Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

February 27, 2018

Last year, global stocks (except in Canada) did a slow grind higher all year without any pullback of more than 3%. This pushed many stock markets to record highs but it also drove stock valuations close to record highs, and it occurred while interest rates were increased three times in the U.S. and twice in Canada. Despite only mediocre economic and profit growth and all of the turbulence around the new government in Washington, stock market volatility (a traditional measure of investor fear or trepidation) moved to record lows and stayed there most of the year. Many money managers, ourselves included, had expected a stock market correction at some point last year given rising interest rates, high stock valuations, excessive investor optimism and the abnormal length of time without a correction. We carried those same expectations into 2018, heightened by an even harsher interest rate outlook and growing budget deficit projections in the U.S. But then stock market investors again ignored those risks and bought stocks at the most aggressive rate seen in three decades, except in Canada where weak energy stocks once again held back the overall averages.

The net result was that, by January 26th, the stock market was sitting at an all-time high and investors everywhere were marveling at what an impressive start to the year it had been. Then things suddenly fell apart. The S&P500’s longest streak without a 5% correction since 1927 came to a violent end as the index lost 10% in a 5-day span, the quickest such decline on record. All the talk about strong earnings growth, tax cuts and a synchronous global economic expansion went ‘out the window’ as this sell-off was not about business or economic fundamentals. The trigger for the fall was the realization that the easy money policy that had funded the huge rise in financial assets over the past five years was coming to an end as central banks were clearly removing the ‘punch bowl’ with rising interest rates, at a time when investors thought there was no risk in owning stocks. These rate fears were fueled further as the U.S. unveiled budget projections that showed deficits running above $1 trillion annually for the next few years and overall debt moving to record highs, with projections showing the debt could rise to an unprecedented level of over 100% of Gross Annual Output.

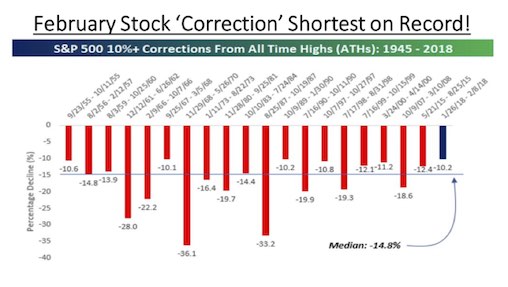

The sell-off on the S&P500 Index from the late January peak to the Feb 9th low counts as the shortest on record since 1945 and is joint second-lowest in terms of the magnitude, according to Bespoke Investment Group. The median postwar decline for corrections from record highs (drops of more than 10%) is 14.8%, the research shows.

But just as quickly as stocks sank into that correction, they once again came back, recovering over 75% of those losses in the major averages over the balance of February. So where does that leave us? After having sat on our trading desk and watched the markets on February 5th, it seems hard to conceive of this market suddenly shaking off all those warnings and going back to record highs. It was probably the biggest intra-day move seen in three decades as we watched a modest 200 point loss on the Dow Jones Index turn into a 500 point decline by mid-day and then accelerate in the afternoon, falling over 1000 points and then quickly melting down to a 1600 point intra-day decline before a slight recovery to an 1100 point loss on the day! This was volatility like the market had not seen since the ‘Flash Crash’ back in 2010. We saw another 1000+ point loss on the index again on Thursday of that week (Feb. 8th). Investor confidence had to have been shaken somewhat by this volatility as opposed to re-enforcing the ‘buy the dip’ mentality that investors have enjoyed since the 2011 lows. Moreover, the cause of this fall had been a ‘stronger than expected’ U.S. employment report on Feb. 2nd that raised fears of rising wages/inflation and more aggressive upward moved in interest rates, undermining the biggest source of stock market strength over the past seven years. That problem is going to remain with us for at least the next year. The key variable supporting the major financial market gains of the past few years is being removed!

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.