Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

January 7, 2022

The one thing that seems to be changing (for the first time in over a decade) is the outlook for interest rates. The low/zero rate policy of most global central banks has lead to a surge in stock prices over the past 12 years, but one that was only 20% due to rising earnings and 80% due to rising valuations for those earnings. That tailwiind is most surely gone. Valuations will contract so that earnings growth will have to carry the bulk of further stock market gains.

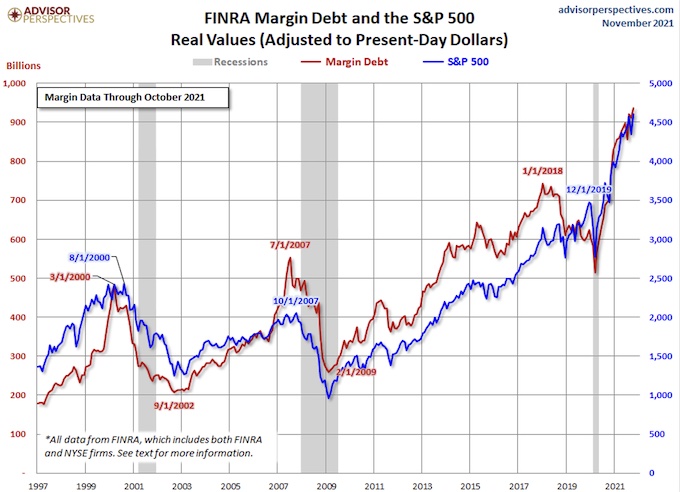

But rising interest rates will have effects beyond stock valuations. Who is most impacted by this and the answer is simple; those who have borrowed the most! That brings us back to the stock market again. The chart below paints an interesting picture between stocks (blue line; S&P500), margin debt (money borrowed to buy stocks; red line) and recessions (grey areas). We can accurately argue that oncoming recessions are the most relevant factor in determining stock market peaks. On that note we take some solace since we still don’t see any signs of recessionary pressure in the next two years at least. However, there is also a close correlation between margin debt and the S&P500. That may not determine the timing of any such pullback or bear market but, like many of the other indicators we have talked about, it does suggest a higher level of downside risk once any bear market does begin. More fuel for our ‘defensive, high yield’ strategy when it comes to picking stocks in 2022.

As 2021 comes to an end, Omicron has reminded the world that we are not yet out of the pandemic woods. However, despite rolling health scares, the economic recovery has continued, with global GDP already around 3% above its pre-COVID level, marking the fastest economic rebound in modern history. Retail Sales were an extraordinary 49% above their 2020 trough levels and 16% above pre-pandemic trends.

Inventory-to-Sales ratios have collapsed throughout the pandemic, falling from 1.7x to 1.1x. While supply constraints have contributed to these declines, robust sales is the primary culprit. Inadequate inventories, and the need to replenish them, should support robust nominal GDP in 2022.

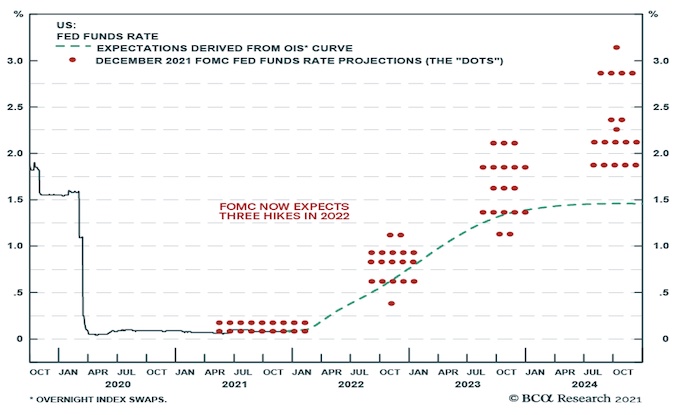

We have pointed out how extreme the risks are for stocks heading into 2022, mostly due to speculative activities and extended valuations. But a catalyst is needed for any correction or bear market. While we don’t see a recession on the horizon, we do think that interest rates could be the source of market volatility, much like it was in 2018. As expected, the U.S. Federal Reserve in December announced they would double the pace of asset purchase tapering, in effect bringing forward the end of the program to mid-March. Also from that meeting came their famous ‘Dot Plot’ outlook as shown below. Since last summer, when all Fed governors expected no rate increases in 2022, the latest reading calls for three rate hikes next year. What’s interesting now is that those series of red dots are now higher than the blue line, which is the expectation for those same interest rates at determined by current bond markets. Is this more hawkish outlook from the Fed just ‘bluster’ to try to keep inflation expectations down, or are investors simply expecting that inflationary pressures will recede on their own and that growth may not meet expectations, in which case the Fed would be forced to retract their more aggressive policies somewhat? Those are the types of changing forces that will cause stock market volatility in 2022, in our view.

Also, from that meeting, core inflation was revised up to 2.7% in 2022 from the prior estimate of 2.3%. Meanwhile, the projected unemployment rate was brought down to 3.5% in 2022 from 3.8% and the GDP growth outlook was increased to 4.0% from 3.8%. so good things are expected from the economy with continued expansion. But we believe that stock investors have to tread very carefully. Our strategy is to stay invested in stocks since they still look better than the alternatives, but our concentration will be on liquid, high yield, low valuation stocks and sectors that have some inflation protection. Energy, financial and industrials fit that criteria best.

Thanks for your continued readership and all the best for all of us in 2022!

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.