Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

September 30, 2018

Stocks in the U.S. continued their uptrend in September, traditionally the worst month for the market each year, while other global markets continued to deteriorate.

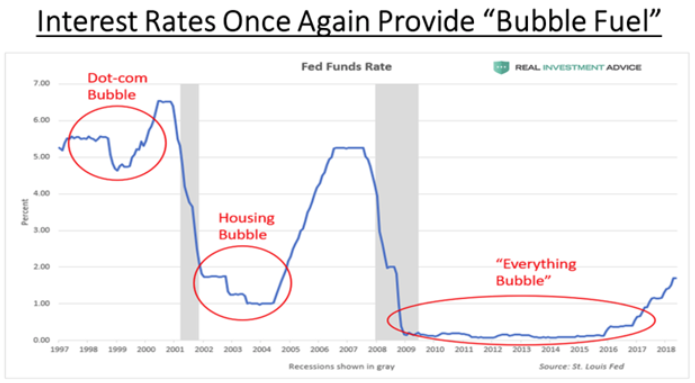

Ten years ago, we were in the midst of the Financial Crisis as the collapse of Lehman Brothers put the final ‘nail in the coffin’ on the mortgage finance bubble that had been growing for the prior five years and poured gasoline on a smouldering financial market crisis. Over the following six months, the S&P500 fell 46%, with similar declines for most global stock market and was followed by the most serious economic downturn since the Great Depression. U.S. Treasury and Federal Reserve officials put together a US$700 billion rescue package for the U.S. banks which avoided a complete run on the global financial system and allowed the banks to survive. While the scars of that downturn were expected by many to put a cloud over investing activities for a long time, investors have slowly forgotten the lessons of that downturn and the stock market in the U.S. has risen to new highs. Throughout this nine-year bull market, which has recovered all of the losses from the crash plus an additional 80%, the crash has continued to resonate. Stocks have been climbing a constant “wall of worry,” which shifted from the European debt crisis in 2011 to a Chinese stock meltdown in 2015 to a U.S. government shutdown and, finally, to the current brewing trade war. Meanwhile, the easy money policies have encouraged a massive build-up of debt at all levels, from governments to corporations. A rise in the combined balance sheets of the U.S. Fed, the European Central Bank and the Bank of Japan, from roughly $4 trillion in 2008 to a peak of $15 trillion in early 2018, has paralleled the rise in the S&P500.

What the markets now fret about most is the withdrawal of this unprecedented ‘medicine’ provided by central banks in the form of trillions of dollars’ worth of liquidity and zero interest rates, which have inflated asset values and spurred the long but slow recovery of major economies. After initially failing to either appreciate the approaching crisis in 2007-08 or respond adequately, policy makers seemed to learn from the mistakes made back in the 1930s; they tried to do the opposite of what policy makers did back then. Most specifically, by adopting quantitative easing—enormous central bank purchases of securities with money created out of thin air—the Federal Reserve, the European Central Bank, and the Bank of Japan, plus other major central banks, avoided what economists deemed the key policy blunder of the Great Depression of letting the money supply contract. Forbes cleverly coined this phenomenon as the “Everything Bubble” in an article last month.

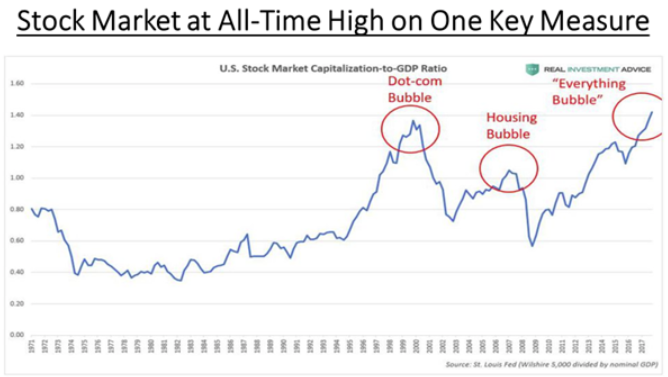

While the economic recovery took longer to take root than expected, the recovery in the financial markets has taken asset values to records not ever seen before. While many more bullish investors argue that stock markets are not necessarily over-valued on an earnings basis, the earnings in the U.S. have been artificially lifted by massive share buybacks in recent years as well as the tax cuts this year. On one of the other broader measures of stock market valuation, the ratio of stock market capitalization to GDP, stocks are more over-valued than they have been in at least 60 years!

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.