Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

January 24, 2018

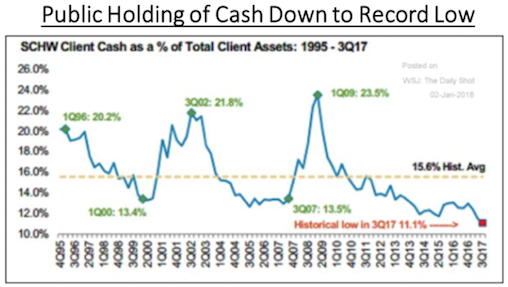

The problem for stock investors now is that all of this potential good news on global economic growth, lower tax rates boosting earnings and upcoming increases in dividends, stock buybacks and corporate activity is already being reflected in current stock valuations and has lead to a ‘giddiness’ in investor sentiment that is typically only seen at market peaks. Stock market optimism among professional investors just keeps on surging, and is now at the highest level since before the crash of 1987. Bullishness, or the belief that the market is heading higher, is now at 66.7% in the latest Investors Intelligence survey, a widely followed gauge of sentiment among investment newsletter authors. That’s the highest level since early April 1986 — a potential warning sign that the rush into equities is getting overdone. After all, a year after the bulls had reached this level came the infamous Black Monday crash that sent the Dow Jones industrials down nearly 22% in a single day. This bullish sentiment is clearly also being reflected in the behaviour of investors. The January Bank of America Merrill Lynch Fund Managers Survey — another gauge of professional investors’ sentiment — showed cash levels at a five-year low, allocations to stocks at a two-year high and the overweight ratio of stocks to government bonds at its highest since August 2014.

One ‘entity’ could be held responsible for the ongoing strength in global stock markets, and her name is Tina Fomo, which is a combination of the two acronyms that are often used to explain the psychology underlying the market’s spectacular rise: TINA, for There Is No Alternative; and FOMO, for Fear of Missing Out. FOMO seems to remain a key factor in the current rally. One could certainly argue that the current year-end/New year’s rally has been propelled by investors’ unwillingness to let the market go higher without them. Even the slightest downturn is almost immediately met with an influx of new buying. Sentiment indicators are registering strongly bullish, and virtually all potentially risky situations that have occurred since the presidential election have either been ignored or considered to be buying opportunities.

TINA may be showing some cracks, however. The U.S. Federal Reserve’s recent rate hikes have pushed up short-term rates to a level where they may provide some competition for equities. The two-year Treasury rate is now yielding more than the S&P500 dividend rate for the first time in roughly a decade. Moreover, other central banks, including the Bank of Canada, have been following the U.S. in raising interest rates. That alone is not sufficient to produce a significant decline in the stock market, but a Fed-propelled steady rise in short-term rates bears attention, as higher risk-free rates could cause a re-rating of equity valuations.

Further, there are bond investors who believe that as the 10-year Treasury yield rises through 2.5%, it is signaling the end of the bond market’s long-term bull run. At some point, higher interest rates can provide credible competition to stocks and make it more expensive to fund operations or share buybacks. We have already seen underperformance from interest rate sensitive sectors such as utilities and real-estate investment trusts. But the broader market and even the financial sector have shown little evidence of rate concerns so far. The bottom line is that we find this market reminiscent of 1987 in many ways. Back then, economic growth was on the upswing and it seemed that every day we hit another new high in stocks and a decline in bond prices, reflecting the higher yields. That pattern persisted throughout the first three quarters of the year, proving that stocks and bonds can diverge meaningfully for quite some time. The stock market peaked in August of 1987 and those trends then reversed with a vengeance on October 19thas stock prices fell sharply and bond prices rallied. We’re not saying that 2018 will end like 1987, but it would be imprudent for stock investors to ignore a significant rise in rates, if that occurs.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.