Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

June 2, 2023

The teflon economy keeps chugging along, for now! If we had been told at the beginning of 2022 that central banks, which had been incredibly sanguine about inflation risks, would increase interest rates by over 500 basis points over the next 18 months, we would have expected stocks to be down in the neighbourhood of 30-40% and the economy to be in a full-blown recession. That has clearly not happened. A few reasons why we think the ‘expected outcome’ has not occurred is that employment levels have remained robust as companies have been reticent to cut employment levels since they had such a hard time filling those positions when labour markets were tighter during the pandemic. We also think that many borrowers extended the terms of their loans when rates were low, particularly in the mortgage market. The most immediate beneficiary of the sharp rise in interest rates have been savers, who had accumulated record sums during the pandemic when spending on services and many goods was not an option. That ‘backlog of buying’ has kept consumer spending ‘stronger for longer’ as production and inventories were rebuilt. The re-opening of the service economy has also been a boon to economic growth. However, we believe that all of these ‘tailwinds’ are now beginning to fade as higher interest rates work though their ‘long and variable lags’ on growth. Front end indicators of growth continue to look fairly dismal. In the past, when the Fed tightened enough to fully invert the yield curve, an economic recession has always followed in the subsequent eighteen months. On that basis, we still expect the US economy to be in recession before year end.

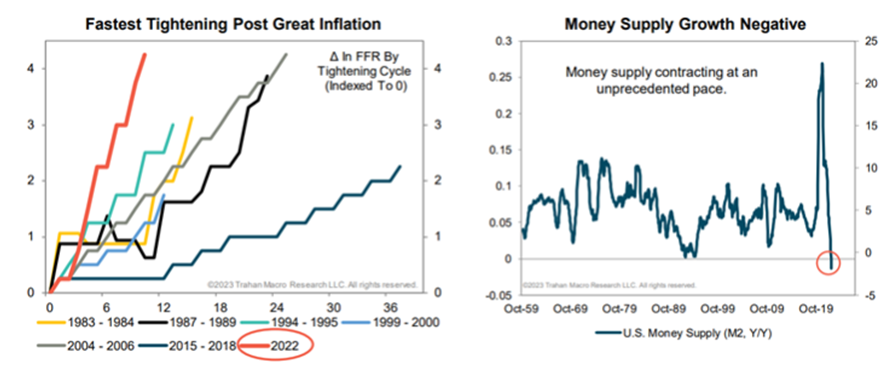

Global growth continues to be bifurcated with manufacturing activity remaining weak while the service-based economy keeps humming along. However, there are signs that from a directional point of view, economic momentum has started to downshift with many regional economic surprise indexes falling hard in May. We believe this slowing is a result of the lagged impact of the first tightening regime arising from higher policy rates over the past few years. ‘A picture is worth 1000 words’ when it comes to describing the headwinds from central bank actions of the past year. Below we can see (left chart) that the increase in interest rates has been more rapid than any tightening cycle over the past four decades. It also comes after a period when central banks had been adamant that rates would remain low for a long time. The right chart is even more telling. The drop in money supply growth has been the sharpest on record. If the monetarists are all correct and money supply is what drives economic activity, then it seems almost impossible for the economy to avoid a recession. Regardless, growth will slow going forward but interest rates will stay ‘higher for longer.’

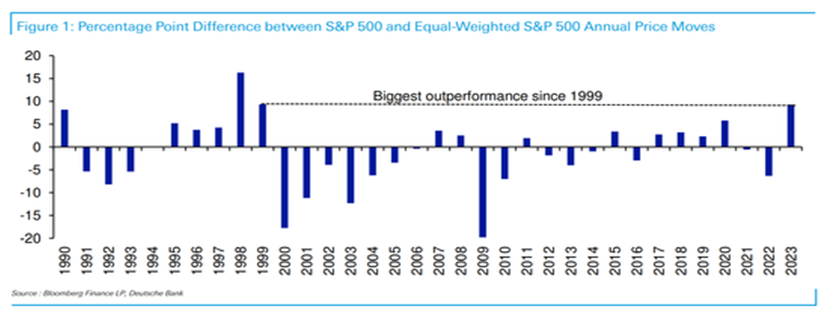

While investors debate the economic outlook, we have seen the most narrow breadth of advances for the stock market in almost 25 years as a very small group of mega-stocks have been responsible for more than 100% of the total gains in the major averages. This trend accelerated in May with the ‘equal weighted S&P500’ Index falling 3% while the Nasdaq100 Index (almost all technology) rose almost 10%. Bull markets in stocks are generally associated with increasing breadth as more and more names participate in the advance. Clearly that has not been the case here, which further supports our overall cautious outlook for stocks, particularly with the impact of the aggressive tightening of interest rates over the past year still working their way through the economy. The chart below shows that the last time we saw such strong relative gains of the S&P500 versus the ‘equal weighted’ S&P500 was in 1999, just as we were seeing the peak of the ‘dot com’ technology bubble in stocks. Following that we saw seven straight years where the equal weighted index did better, meaning that good individual stock picking in the rest of the S&P5600 was able to add more value versus the overall index. The risk for investors is that this stronger performance for the ‘rest of the market’ comes during a period of overall stock market weakness, not unlike what we saw in 2001-2002. In either case, we see better relative returns away from those big tech names that have been leaders.

Despite the prospect of bad news on both the economy and corporate earnings over the next few quarters, we have not gone to an underweight position in stocks. Investors are well aware of the economic risks going forward and most of this bad news, particularly in cyclical stocks, seems to have already impacted investment decisions. Investor allocation to equities relative to bonds has dropped to its lowest level since the global financial crisis as worries about a recession take hold. In terms of our asset mix strategy, we do remain somewhat cautious on stocks, but see more potential for upside surprises in the next year and therefore don’t want to carry too low a weight. We currently have about 48-50% of most client investment portfolios in stocks, with a somewhat more defensive bias (i.e. overweight telecom stocks, pipelines, energy and golds). We added to bonds earlier this year and continue to have about a 40% weight in fixed income, primarily government mid and long-term bonds in both the U.S. and Canada. We don’t expect a peak in short-term interest rates until the third quarter and then don’t see any reductions in rates beginning until mid-2024. This is a more bearish view on rates than consensus expectations of investors and, if we are right, does suggest more risk for stocks. The biggest risk for central bankers is that they begin to reverse policy on interest rates and too and then see a resurgence in inflation from much higher levels than they saw at the beginning of this cycle. This is what happened in the 1970’s. Ultimately it forced central banks to get even more aggressive on interest rates in the 1980-82 time frame (the ‘Volcker era’, named for Fed Chairman at that time Paul Volcker), where we saw rates move up to mid-teens levels in order to get ‘double-digit’ inflation rates back down. Central bankers are clearly aware of this history and do not want to repeat it. We therefore think they will hold interest rates at these elevated levels until inflation has moved all the way down to their 2% target, and maybe even below it, and then stabilize at those lower levels.

Longer-term interest rates have risen in the past month as inflation remains at elevated levels, employment has been resilient and the expected economic downturn has not yet taken hold. But we still see all the risk indicators for economic growth on the downside and that the ten-year U.S. bond will trade back down to yields in the 3.0% range over the next year. History has shown that in a recession scenario, yields fall a minimum of 200 basis points below peak Fed funds rates, which we expect to be no higher than 5.25%. Cash though does remain an attractive alternative in the short term given the sharp rise in short-term interest rates. Bottom line, it’s hard to get really excited about stocks knowing that we are most likely headed into a recession in the back half of 2023 and still face a period of elevated interest rates (at least in comparison to where they have been over the past decade). But history has also shown us that times of economic weakness and investor despondency are also times to be looking to position for the next cycle since most of the bad news is already ‘priced in.’ We may not be quite there yet, but it does feel like we are getting closer!

Time to Unwind the Growth Trade. Everyone knows that the breadth of the market has been miserable in 2023 as the market has been supported by just seven mega-cap tech stocks — Apple, Microsoft, Nvidia, Meta, Tesla, Amazon and Alphabet — which have accounted for 95% of the S&P500′s total return so far in 2023. Everything has gone right for Big Tech. First off, valuations have risen because long-dated bond yields have dipped as the market anticipates a pause in the Federal Reserve’s interest-rate increases. At the same time, analysts are more upbeat about earnings. Analysts’ forecasts for 2023 earnings per share have risen this year for all these companies, except for Amazon. On top of all that we have seen a mania for anything related to artificial intelligence (AI). The blowout numbers from AI chip leader Nvidia gave the rally a further boost in the last two weeks of May. Even skeptics about the ‘hoopla’ around AI have to admit that those reported quarterly numbers were shockingly good. We have not seen such a solid earnings beat in tech since Blackberry’s third quarter in 2006, which also saw its stock rise 50% the next day. Clearly there is a shift going on in the semiconductor industry to the higher margin chips that power the generative AI transformation and Nvidia is the biggest player in that market right now. While this has more staying power than either the ‘dot com’ or ‘crypto’ bubbles, we are still not fully convinced that the projected growth and penetrations of AI will meet these extreme expectations. Though we are not selling out of tech altogether, we have been migrating away from the tech trade recently. In our view, either the advances will broaden out to include more cyclical sectors (and tech will lag) or these leaders will be the last one to fall in a general market downturn.

At the sector level, we are now back to a market weight in the technology sector while overweighting energy, telecom and health care. Growth stocks and many defensive sectors are currently very expensive creating valuation risk that more than offsets their lower economic sensitivity. Cyclical stocks have low multiples and very high equity risk premiums suggesting a more severe recession than seems likely has been discounted. While earnings in the cyclical stocks will be hurt by the impending economic slowdown, valuations have already factored in most of this weakness. We see stocks in the auto and leisure good industries trading at single-digit earnings multiple. Moreover, inventories are nowhere near the peaks typically seen late in the economic cycle since the semi-conductor shortage and the pandemic shutdown had put constraints on manufacturing, such that these companies need to continue to run near full capacity just to meet existing demand and build inventories back to normal levels. BRP Inc, CargoJet, Magna, GM and Martinrea remain our top names in those sectors. While still somewhat cautious on the bank stocks due to tighter lending standards and an economic slowdown, most Canadian and money-centre U.S. banks have strong deposit bases, excellent capital ratios and trade at the very low end of their traditional ranges, with the benefit of high dividend yields while investors wait for the economy to through its downturn. Recent earnings reports from the major Canadian banks fell short of expectations but the stocks have more than compensated for that risk in our view. Capital ratios are extremely strong in the group, valuations are back to cycle lows and dividend yields are attractive.

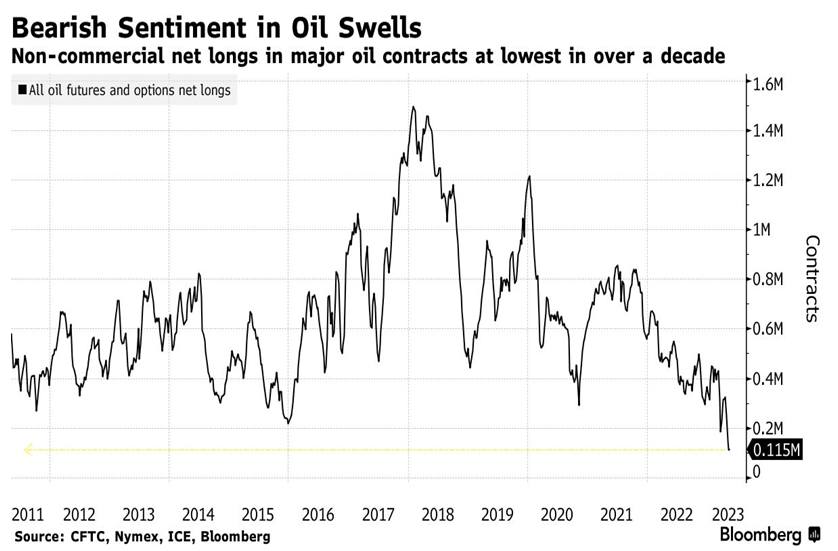

Nowhere, though, are relative values more attractive than in the energy sector. While investors lament the inability of crude oil to hold above US$80 versus some expectations of another march up to US$100, we would rather focus on the fact that these companies are generating massive free cash flows and trading at historically low multiples even assuming oil prices only in the US$75 range. Many Canadian producers (Baytex, Whitecap, Crescent Point and Cenovus top our list) trade at cash flow multiples of only 3-4 times at current strip (oil) prices and free cash flow yields over over 20%! Meanwhile, underlying physical markets aren’t reflecting the dire state that traders are preparing for. Refineries are processing the most crude for this time of year since the pandemic began. Air travel is rising just about everywhere, and gasoline demand in the U.S. is now at the highest level since December 2021. At the same time, fuel inventories are below seasonal norms for gasoline and diesel in the US, and OPEC+ cuts and Canadian wildfires have limited crude supply. On top of all that, financial players in the oil market are positioned even more bearishly than they were in the crazy period in early 2020 when oil futures briefly slipped into negative territory. The chart below shows the non-commercial contracts in oil and the lowest level in over a decade. Any shortfalls in production, increases in demand of geo-political risk could lead to a major short-covering surge in prices. Physical markets are expected to remain tight as refinery output grows, Russian production is unable to grow and OPEC+ cutbacks remain in place.

We did not even talk about the U.S. debt deal and the risk of a default, but it really feels like we have been taken to the edge with these risks many times before and the politicians always manage to ‘kick the can down the road’ a little more and promise to deal with it a future date. We expect the same outcome here. There is absolutely no upside to the politicians in not approving whatever deal is put on the table. The fact that almost everyone seems unhappy with the deal suggests to us that it did a good job of playing the middle of the road. While even a temporary delay in payments on U.S. debt would have caused a major disruption to financial markets, it really did not seem to be a serious threat in the eyes of most investors. Of course it is the unexpected events that cause the biggest moves in markets so, until the Fiscal Responsibility Act gets passed by both houses of congress and signed off by the president, that market risk remains in place.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.