Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

May 13, 2024

In April, once again preferred share redemptions by banks and speculation regarding future redemptions drove the preferred share market higher. The preferred share market moved sideways for the first part of the month as bond yields moved higher and equity market weakness pulled risk assets lower. However, the market turned around when Royal Bank of Canada announced the redemption of a rate reset issue that surprised investors, given that the day before National Bank of Canada announced that it would not redeem a rate reset issue with a higher reset spread. A few days after its announcement, Royal Bank issued a U.S. dollar Limited Recourse Capital Note (LRCN) which resulted in favourable economics that supported the redemption. This redemption led to more speculation regarding further preferred share redemptions by banks. Later in the month, Bank of Montreal announced the redemption of two rate reset issues. Despite the market having largely anticipated this, it added to the positive momentum of the market. As a result, the prices of many banks’ rate reset issues scheduled to reset later this year and in 2025 moved higher. Also, on the last day of the month, investors received $850 million from previously announced redemptions, which generated reinvestment related buying. Over the entire month, rate reset and floating rate issues had positive returns, while perpetual issues generated negative returns. The S&P/TSX Preferred Share index ended the month with a gain of 1.22%.

Despite bond yields moving higher in April, Canadian economic data released during the month remained supportive of potential interest rate cuts as soon as June or July. The unemployment rate jumped to 6.1% from 5.8% as the number of jobs unexpectedly shrank while the labour force continued to grow rapidly due to surging immigration. Growth in GDP appeared to be decelerating from January’s robust pace, with slower than expected growth in February and StatsCan estimating no growth in March. Retail sales were also weaker than expected, suggesting high interest rates were discouraging consumption. Inflation was little changed as CPI rose to 2.9% from 2.8%, but core measures eased to slightly below 3.0%. The Bank of Canada left its interest rates unchanged at its April 10th meeting and indicated that it wanted more evidence that inflation was under control. The Bank also indicated that rate cuts are likely to be gradual when they finally begin.

In April, there were no new issues of preferred shares. However, as noted above, Royal Bank issued a U.S. $1.0 billion LRCN with an initial coupon rate of 7.50% and a reset spread of 289 basis points. After the issue was converted to a Canadian dollar equivalent security, it was estimated that with the redemption of the $500 million RY.PR.Z that had a reset spread of 221 basis points, the bank was reducing its after-tax cost of capital by approximately 60 basis points. The Royal Bank transaction led to speculation that the U.S. dollar LRCN funding option would lead to further redemptions of bank rate reset issues with reset spreads between 200 and 300 basis points. Banks that have reached the regulatory limit for LRCNs may need to issue an institutional preferred share to increase their limit and allow for future LRCN issuance. However, institutional preferred shares currently do not offer any savings versus outstanding $25 par shares. Investors remain hopeful that the Office of the Superintendent of Financial Institutions will continue to encourage banks to replace traditional $25.00 par preferred shares with LRCNs or institutional preferred shares.

The coupon and reset spread of the Royal Bank LRCN were lower than the February U.S. dollar LRCN issue from Bank of Montreal which had an initial coupon rate of 7.70% and a reset spread of 345 basis points. Following Bank of Montreal’s LRCN issue, the market had correctly anticipated its April redemption announcement of the $350 million BMO.PR.F series and the $500 million BMO.PR.S series. Year to date, announced redemptions by banks total $2 billion and continue to drive the preferred share market’s positive performance.

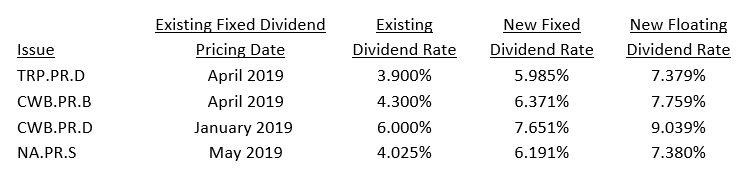

During the month, four series of preferred shares reset their dividends. Dividend rates continued to reset significantly higher because the 5-year Canada bond yield continued to be substantially higher than five years ago. Details of the resetting issues were as follows:

As of the end of the month, National Bank had yet to announce if enough investors had opted for the floating rate option for one to be issued. However, both TC Energy and Canadian Western Bank announced that an insufficient number of investors in their respective resetting series wanted to make the switch into the floating rate series and all shares will remain fixed rate ones. Despite floating rate yields substantially higher than fixed rate ones, preferred share investors remain concerned that interest rates will fall significantly in the next year and take floating rate dividends below fixed rate levels.

Also in April, Laurentian Bank announced that it does not intend to redeem the LB.PR.H series on June 15th. The new dividend rates for the fixed and floating rate options will be announced on May 16th. In addition, Manulife Financial Corporation announced that it does not intend to redeem the MFC.PR.L series on June 19th. The company will announce the new dividend rates for the fixed and floating rate options on May 21st.

In aggregate the seven largest preferred share ETFs had an outflow of $73 million in April. Despite another month of strong market performance, this was the fourth month in a row of outflows and was the largest monthly outflow this year.

J. Zechner Associates Preferred Share Pooled Fund

The fund had a return of -0.17% in April, and underperformed the S&P/TSX Preferred Share index. The fund’s underperformance was largely a function of security selection. During the month, rate reset issues had the best performance, particularly bank reset issues. The fund held only a few of those shares, which hurt performance. In addition, the fund held relatively more perpetual type preferred shares which had a negative return for the month.

Portfolio activity during the month included switching AQN.PR.A into AQN.PR.D for a pickup of approximately 20 basis points. Also, we switched FFH.PR.K into IFC.PR.G and TRP.PR.D for a pickup of more than 50 basis points and purchased more of the floating rate FFH.PR.D shares that yielded over 9.20%. Other activity included adding to the TD.PF.C position, which trades below par, and selling some of the TD 7.232% institutional preferred shares.

Outlook and Strategy

Despite another month of strong positive performance, we believe the preferred share market continues to offer attractive yields, significantly better than corporate bonds, making them an appealing fixed income alternative. The 5-year bond yield continues to be substantially higher than five years ago resulting in substantial increases in dividend rates on resetting issues, which is reflected in three of four resetting issues in April increasing their dividend rates more than 2.00%.

The surprisingly sharp drop in inflation in the last two months makes the next CPI report on May 21st a particularly important one as it will be the last measure of inflation before the Bank of Canada’s June 5th interest rate announcement. While we anticipate that inflation will rise back above 3.0% because of energy and shelter costs, another lower-than-expected CPI report may encourage the Bank of Canada to begin easing monetary policy. However, we believe the Bank of Canada will not lower interest rates as much as the market currently expects.

For several years, the Bank has been estimating the “neutral” interest rate, which is neither stimulative nor restrictive, to be between 2.00% and 3.00%. More recently, though, the Bank has indicated that the neutral rate has probably increased. Our view is that the Canadian economy can sustain significantly higher interest rates than prevailed in the 2009 to 2022 period.

Notwithstanding the possible slowing of the Canadian economy, we continue to remain confident in the creditworthiness of the issuers in the portfolio, as these companies have successfully weathered previous economic downturns without impacting their ability to pay the dividends on their preferred shares.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.