Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

January 31, 2019

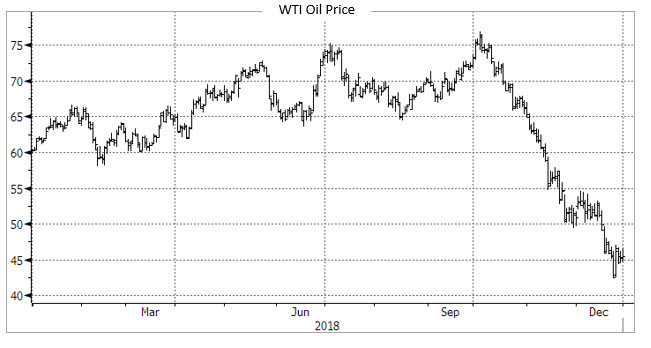

Adding insult to injury was Canada’s inability to successfully permit/build pipeline capacity. This created an extremely difficult pricing environment for Edmonton light producers with differentials blowing out to greater than $20/barrel.

Since the lows in December we have seen two things happen: OPEC has cut production and through political intervention the Alberta government has mandated production cuts. The result has been a meaningful rebound in WTI toward $55/barrel and a significant reduction in differentials (high single digits). With oil off over 40% in the quarter, it should be of no surprise that the energy sector was the worst performing sector (the S&PTSX Small Cap Energy index was down 33.6%), however with the oil price rebound we would expect a sharp recovery in the first quarter of 2019.

The success of horizontal drilling in what were previously uneconomic basins highlight an inherent issue for the oil and gas industry. Although the Saudi’s and OPEC still act as the swing producer, their influence to control supply is diminished with more and more supply coming from the US. Until Basins such as the Permian, mature, the price of oil will most likely be range bound between the $50-$65. The energy stocks should be traded accordingly, as prices increase to the upper end of the range will likely get US producers to increase production. The Canadian issue has further complexities. The government policy to reduce supplies has helped the differentials short-term, but it has not solved the long-term issue of take-away capacity. Valuation of the sector at the end of December was extremely depressed and thus we came into the year 6% overweight the index, with a strong tilt toward Brent producers such as Parex and Grand Tierra.

Other factors causing the market volatility in the fourth quarter were the on again off again resolution of the US/China trade dispute. Which despite back and forth rhetoric is still not done but both sides seem to understand a deal would be beneficial to both markets and help stabilize the current global uncertainty.

The US market made a new high in September but that changed on October 3rd when US Federal Reserve Chairman, Jerome Powell, made the unfortunate comment that the US interest rates were still a “long way” from the normal level. The market began anticipating that four rate rises were possible in 2019; thus, breaking the back of the US stock market, and unfortunately taking the rest of the world down with it. The fear of an overly aggressive Fed (and the fear it would cause a recession) contributed to the downdraft in base metal stocks (despite a very constructive fundamental picture with regards to supply/demand and inventories). On top of the normal selling pressure from recession fears, we saw several large global metals portfolios liquidate in the quarter. The most significant of which was the M&G Gold fund. This unwind put significant pressure on the smaller producers and the exploration companies (several of which were held in the portfolio). Despite the price of gold being up +7.7% in the quarter, these liquidations caused many gold holdings in the portfolio to trade down in the quarter. Gold holdings like Roxgold, Goldenstar, Troilus and Barkerville, all underperformed due to large portfolio liquidations.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.