Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

July 29, 2022

As we typically see in stock markets and had written about last month, when investor sentiment gets as bearish as it got, expectations for earnings plummet and cash levels rise to cyclical highs, stocks do tend to find a bottom, at least for the short term. From mid-June to mid-July, the S&P500 rallied over 9% and the ‘technology heavy’ Nasdaq Index jumped over 13%. Underpinning that short-term recovery in stocks was a decline in bond yields, with the 10-year U.S. Treasuries falling below 2.80%, well under its mid-June peak near 3.50%. The conclusion from this is that investors have started to price in a fairly severe economic downturn, which is why there was a switch back to the ‘growth’ stocks that tend to do better in a period of slower growth and lower interest rates. That also dovetails with the fact that the more ‘cyclically-oriented’ sector such as industrials, metals and energy all sold off sharply in the June downturn. Investors then had to focus on second quarter earnings reports and forward guidance to either confirm the recession view or indicate a less severe slowdown.

The earnings results were mixed, with many companies missing projections due to rising input costs and ongoing supply chain issues. But the results did not support the most bearish views that had taken stocks down to their mid-June lows and the valuations were already reflecting some bad news. Walmart Inc, the world’s largest retailer, cut its profit outlook for a second time in two months, saying inflation is causing shoppers to spend more on necessities such as food and less on discretionary items such as clothing and electronics, forcing the company to sell off some excess inventory at reduced prices. The stock dropped sharply on those results. Other corporate giants such as General Motors, Microsoft, Amazon and Google parent Alphabet Inc. reported second-quarter results that fell slightly short of Street expectations, but the stocks actually rallied since investors had been prepared for worse news. Ditto for Canadian tech giant Shopify, where second-quarter financial results indicated a continued slowdown in online spending at the same time as they had to deal with rising labour costs, all of which lead to losses, yet the stock rallied as well. A handful of companies did beat expectations, lead by Apple and Amazon and also including Visa, Amex, Coca-Cola and McDonald’s, all of which provided some optimism that companies are managing their way through this downturn. The fact that some stocks are rallying even on earnings misses strongly suggests that investors were already prepped for bad news.

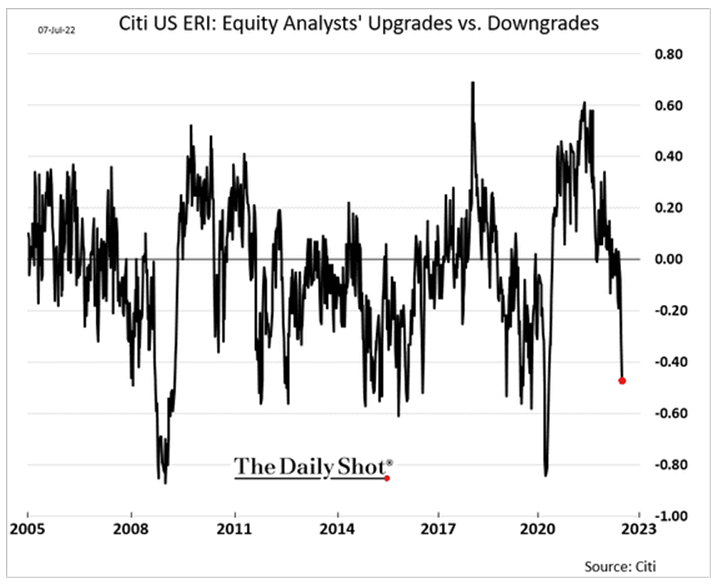

Consensus analyst estimates are probably still too high across most sectors as analysts have been somewhat slow in adjusting to a slower economic backdrop. We will be looking to see how potential downward revisions could affect stock prices and broader markets. But analysts are coming around to the new economic reality and have been busy slashing expectations at a more aggressive rate as earnings are being reported, as shown below. The ratio of analyst upgrades to downgrades has dropped to the negative .5 range, getting much closer to the lows of negative .8 seen at the market bottoms in 2009 and 2020, and a long way from the positive 0.6 ratio seen at the market peak last November.

The economic news in the past month hasn’t really done anything to help the bullish case for stock investors though. Core inflation reports in both the U.S. and Canada continued to surge to 30-year highs and exceeded expectations, dampening hopes that central banks might soon lighten up on their newfound hardline policies. To the contrary, the Bank of Canada actually surprised markets with a full 100 basis point increase in short-term rates. That gave the U.S. Federal Reserve ‘cover’ to implement a similar move at their July 27th meeting, but they stuck to the script and ‘only’ took short-term rates up another 75 basis points, the same as they did in June. At the press conference after that meeting Chair Powell indicated that now they will sit back and watch the inflation data in particular over the next two months before their late September meeting to decide if a similar rate hike would be appropriate or whether they will start to wind down the ‘tightening’ of financial conditions. While stocks did rally on that information, investors need to understand that these central banks are strongly determined to bring down inflation levels, since they bring a much wider and negative impact on the entire population than the level of stock prices. The risk for markets remains that this plan to bring supply and demand for goods and services back into balance might end up driving the economy into a recession.

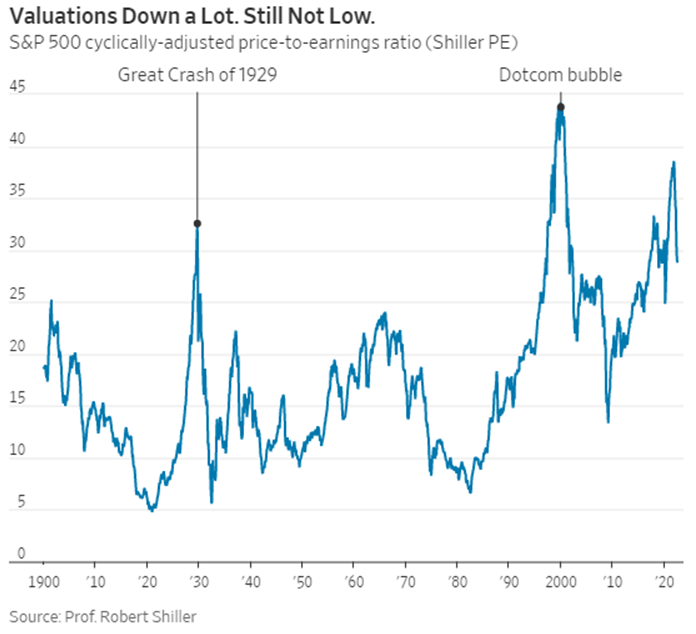

One factor favouring a more positive outlook for stocks is that valuations have corrected. However, as shown below in the chart of the ‘cyclically-adjusted price-to-earnings ratio (the Schiller PE), valuations are nowhere near the lows seen at prior market bottoms. While down significantly from the peak, the S&P500 still trades at a premium to history on forward P/E (16.6x vs. the long-term average of 15.5x) based on EPS forecasts that are still near a potential cyclical peak. Investors will not be able to count on higher valuations to take stocks higher. Instead, they will need to see a continuation of earnings growth. That could be a ‘tough ask’ given an impending economic slowdown. However, we believe that we may have already absorbed the bulk of the downside risk in stocks since this sell-off has already been so severe. The severity of the eight-month drop in stocks from November’s peak has been exceeded only twice since 1881; the first time was the 1929 stock market crash and the second time was in the wake of the ‘dot-com bubble’. Bottom line, there may be more downside in stocks in the short term but the ‘risk-reward’ tradeoff for being in stocks has improved dramatically since the beginning of the year. Unless investors feel they can identify stock market bottoms accurately, it is time to add back to stocks.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.