Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

February 5, 2020

The monetization of Global debt. Global debt hit a record high of over $250 trillion in the first half of 2019, led by a surge in borrowings in the U.S. and China, according to a new report. The IIF said the overall number exceeded $255 trillion by the end of 2019. China and the U.S. accounted for over 60% of the increase. Similarly, Emerging Markets debt also hit a new record of $71.4 trillion (220% of GDP). While record low interest rates has allowed the servicing of this debt to be manageable, there is very little consideration being paid to the ultimate redemption of this debt. Normally we see debt increased in dire times and paid down when economic growth resumes but, in this cycle, we have seen a continual growth in debt while economic growth has remained below historical levels. The ultimate resolution is most likely the ‘monetization’ of this debt by allowing currency values to fall and thus reduce the value of that debt liability. This would be similar to what occurred in South America in the 1970s, which resulted in a period of hyper-inflation and massive currency devaluations. This time around that would also include the mighty U.S. dollar, since that country has added most aggressively to debt in the past decade. In this scenario we see gold, as the ‘anti-currency’, as being the biggest beneficiary and we continue to see a gradual upward move in gold bullion to the US$2000 level. On the other side, the world’s banks would be the biggest centers of risk.

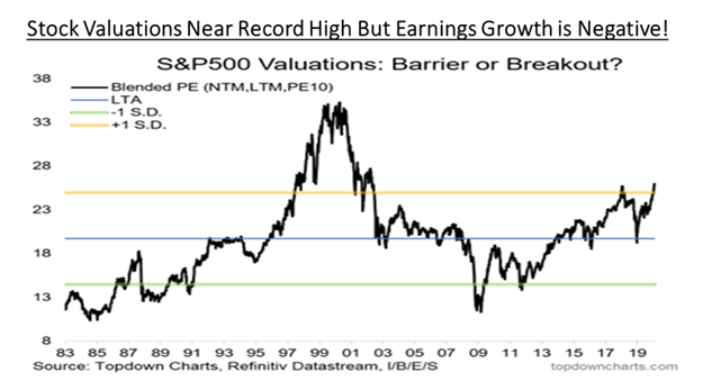

Are Zero Interest Rates Making Us Throw Out all the Old Playbooks on Investing? In almost 40 years of managing money, our strategy has always been to look for cheap stocks to buy and then sell those stocks when valuations became excessive, with the caveat that we would generally attribute a somewhat higher multiple to companies with consistently higher earnings growth rates. The age of zero interest rates appears to have changed all of that or else we are just seeing the speculative phase of a bull market that has lasted almost 11 years. Low interest rates allow for future earnings to be discounted at a lower rate, such that investors are willing to pay much for today for expected earnings in the future. But that dynamic seems to have taken on a life of its own with huge discrepancies. Companies such as Netflix and Uber don’t even need to show earnings as long as revenues are growing while the valuation of so-called ‘value stocks’ continues to sink. Shopify trades at over 35 times revenue and 100 times operating cash flow and yet we see metals and energy stocks which aren’t able to get better than valuations of 3-4 times operating cash flows. Similar story on defensive stocks where utilities and pipelines can get earnings multiples above 20 times simply because they have large dividend yields and are effective ‘bond proxies.’ Our conclusion is that this ‘new world of investing rules’ will not last. Earnings and valuations will ultimately matter and we will get a recession and a bear market that will undo these excesses. When that comes remains the bigger mystery.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.