of 2021 included AcuityAds, Tamarack Valley and Capstone Mining. Collectively these three names added +3.0% to the portfolio’s return.

AcuityAds is a leading technology company that provides marketers programmatic advertising as a one-stop solution for omnichannel digital advertising. The company’s journey automation technology, illumin™, offers planning, buying and real-time intelligence from one platform in which the customer can navigate their advertising campaigns by themselves. We like the space AcuityAds occupies but felt after a tremendous run, the stock was overvalued and have since exited the position. The stock has corrected significantly, and we continue to monitor and evaluate the company.

Tamarack Valley is an oil and gas exploration and production company located in the Canadian western sedimentary basin. We have a long history with the company and have a great deal of regard for management. After living through the negative oil prices in 2020 and seeing valuations in the energy sector crushed, we increased our energy weight to overweight towards the end of last year including a sizable position in Tamarack. Tamarack Valley was well positioned coming out of the crisis given their exceptionally strong balance sheet and have been able to make several astute and accretive acquisitions in the space. We have recently reduced the positions slightly but are still a holder.

Capstone Mining is a copper miner with two operating mines, Pinto Valley in the USA and Cozamin in Mexico. Both mines have undergone significant optimization programs and or expansion over the last year or so, improving their cost profiles. Copper has also had a significant move upwards resulting in significant increases in EBITDA for the company. The company has also made forward strides on their development project, Santo Domingo in Chile simplifying the ownership structure and are now able to seek a partner to build the project. We have a favourable view on copper and like Capstone’s growth profile. We have taken some profit in the position to redeploy in some copper names that are underperforming Capstone and continue to hold a significant position in the name.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.