Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

February 27, 2018

Going forward we have said that this period reminds us of 1987. At that time, the U.S. dollar had slipped amid discord with Europe and unnecessary stimulus measures; a new Fed chair (Paul Volcker) hiked interest rates too quickly; bonds suddenly sold off; and then stocks crashed. While the ’87 crash was frightening it was relatively short-lived, and the market resumed its upward trend relatively soon afterwards. This pattern seemed to be taking place again in the current correction as stocks recovered most of their losses in the three weeks following the big sell-off. But valuations and sentiment seem much more extended this time around. Also, the tax cuts in the U.S., the continued easy money conditions and the massive increase in deficits are coming at a time when the U.S. economy is already at full employment. This could be throwing more ‘fuel on the fire’ in terms of increasing inflationary pressure and the risk that the U.S. Federal Reserve will have to increase rates at an even greater rate than currently expected. With consumer and government debt levels at record levels, there is just no ability to absorb large rate increases without impacting growth.

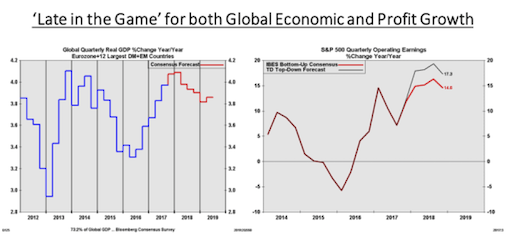

Despite the recent tax cuts in the U.S., we believe that profit growth is in the process of peaking for this cycle (as shown in the right panel below). After listening to dozens of quarterly earnings conference calls in the past month, I noted that rising input costs (raw materials and labour in particular) seemed to be the biggest concern of many CEO’s. Also, while a global recession is nowhere on the horizon right now, we have clearly seen a peaking in the ISMs and other survey data in both the U.S. and Europe over the past few months. That could indicate that we are in the process of seeing peak growth for this cycle. Stocks generally top out months before any major slowdown in growth. Is the February stock market volatility an early warning sign of this peak? While stock market averages tend to experience ‘V-shaped’ bottoms, they tend to have ’rounded tops.’

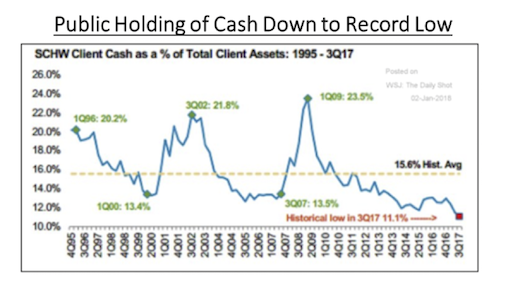

Last month we pointed out that the public’s holding of cash in their investment accounts was at record lows (see chart below), well below the levels seen at the prior stock market peaks in 2000 and 2007. This presents another risk for stocks as there is no ‘wall of cash’ sitting on the sidelines waiting to buy into any pullback. Moreover, as interest rates increase, the alternatives to stocks start to look more attractive.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.