Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

January 7, 2022

When news of the Omicron variant of Covid-19 appeared in late November, stocks sold off sharply and quickly as many investors worried that we could be rolling back into lockdowns. Moreover, Fed Chairman Powell came out after their December meeting and, rather than reversing recent ‘hawkish’ chatter, he re-iterated that new, tighter stance on interest rates and the ‘taper’ of bond buying. His reasoning was that inflation is a problem that needs to be dealt with now, so the Fed will more quickly reduce their buying of bonds and moved ‘up’ the timeline for raising interest rates in 2022. On top of all of that, stocks had already generated strong gains for most investors in 2021, so the initial reaction was to ‘sell now and ask questions later.’ It certainly looked like the traditional ‘Santa Claus rally’ would not be making an appearance this year.

But, as quickly as the bad news set in, the momentum in stocks that we have seen since late March, 2020, kicked back in and the downturn ended almost as quickly as it started, limiting the losses to about 5%. Markets then rallied and the S&P500 pushed back up to record highs. What most surprised us about this rally was the fact that many of the ‘re-opening’ names were the ones that lead stocks higher. Cruise operators, airlines, energy stocks and consumer discretionary lead the most recent advance. Meanwhile, the high multiple, high growth winners of 2020 continued to lose ground, which made sense considering that low interest rates and a switch to ‘working from home’ drove those hyper valuations. Markets are now pricing in a scenario where the economy continues to open up, interest rates climb and inflation stays higher. The valuations of some of those ‘high growth’ stocks have collapsed. Peleton down 78% and Zoom down 59% highlight that list, but the more notable move is in the ARK Innovation Fund, which was the biggest winner of 2020 and highly publicized for its holdings in many of these high growth names. While the 5-year return on that Fund is still impressive, it is down almost 40% from its February peak despite a strong year for the largest holding in that Fund, Tesla Inc. What the market is telling us is that Omicron will not derail the recovery and that the Federal Reserve will indeed begin to start ‘pulling away the punchbowls’ of monetary stimulus that have dominated the landscape for much of the past decade. The Bank of Canada, the Bank of England and the Bank of Australia have all recently indicated similar plans for starting to reduce monetary support in 2022.

Under the scenario that we outline, Canadian equities look attractive heading into 2022, as they have some of the key criteria we believe investors will focus on; high dividend yields, lower valuations and a predominace of industries that have strong inflation hedges. Canadian stocks have lagged the U.S. for most of the past decade during which time growth stocks, which are driven in large part by rising valuations from lower interest rates, lead the more economically sensitive ‘value sectors’ that are more prevalent in Canada. With the recent pivot in Fed policy we are expecting 2022 returns to be driven by stocks with earnings stability, inflation protection, low valuations and higher dividend yields. Financials, energy, telecom, pipeline and industrial stocks all fit that definition and make up a large portion of the Canadian market. We also see a recovery in the auto sector as the semiconductor shortage eases, lifting stocks like GM, where the valuation is exceptionally low, as well as Canadian parts manufacturers Magna and Martinrea. Another growth industry at a reasonable valuation is the space industry as satellites continue to be launched into the LEO (Low Earth Orbit) field. Maxar will be putting its Legion satellites into space in mid-2022 which will allow it to assimilate more data for its Digital Globe unit, while MDA Inc. makes many of the robotics for those systems. Both stocks trade at about 10 times operating cash flow. Oil stocks remain incredibly cheap and the companies are starting to act in a much more ‘shareholder friendly’ way. Our top names are natural gas leaders Arc Resources and Tourmaline as well as the oil-levered names such as Cenovus, Crescent Point and Suncor. We also still think the semi-conductor industry has one of the best long term growth outlooks of any industrial sector, with chips powering everything from computers to cell phones to as well as IOT (internet of things). The damage to the economy in the past year from the global chip shortage is a key demonstration of how integral these products our to the global manufacturing chain. Our top pick there is the semi-conductor ETF, ticker SMH. Finally, we have to believe that mass vaccinations will encourage a return to normal activities, in which case we see Air Canada as having the best leverage to a recovering economy and return to travel.

But we also have to be wary of the top risks you are watching in the market in 2022. Bull markets don’t necessarily ‘die of old age’ or due to excessive valuations alone. While the virus risk remains front and centre, the growing global level of vaccinations and ongoing biological advances in dealing with variants, seems to be mitigating this risk a bit. That was clear in how quickly stocks moved back to new highs following the Omicron news. The biggest risk in our view is that inflation has become embedded in wage expectations and that ongoing supply chain issues remain more persistent. Central banks would then have to act even more aggressively to control it. As seen from the sharp pullback in the high growth sectors, the valuations of this market cannot handle any sharp increase in rates. If that occurs then 2022 could end up looking a lot like 2018. Earnings expectations are also contingent on a continued return to more normal economic conditions. Any shortfalls there would have a particularly negative impact on the airline, retail, energy and financial sectors.

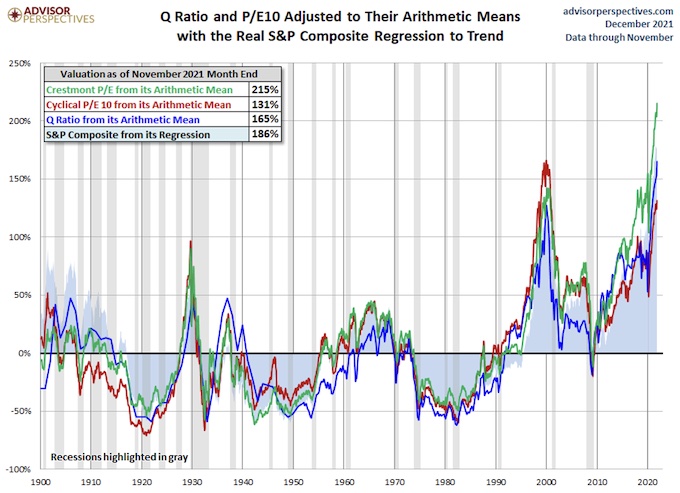

Historically speaking, overvaluation by itself doesn’t cause a bear market. It simply tells you the level of risk when the next bear unfolds. That though suggests the level of risk in this market has seldom been higher. To be clear, this is a monetary-driven bubble. That is not just from the Fed’s asset sheet, which has ballooned to over $8 trillion, but also the perceived guarantee that Fed officials will not take away the punch bowl anytime soon. By dropping short-term rates to zero, the Fed has created a TINA environment—”there is no alternative”—that has pushed stock market valuations $14 trillion higher than prepandemic levels. While there are limitless measures of how extended this bull market has become, the chart below sums it up fairly well, as it encompasses four different variables and shows a 120 year history. Almost all the measures have moved to all time hgihs, with particular note of the Crestmont P-E ratio. Since the business cycle constantly distorts earnings from its core baseline trend, this measure ‘normalizes’ those earnings based upon the relationship between historical nominal GDP and reported EPS. But in terms of measuring the risk to markets as a ‘return to the historical norm’ it is clear that the risk is higher today than at the end of the tech bubble or just before the Stock Market Crash of 1929.

While the S&P 500 climbed to yet another record high last week, the rally has been increasingly driven by a narrow group of mega-cap companies, which is reminiscent of the bubble in tech stocks in 2000. It was less than two years ago that we all marvelled at the fact that Apple Inc. became the first company to cross the US$1 trillion market capitalization threshold. This week the stock seems set to be the first to cross the $3 trillion level!. Investors have been treating these mega cap stocks as their safe-havens, or “pseudo-bonds,” in times of market volatilty. That was seen again in the initial Omicron sell-off in late November. This alone is not necessarily a reason to get out but needs monitoring. While these mega-cap growth stocks offer some safety in terms of better earnings stability and growth, the valuation cannot continue to increase indefinitely, especially if interest rates do indeed start to go higher in 2022.

On the other side of the ledger, the drawdown in smaller companies offers investors attractive entry points for “reopening stocks”, such as travel and hospitality, as well as energy and e-commerce, as inflation normalizes and concerns over the Fed’s hawkishness abate. Despite Omicron, the travel data continues to improve. The recent measures of TSA checkpoint travel numbers in the U.S. are back to 80% of their 2019, per-pandemic levels. Clearly people are more inclined to push forward with re-opening behaviour after almost two years of pandemic restrictions.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.