Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

January 31, 2019

But where to from here…

We have had a significant repricing of stocks both in Canada and globally as many participants are factoring that global growth deceleration is here and is expected to continue for the foreseeable future. We believe that the recent volatility in equity markets is an over-reaction to slower growth prospects combined with unwinding of excessive speculation following an unbroken rally since the financial crisis ten years ago. As investors realize that a recession is not in the cards for 2019, the risk-off market sentiment will fade, and we will get the late cycle rally we had expected in the last half of 2018.

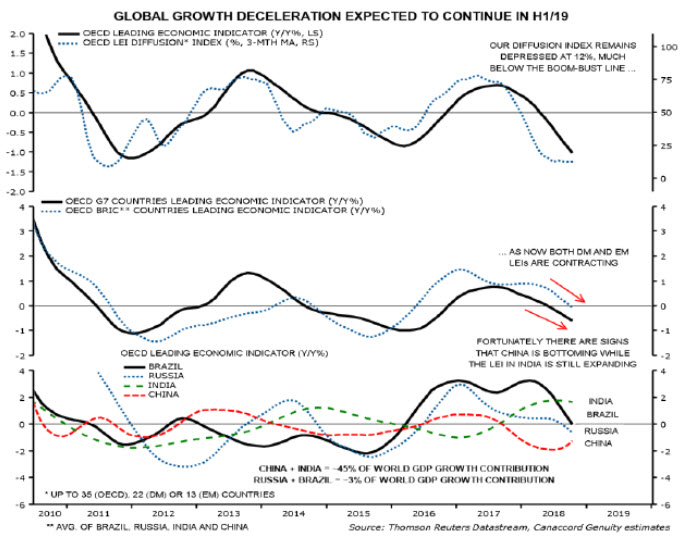

Both developing markets and BRIC countries leading indicators are contracting but India remains robust. It appears China is bottoming, and the US is still trending upward. Furthermore, the US dollar finally appears to be toping, which supports commodities and thus emerging markets and Canada.

As can be seen below, EEM have held the lows in October and are trending up, which should be bullish for our portfolio’s energy and material holdings.<!–nextpage–>

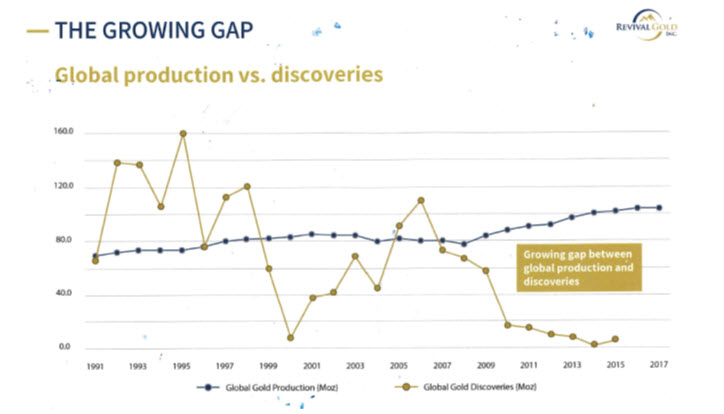

We are more long term bullish on materials versus energy due to the ongoing underinvestment in materials. The chart below shows a picture of continued strong production in the gold sector but the significant decrease in exploration dollars.

The same picture is true of the base metal sector. On the demand side, as Electric Vehicles become more mainstream the demand for copper and nickel will accelerate from these current levels. We do believe there will be some resolution to the trade dispute between China and the US, and China has already begun to reflate its economy. The inventory picture within the base metal sector is already extremely tight. We think 2019 will bring significant outperformance in the sector. We go into 2019 overweight energy, base metals, and gold.<!–nextpage–>

We feel that with the flight of capital from Canada, the market cap sectors and stocks in where we are finding opportunities bode well for our equity strategy as the opportunities that we see, are similar to valuations we saw during the lows of 2008. This should result in robust returns in areas mostly ignored by large or all cap managers.

Looking forward to a better 2019. Wishing you health and prosperity in 2019 and if there are any questions, please do not hesitate to contact me.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.