Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

July 29, 2022

In terms of how aggressive central banks will ultimately need to be on interest rates, there are a variety of encouraging signs that inflation may be close to an inflection point and that some of the initial underlying drivers are now backing off. Most obviously, commodity prices are simmering down broadly. A basket of key commodity prices has melted almost 20% in the past seven weeks alone from the early June peak and is now almost precisely right back to levels prevailing in the days prior to the invasion of Ukraine. We are a long way though from seeing a reversal in Fed policy like we saw at the end of 2018, after stocks had dropped over 20% in the fourth quarter of that year. Central banks have only just begun their tightening and inflationary expectations have become somewhat ‘embedded’ as evidenced by ongoing wage gains and price escalators. Our expectation is that rate increases will continue into the back half of 2022 but we might not see any further increases next year as inflation will have already receded back to the 2-3% range on slower economic growth.

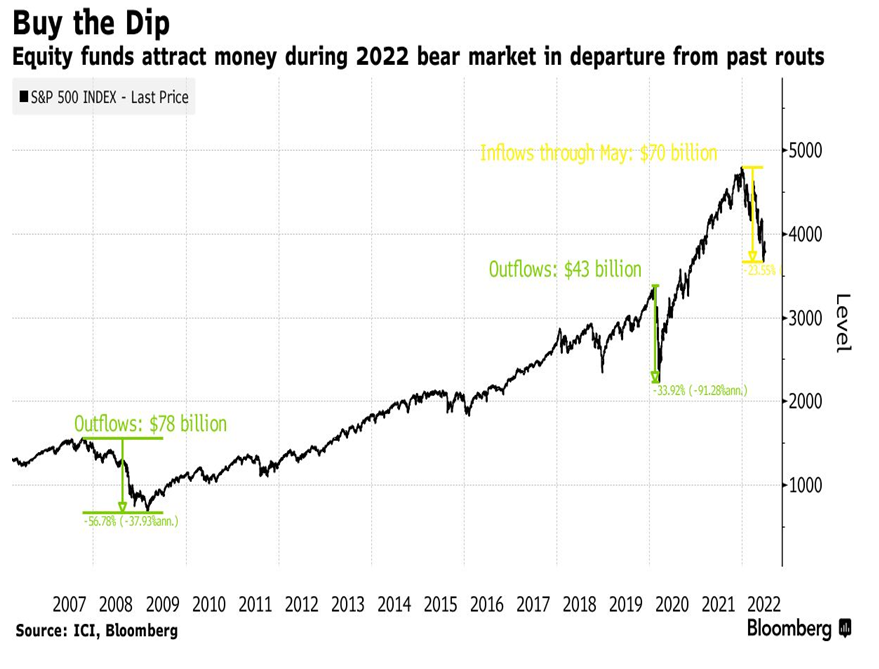

Markets very well may be oversold technically, and we think the long-run outlook for stock returns has improved markedly since the start of the year, but that is very different from saying the stock market has definitively ‘bottomed’. We need to have some reliable measure of investor sentiment to make that assessment. If everybody is itching to get back into the market at the bottom, it probably means we are not yet at the ‘capitulation phase’. Investor ‘despair’ rather than optimism is symptomatic of stock market lows. While punishment for optimism has been swift in 2022, a decade of bull-market conditioning is proving difficult to vanquish. In the 2009 bear market (S&P500 fell 56%) U.S. investors pulled $78 billion out of Equity Funds. During the 2020 downturn (S&P down 34% in a month) investors redeemed another $43 billion from stocks. However, in the current downturn, which has seen the S&P drop over 23% at the lows, investors actually put $70 billion back INTO stock funds.

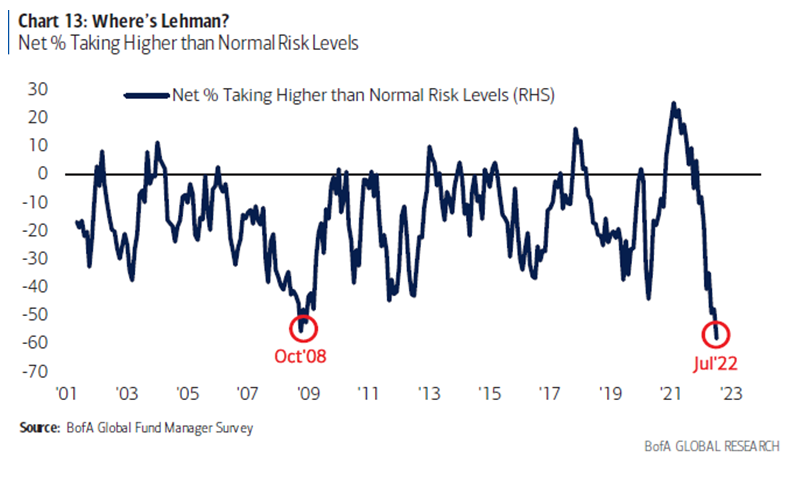

While retail investors have been throwing more money into stock funds during this year’s selloff, institutional investors (a much larger contingent of total investment dollars) have gone in the other direction and slashed their exposure to risk assets to levels not seen even during the global financial crisis. In a sign of full capitulation amid a “dire” economic outlook, according to Bank of America’s Monthly Fund Manager Survey, global growth and profit expectations sank to an all-time low, while recession expectations were at their highest since the pandemic-fueled slowdown in May 2020. Investor allocation to stocks plunged to levels last seen in October 2008, while exposure to cash surged to the highest since 2001. A net 58% of fund managers said they’re taking lower than normal risks, a more bearish level than the record seen in the survey during the global financial crisis in 12008. Also, in the survey, equity fund managers’ cash holdings hit 6.1%, the highest tally since October 2001. A net negative 40% of respondents said they are overweight equities; that’s the percentage of respondents who said they are overweight stocks minus the percentage who aren’t. When positioning reaches such bearish extremes, stocks tend to have only one direction to go, even if fundamentals continue to look shaky. Putting together the more bullish outlook of retail investors compared the record bearishness of institutional investors leads one to conclude that the ‘big money is bearish!”

Our shorter-term investment strategy in this downturn has been to look to for positions in depressed valuation sectors or those reflecting excessive pessimism, which should have limited further downside yet some strong recovery potential. We are seeing such opportunities in energy, where the stocks dropped over 20% in the June-July period despite trading at record low valuations. But the forces keeping energy prices high are enduring, whether there is a recession or not. Key names in the oil sector that we have been adding include Crescent Point, Whitecap Resources and Cenovus as well as natural gas producer Arc Resources. We see similar oversold opportunities in the consumer sector. Consumer discretionary stocks, specifically, have the worst returns of any S&P500 sector, with year-to-date losses over 30% as sectors such as autos and travel have sold off dramatically and already reflect a recession scenario. We added to positions in GM, Fedex, Magna, BRP (skidoo/seadoos) and Air Canada as well as U.S. financials (Citi, Amex and JP Morgan) on the first half weakness.

While we may be more ‘constructive’ on the outlook for stocks, given our expectation tha inflation has peaked and valuations have reset to a large degree, there remain many who are much more dour on the outook. Perrrenial bear, Economist Nouriel Roubini, said the US is facing a deep recession as interest rates rise and the economy is burdened by high debt loads, calling those expecting a shallow downturn “delusional.” “There are many reasons why we are going to have a severe recession and a severe debt and financial crisis (and) the idea that this is going to be short and shallow is totally delusional.” Among the reasons Roubini cited was historically high debt ratios in the wake of the pandemic. He specifically mentioned the burden for advanced economies, which he said continues to rise, as well as in some sub-sectors.

Differences of opinions is what makes markets work!

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.