Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

January 24, 2018

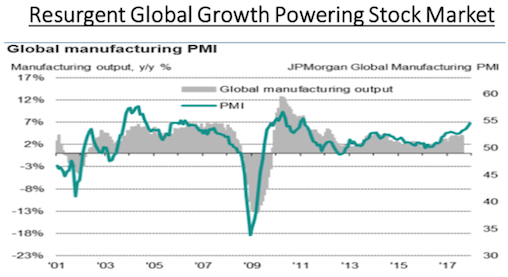

The first month of 2018 looked a lot like all of last year, with U.S. stocks fighting their way higher and even the slightest pullback being quickly met by a large influx of new buying, especially in Index Funds. Canada, once again, is lagging due to some more weakness in energy stocks despite the move higher in oil prices to the best level since 2014. One of the reasons 2017 was a good year for the markets was because the economy accelerated globally. There are signs of sustainable growth everywhere; the momentum will continue for a while. U.S. gross domestic product is likely to be lifted somewhat this year because of the tax cut. It should benefit economic growth beginning early in the year; but we’ll find out if the impact is lasting. However, Europe and Asia are also experiencing decent recoveries, due both to the lagged impact of all the monetary easing (zero interest rates do eventually work, as proven by the move in the U.S. economy). The chart below shows the movement in the Global PMI (Purchasing Managers Index) over the last 18 years. Following the sharp recovery after the Financial Crisis in 2008, growth slowed down to a moderate pace of the past eight years. Now we are beginning to see a clear pick up. What’s important to remember is that economic growth, unlike stock market psychology, gains strong momentum in either direction and rarely reverses quickly. This suggests that the only way we well see a slowdown in this growth is if the monetary authorities (central banks) start to tap on the brakes a little harder by raising interest rates more quickly and aggressively than expected.

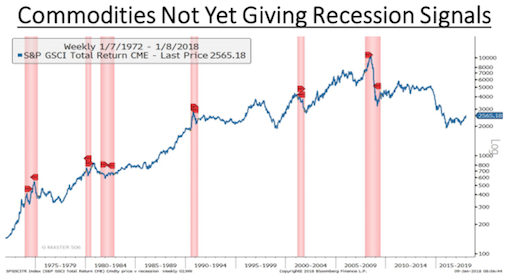

Not only has growth been strong on a global basis (and picking up momentum), none of the typical ‘end of cycle’ signs have been showing up in the economic data. We really can’t find a recession anywhere on the economic radar screen. We’ve never gone into a recession without the Index of Leading Economic Indicators falling below zero. In the U.S., the LEI is currently up 5%-plus, year over year, and the trends look to be persistent. Other ‘forward-looking’ data, including the Purchasing Managers’ Index and measures of CEO and small-business confidence, are all at cyclical high levels. These types of sentiment indicators fall off a cliff in front of a recession. Another good recession indicator is commodity prices. They tend to have sharp increases late in the economic cycle and then peak and begin to turn down in front of the next recession. We are not seeing any of the same action in commodities lately. In fact, they had been in a clear downturn since peaking before the financial crisis. While we have seen a good recovery in copper, oil and many industrial metals over the past few months, those commodities remain well below prior peaks. Most of the recent gain in some commodities can also be traced back to the weakness in the U.S. dollar. The dollar and commodities tend to trade inversely to each other.

In the wake of the new tax provisions enacted last month, U.S. corporations are planning to bring billions of dollars held overseas back home. Investors have been wondering how much of that cash will be returned through dividends and share repurchases versus how much will be plowed back into expansion and other spending to support growth. The latter is clearly the option that would benefit the domestic economy the most. The ‘jury is still out’ on this one but Apple agreed to pay US$38 billion in taxes in order to be able to repatriate over US$250 billion in cash held in overseas accounts. They say that this money will be spent on growth in the U.S., ultimately leading to the creation of over 20,000 new jobs and took a page from Amazon’s playbook by announcing plans to build a second U.S. campus. Companies could also go the increased dividend route with some analysts speculating that Microsoft could pay a massive special dividend. There’s also a third option; mergers and acquisitions. With the economy booming, the market surging, and disruption an ever-present threat, companies might be more likely to purchase other companies to boost growth, especially in tech where ‘disruptive technologies’ are constantly emerging that threaten the growth of the larger conglomerates. For now, companies have been reporting massive charges to fourth quarter earnings as they enable themselves to bring back those massive sums held outside the U.S. and give themselves the option to take one of these routes with the excess cash. The growth option would help the economy while the buyback or dividend routes would only help stock prices further.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.